Explore the E-Invoice era in India under the GST regime. Learn about the applicability, threshold limits, and footprints of the E-invoicing system. Discover the process of generating E-invoices, exemptions, QR code requirements, and consequences of non-compliance. Gain insights into the types of documents covered and the mandatory data embedded in the QR code. Stay informed about the cancellation process, penalties for non-compliance, and the significance of E-invoices for businesses with turnovers exceeding specified limits.

E-invoices typically contain the same information as traditional invoices, such as the details of the goods or services provided, the amounts charged, and the payment terms. However, e-invoices are more efficient and secure than paper invoices, as they can be processed automatically, reducing the risk of errors and fraud. E-invoicing is becoming increasingly popular in B2B transactions as it helps streamline the invoicing process, reduce costs, and improve cash flow.

Applicability of E-invoicing.

The threshold limit for issuing E-Invoicing was reduced from Rs.10 Crores to Rs.5 Crores effective from 1st August 2023. Any person having turnover in excess of Rs.5 Crores during any of the Financial Years commencing from 2017-18 would now be required to generate invoices electronically.

The GST Network released an advisory on 12th April 2023 notifying taxpayers with Annual Aggregate Turnover equal to or more than Rs.100 crore must report invoices on the Invoice Registration Portals within 7 days of the date on the invoice only. Others can generate e invoices beyond 7 days. However, they have deferred the time limit of 7 days to 3 months as per the latest advisory released on 6th May 2023.

Foot Prints of the Limit

| Sl No. | Aggregate Turnover | Applicable Date | Notification No. |

| 1 | More than Rs. 500 crore | 01-10-2020 | 61/2020 – Central Tax

70/2020 – Central Tax |

| 2 | More than Rs. 100 crore | 01-01-2021 | 88/2020 – Central Tax |

| 3 | More than Rs. 50 crore | 01-04-2021 | 5/2021 – Central Tax |

| 4 | More than Rs. 20 crore | 01-04-2022 | 1/2022 – Central Tax |

| 5 | More than Rs. 10 crore | 01-10-2022 | 17/2022 – Central Tax |

| 6 | More than Rs. 5 crore | 01-08-2022 | 10/2023 – Central Tax |

How to generate E-invoice?

There are various methods to generate e-invoice, one of the method is explained as follows:

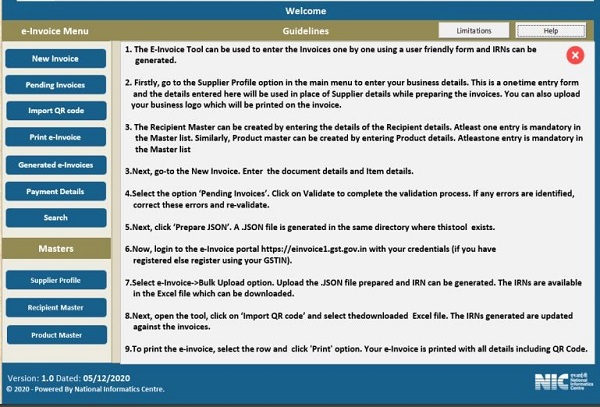

Step1: Registration

- Login to https://einvoice1.gst.gov.in/ > Registration > Portal Login > Enter GSTIN > Captcha > Go > send OTP > enter the OTP > verify

- Set User Name and password > Save

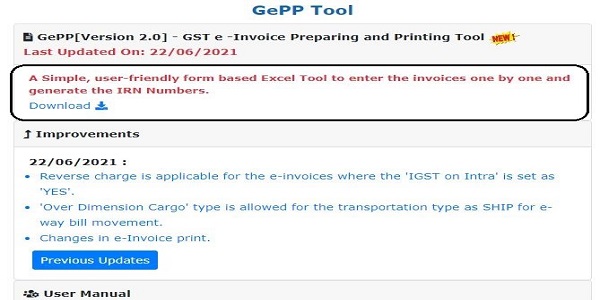

Step 2: Download the E-Invoice generation tool

A Simple, user-friendly form based Excel Tool to enter the invoices one by one and generate the IRN Numbers

- Login to E-invoing site > Help > Tools > Bulk Generation Tools > download GePP tool > fill the details > Submit

- Instructions for using the tool has been explained in the ‘Help’ button available in Home page of the Tool

- After verification a unique IRN will be generated and E-invoice JSON will be updated with digital signature and a QR code

- Invoice JSON will be shared with GST system and E-way bill system for auto population of GST return.

Who are exempted from generating e-invoice?

- Insurance Company

- Banking Company or a Financial Institution, including a Non-Banking Financial Company (NBFC)

- Goods Transport Agency (GTA) transporting goods by road in a goods carriage

- Transport service provider, providing passenger transportation service

- The registered person providing services of – admission to an exhibition of cinematograph films in multiplex screens

- Special Economic Zone (SEZ) units

- Free Trade & Warehousing Zones (FTWZ)

E invoice required for B2C?

E-invoicing is applicable only to B2B invoices and not to B2C invoices. Thus, B2B invoices require both e-way bills and e-invoices, whereas B2C invoices only require e-way bills to be generated (wherever e-way bill is applicable).

Is QR code mandatory for B2C invoices?

