The intention is here to tax works contract (Including any transfer of property in goods in the execution of contract) related to immovable property as the supply of service. Works contract, as well as the sale of under construction apartment, shall be subjected to GST. Stamp duty has not been subsumed in GST, therefore over and above GST; buyer has to pay a stamp duty 5-8% in as applicable in different states. Currently, service tax charge on 40% of project value, thus the effective service tax rate is 6%, similarly effective vat rate around 1% charge on project value in the different state. We should wait for what will be tax rate on the work contract in the new tax regime.

Now, the question arises in mind what will be the treatment of Composite contract related to movable property, the concept of composite supply and mix supply has been inserted in Revised Model Draft GST Law in Nov 2016.

It is clear that work contract will be taxed in GST, but the issue relating to Rate, Value of Supply, and Place of supply and time of supply can arise in future.

A transaction of works contract, is now, sometimes, taxed twice; firstly as a sale by the State Government and secondly as service by the Central Government.

Works contracts can straddle two taxable activities as per the current law. There is of course of supply of goods. Then, due to the very nature of the contract, there is a supply of services.

As of now, the supply of goods is taxable in the form of Value Added Tax (VAT), while the services element is taxable as service tax.

In law, there have been differing views of the Supreme Court and the High Court’s on the applicability of this theory. The final word of the Apex court in BSNL and Others vs. Union of India (SC 2006) was that the aspects doctrine pertains to legislative competence and not the application of taxation on the same components of a transaction.

At present, State VAT laws have specific provisions for taxing works contracts. To avoid taxing the services element, these laws and associated rules provide for either separation of labour and materials or percentage deductions in transaction value. Another method is of prescription of a lower rate of tax in a composition/lump-sum scheme for works contracts. The service tax law has also provided for similar treatment to avoid taxation of sale of goods as part of a works contract.

The overarching concept in a GST is one of supply which subsumes the concepts of sale of goods, provision of services and manufacture. In GST Model, goods as well as services will be taxed at a uniform rate. Therefore the dispute whether a transaction is subjected to VAT or Service tax comes to end.

After article 246 of the Constitution, the following article shall be inserted, namely:—

“246A. (1) Notwithstanding anything contained in articles 246 and 254, Parliament, and, subject to clause (2), the Legislature of every State, have power to make laws with respect to goods and services tax imposed by the Union or by such State.

(2) Parliament has exclusive power to make laws with respect to goods and services tax where the supply of goods, or of services, or both takes place in the course of inter-State trade or commerce.

In article 366 of the Constitution,—

(i) after clause (12), the following clause shall be inserted, namely:—

‘(12A) “goods and services tax” means any tax on supply of goods, or services or both except taxes on the supply of the alcoholic liquor for human consumption;’;

All supply of goods or services or both will attract CGST (to be levied by Centre) and SGST (to be levied by State) unless kept out of purview of GST. GST will be applicable even when the transaction involves supply of both (goods and services). In effect, woks contracts will also attract GST. As GST will be applicable on supply ‘the erstwhile taxable events such as manufacture‘, sale‘, provision of services etc. will lose their relevance.

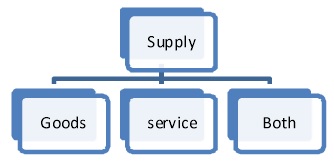

For taxing a transaction in GST, two things are important one is supply and other is goods or service or both

Section 2(95)

“Supply” shall have the meaning as assigned to it in section 3;

Supply includes—

(1)

(a) all forms of supply of goods and/or services such as sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business,

(b) importation of services, for a consideration whether or not in the course or furtherance of business, and

(c) a supply specified in Schedule I, made or agreed to be made without a consideration.

(2) Schedule II, in respect of matters mentioned therein, shall apply for determining what is, or is to be treated as a supply of goods or a supply of services.

(3) Notwithstanding anything contained in sub-section (1),

(a) activities or transactions specified in schedule III; or

(b) activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities as specified in Schedule IV, shall be treated neither as a supply of goods nor a supply of services.

(4) Subject to sub-section (2) and sub-section (3), the Central or a State Government may, upon recommendation of the Council, specify, by notification, the transactions that are to be treated as—

(a) a supply of goods and not as a supply of services; or

(b) a supply of services and not as a supply of goods; or

(c) neither a supply of goods nor a supply of services.

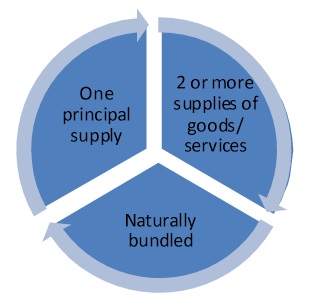

(5) The tax liability on a composite or a mixed supply shall be determined in the following manner —

(a) a composite supply comprising two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply;

(b) a mixed supply comprising two or more supplies shall be treated as supply of that particular supply which attracts the highest rate of tax.

Section 2(49)

“Goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply;

Section 2(92)

“Services’’ means anything other than goods.

