Transaction Analysis – Volume II – Supplies under Reverse Charge Mechanism (RCM)

In continuation of our series of article on Transaction analysis in GST, let us now analyze transactions, covered by RCM.

1) Reverse charge mechanism (RCM)- Impacting the GST provisions

- Under GST, RCM is applicable to both supply of certain Goods and or services as notified by the Government. RCM is also applicable for supplies received from unregistered suppliers also.

- Persons who are required to pay tax under reverse charge has to compulsorily register under GST

- Though GST is paid, this turnover is not be counted for determining Aggregate Turnover, as turnover for output tax liability, as turnover in a state or union territory.

- The rule of adding up of output tax liability if payment Is not made within 180 days for the supplies received is not applicable to RCM supplies.

- Where the input is common to both exempted and taxable supplies, supplies under RCM is to be computed as exempted supplies, for determining reversal of ITC on exempted supplies.

Also Read- GST Transaction Analysis – With Practical examples-Part I

2) Time of supply- For RCM supplies

a) In respect of Services, RCM liability is the earliest of

(a) the date of payment by the recipient

(b) the date immediately following sixty days from the date of issue of invoice or any other document,

If time of supply could not be determined from a & b, then date of entry in recipient book.

Also, date of entry in recipient book, if the supply is by associated enterprise, who is outside India

b) In respect of Goods, RCM liability is the earliest of

(a) the date of the receipt of goods; or

(b) the date of payment; or

(c) within 30 days from the date of issue of Invoice

In the event of it is still not possible, from the above, it shall be the date of receipt as per recipient records.

3) Input Tax credit eligibility

To the extent of tax payment Input tax credit is eligible subject to the eligibility. If the service against which, GST is paid on RCM basis, input tax credit is not eligible then such tax paid is a cost of the service. Accordingly, to be treated in the financials and return.

It could be observed there are timing difference between the tax determination, tax payment and availing the input tax credit. Also, all the tax paid under RCM may not be eligible for input tax credit.

4) Entries in Financial

Since the balance of CGST, IGST and SGST/UTGST accounts in trial balance has to match with the return, enough care is to be ensured to park the time difference entries in a separate GL, till it is accounted in return as per GST provisions.

Illustration

While time of supply is determined as referred in para 2, the following entry is passed

Rs.

On 1st September 2017

While booking the expense

Dr Service Expense – 1000

Dr IGST credit not availed -200

To S. Creditors 1000

To IGST payable 200

On 1st October 2017

While making payment to Supplier

Dr S creditors – 1000

To Bank -1000

While making GST payment

Dr IGST Payable-200

Cr Bank 200

If the service is eligible for ITC, then

Dr ITC credit availed – 200

Cr ITC credit not availed- 200

If the service is not eligible for ITC, then

Dr Service Expense – 200

Cr ITC credit not availed- 200

Entries in GST Returns

As it is a tax liability to the service receiver, the entries would be uploaded in the GSTR -2

For addition of entry

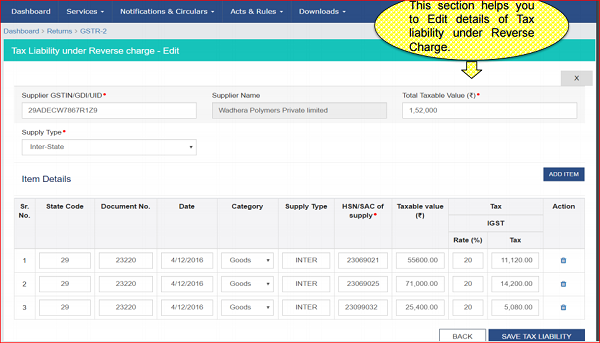

After additions, the screen will look like as below, with an option to Edit at item level

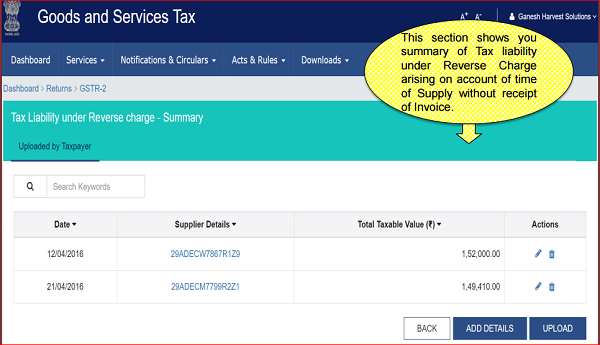

Summary of entries after editing

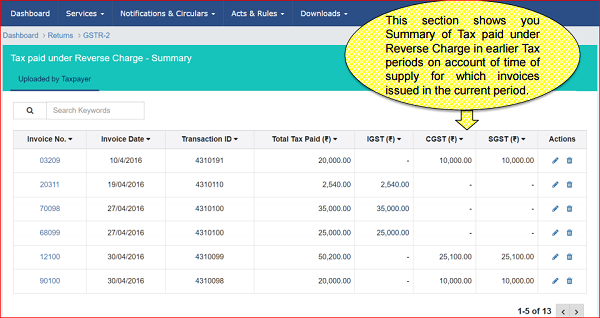

Final Summary of RCM Tax paid screen

The treatment and accounting of ITC in respect of transactions where credit availed but payment not made within 180 days will follow in volume III of Transaction analysis series.

Author Bio

Good & helping article..

Can you please tell me when will i get ITC credit if Tax is paid by me under RCM?

For e.g. my tax liabiilty arise in July in RCM & i paid tax in before 10th August and upload data of RCM.. May i get credit of tax paid in RCM in August return or September return??