As per GST Notification No. 14/2020, the B2C QR Code is mandatory on invoices for taxpayers having annual turnover more than of Rs.500 Cr in any preceeding financial year from 2017-18. It came into effect on December 1, 2020 after amending the initial date of October 1, 2020 by GST Notification No. 71/2020.

What data is embedded in the QR code?

The QR code contains the following data:

- GSTIN of supplier and recipient

- Invoice Number

- Date of generation of invoice

- Document type

- Invoice value

- Number of line items

- HSN code

- Unique IRN

- Date of generation of the IRN

What are the types of documents that are to be reported to the IRP?

The following documents will be covered under e-Invoicing:

- Tax invoice

- Credit Note

- Debit Note

What is an invalid or incorrect e-invoice?

- If the e-invoice generated is not as per the standard e-invoice format or does not have one or more mandatory fields required as per the government.

- The e-invoice generated is duplicate of earlier invoice against which IRN is generated.

- Supplier or recipient GSTIN is inactive or invalid.

- Based on the updates issued on April 12th and April 13th, 2023, it is now mandatory for taxpayers with a turnover of Rs. 100 crore or more to submit invoices and credit-debit notes to the Invoice Registration Portal (IRP) and generate e-invoices within a period of 3 months from the invoice date, starting from May 1st, 2023. Failure to comply with this requirement will render these invoices non-compliant.

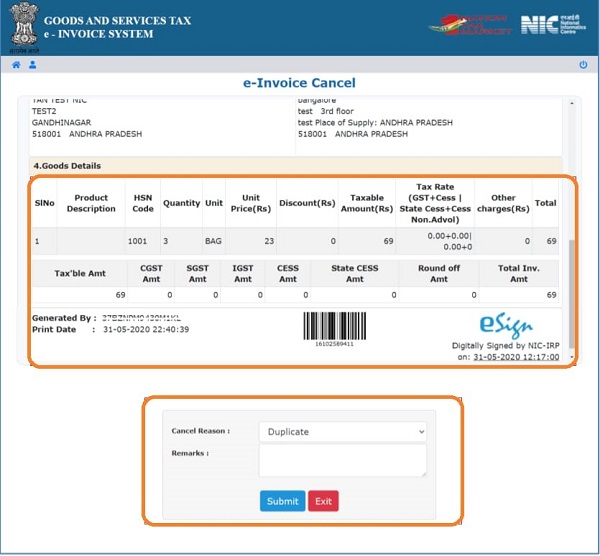

What is the time limit for cancelling e-invoice?

E-invoice is required to be cancelled within 24 hours from the time of generation. Once cancelled, the same document having same document number cannot be reported again for generation of IRN.

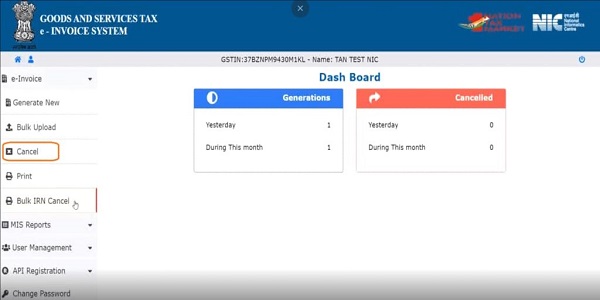

How to cancel e-invoice?

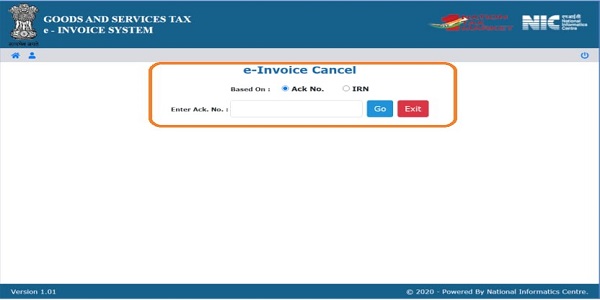

- Step 1: Log in to the e-invoice portal and select e-Invoice -> Cancel

- Step 2: Select Ack No. or IRN as applicable and enter the number. Click Go to proceed.

- Step 3: The system will display the e-Invoice and ask the user to select the reason for cancellation. To cancel the e-Invoice, click Submit.

What is the penalty for e-invoice?

According to rule 48(5) of the CGST Rules, if an Invoice Reference Number (IRN) or e-invoice is not generated, it will be regarded as a failure to issue an invoice. In such cases, penalties will be imposed as outlined below:

- Penalty for non-issuance of invoice: 100% of the tax due or Rs.10,000/- (whichever is higher) will be imposed for each instance of non-compliance.

- Penalty for incorrect invoice: Rs.25,000/- will be imposed per invoice

- If goods are transported without a valid invoice, the relevant department has the authority to detain both the goods and the vehicle. Penalties may be imposed in such cases.

- Additionally, it is important to note that without a valid Invoice Reference Number (IRN), the generation of an E-Way Bill (EWB) will not be possible. This can lead to further penalties associated with EWB non-compliance.

Conclusion:

In conclusion, we can say that E-invoice is a significant document mandated by the government if the turnover of a business exceeds a specified limit as stated above.

*****

Article By: Mr Irfan Ahammed [Intern @ NRSR & Co Chartered Accountants Manipal Udupi]

Author Bio