Understand the nuances of Tax Invoices and Bills of Supply in GST. Learn who can issue them, when to issue, mandatory requirements, and key precautions to ensure compliance.

What are a Tax Invoice and Bill of Supply? Who can issue it?

Tax Invoice: A tax invoice should be issued by a registered person who is supplying taxable goods or services or both and also charges GST from the customer. A tax invoice shows the GST rate charged on the goods and services supplied and allows the seller to collect GST from his buyers, as well as claim ITC on GST paid to his suppliers.

Bill of Supply: A bill of supply should be issued instead of a tax invoice in case a registered person supplying exempted goods or services or both or a registered person is paying tax the under composition scheme. A bill of supply does not contain any tax amount as the seller cannot charge GST to the buyer. A bill of supply is evidence of tax-free supply and the taxes cannot be collected from the buyer of goods or services.

When to issue these two documents?

Tax Invoice in respect of Goods:

| Section 31 (1) | A registered person supplying taxable goods shall issue a tax invoice. The invoice shall be issued before or at the time of removal of goods for supply to the recipient. Where the supply does not involve the movement of goods, the invoice shall be issued when goods made available to the recipient. |

Tax Invoice in respect of Service:

| Section 31 (2)

|

A registered person supplying taxable services shall, before or after the provision of service but within a prescribed period, issue a tax invoice, showing the description, value, tax charged thereon and such other particulars as may be prescribed |

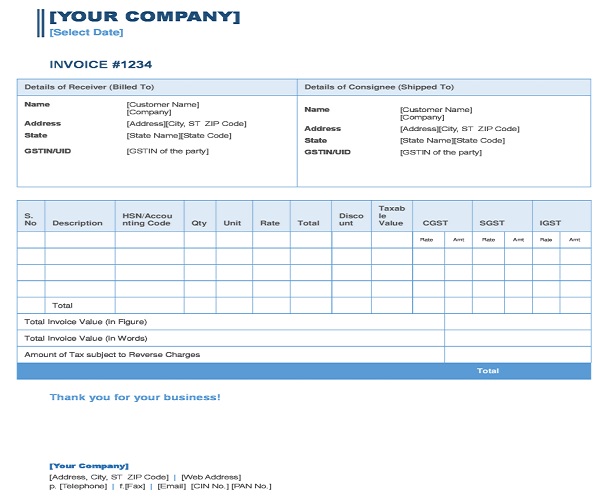

What is the Mandatory Requirement in an Invoice?

- Name, Address, and GSTIN of the Seller

- Name, Address, and GSTIN of the Buyer

- HSN code or SAC for goods and services

- Invoice number, (Should be Serially numbered)

- Date of Invoice

- Description of the Goods/Services

- Quantity of goods (Ex: Metre, kg etc.)

- Taxable value of supply

- Applicable rate of GST (Rates of CGST, SGST, IGST, UTGST, and Cess clearly mentioned)

- Total value of supply of Goods/Services

- Place of supply/delivery address and name of the destination

- Whether GST is payable on a reverse charge basis

- Signature of the supplier or his authorized representative

What care should be taken while issuing the Invoice?

- Verify customer details: Before issuing a tax invoice, it is essential to verify the customer’s details such as their name, address, GSTIN, and other relevant details to ensure that the invoice is issued to the right recipient.

- Include all mandatory details: The tax invoice must include all the mandatory details such as the name and address of the supplier, the customer’s name and address, the invoice number, the date of issue, the description of the goods or services provided, the quantity, the price, the GST rate and amount, and any other applicable taxes.

- Ensure compliance with GST laws: It is crucial to ensure that the tax invoice complies with the applicable GST laws and regulations, including the correct calculation of GST, the correct tax rate, and the appropriate classification of goods and services.

- Issue the invoice in a timely manner: A tax invoice should be issued as soon as possible after the goods or services have been supplied, preferably within 30 days of the supply.

- Maintain records: It is important to maintain records of all tax invoices issued, including the invoice number, date of issue, customer details, and the amount of GST collected.

- Signature on Invoice: It is important the tax invoice is signed by the supplier or the person in charge. A signed invoice represents the authenticity of the invoice.

Conclusion

In conclusion, the concept of tax invoices under the GST Act is an important component of the taxation system in India. It is a legal document that contains all the necessary details. Moreover, it is the basic document to claim the input tax credit in India.

Author Bio

Consultancy fees paid to CA and CA issue Bill without Gst to me(registered person)

Ca is also registered person and I will pay gst under RCm or ca is responsible to collect tax and deposit the same

who is responsible to deposit tax to govt?

if book entry without gst is it responsible for penalty?

Sir, my query is that – Say, I have provided a service to my client (who is unregistered) of a value amounting Rs 180, in a particular tax period. Since, the value of supply is less than Rs 200, as per GST law, there is no need to issue a tax invoice but issue a bill of supply instead. If I issue a bill of supply I won’t be able to collect GST on such supply, from my client. So, in such a case, do I need to pay GST on the supply above, on an inclusive basis ??? Out of my own pocket ??

Please resolve this query. Thanks.. !

I’m a buyyer of scrap Iron.

sending the scrap to rerolling factory near to me.

after meeting process is completed, the shape of the scrap transformed to flat shape and transport to my store for resale purpose.

in this case, how to raise the invoice?

please suggest.

TAVIDISETTY LAXMI NARAYANA

t.laxman96@gmail.com

9849057228 ( WhatsApp)

If you are buying the scrap from a registered dealer he will issue the invoice,. If you are buying from an unregistered dealer, you should issue a payment voucher for the purchase. On receipt of the processed goods, on sales if you are a GST registered person you should raise tax invoice if not registered bill of supply.

A Share broker, who has been providing demat services also to his customer, is neither issuing a Bill of Supply nor Tax Invoice to demat customers. Please advise in the matter.

Sir only banking company, NBFC, GTA have some relaxation in invoicing. But others are required to issue the invoice (Tax invoice/BOS) to the recipient of service for consideration.