Explanation 1.- Services include transactions in money but does not include money and securities;

Explanation 2.- Services does not include transaction in money other than an activity relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged.

Now, we discuss the provision of draft GST Provisions related to Composite contract,

Section 2(27)

“Composite supply” means a supply made by a taxable person to a recipient comprising two or more supplies of goods or services, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply;

Section 2(78)

“Principal supply” means the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary and does not constitute, for the recipient an aim in itself, but a means for better enjoyment of the principal supply.

Example: Indian Airlines provides passenger transportation service. They also supply food on board to passengers. Supply of transportation services would be the principal supply and the service as a whole would qualify as composite supply.

Section 2(66)

“Mixed supply” means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply.

Examples: Supply of soap bars where soap boxes are given free of cost; supply of wheat for which a bottle of honey is given free of cost.

In the above example of honey being supplied with wheat, both wheat and honey will be taxed at the rate of tax applicable for honey (being commodity taxed at higher rate).

The provision of declared service continues without any modification, in GST law also, for removing any ambiguity of taxation of work contract, the work contract and sale of under constructed property shall be subjected to tax as service under GST. Schedule II define the matters to be treated as supply of goods or service and Sec 2(110) defines the work contract.

Schedule II

MATTERS TO BE TREATED AS SUPPLY OF GOODS OR SERVICES

5. The following shall be treated as “supply of service”

(a)……………….

(b) Construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or before its first occupation, whichever is earlier.

Explanation.- For the purposes of this clause-(1) the expression “competent authority” means the Government or any authority authorized to issue completion certificate under any law for the time being in force and in case of non-requirement of such certificate from such authority, from any of the following, namely:–

(i)an architect registered with the Council of Architecture constituted under the Architects Act, 1972; or

(ii) a chartered engineer registered with the Institution of Engineers (India); or

(iii)a licensed surveyor of the respective local body of the city or town or village or development or planning authority;

(2) the expression “construction” includes additions, alterations, replacements or remodeling of any existing civil structure;

(f) Works contract including transfer of property in goods (whether as goods or in some other form) involved in the execution of a works contract;

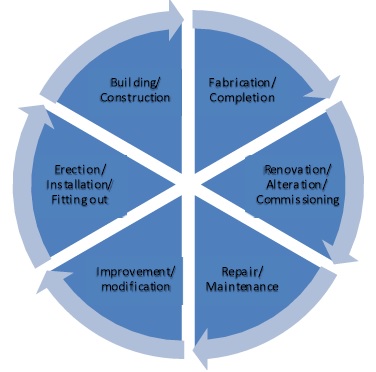

Section 2(110)

“Works contract” means a contract wherein transfer of property in goods is involved in the execution of such contract and includes contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property;

Note: From the means part of definition it is seemed that contract related to Movable property also cover in work contract but the intention here is to cover the only contract related to immovable property only.

The work contract as well as sale of under construction property shall be taxable as provision of service, which also includes the value of goods which is transfer in execution of work contract. Schedule II specifies that works contracts will be treated as supply of services and accordingly, provisions of time of supply and place of supply of services shall apply to works contract transactions.

Contract for Work Vs Contract of Sale

It shall be notable that if we constructed immovable property on its own and later on sale to other person then it is a contract for sale of immovable property and not work contract and shall be out of GST ambit, constitutionally sale and purchase of real estate shall be matter of state and liable to stamp duty and property tax. In case of Larsen and Tourbro v. State of Karnataka (2014) it was held that if the contract entered into after construction is completed, it is not a work contract.

Negative List of Credit;

Sec 17(4) notwithstanding anything contained in sub-section (1) of section 16 and subsection (1), (2), (3) and (4) of section 18, input tax credit shall not be available in respect of the following:

(a) …………………

(b)………………

(c) Works contract services when supplied for construction of immovable property, other than plant and machinery, except where it is an input service for further supply of works contract service;

(d) goods or services received by a taxable person for construction of an immovable property on his own account, other than plant and machinery, even when used in course or furtherance of business;

Explanation 1.- For the purpose of this clause, the word “construction” includes re-construction, renovation, additions or alterations or repairs, to the extent of capitalization, to the said immovable property.

Explanation 2.- ‘Plant and Machinery’ means apparatus, equipment, machinery, pipelines, telecommunication tower fixed to earth by foundation or structural support that are used for making outward supply and includes such foundation and structural supports but excludes land, building or any other civil structures.

Conclusion:

By treating work contract as service provide the complete solution of continues dispute arise in past. Once is it established that composite contract shall be liable to GST, issue related to rate, value of supply, place of service and time of supply can arise. Rate of GST has been decided by GST council will be i.e.5%, 12%, 18% and cap rate will be 28%.Now we should wait for clarification on the issue of rate, value of supply and prepare to face the some other issue.

(Author is Tax Consultant (indirect tax) with Sanjay Sabran & Comapany and can be reached at CAAMITDHAMA@GMAIL.COM)

Author Bio

what is the GST rate if works contract is fixed under 12% when it got revised to 18%