INTRODUCTION

Under the Goods and Services Tax regime, the law and the rules in respect of mess services received by the students from the educational institutions have been legislated based on identical jurisprudence used under the erstwhile Finance Act 1994. But unforeseen circular, which is contradictory to the notification issued, has created chaos.

The basic law as mentioned in Notification No. 12/2017- Central Tax (Rate) dated 28th June 2017 is that Services provided –

(a) by an educational institution to its students, faculty and staff; is exempt.

(b) to an educational institution, by way of,-

(i) transportation of students, faculty and staff;

(ii) catering, including any mid-day meals scheme sponsored by the Central Government, State Government or Union territory;

(iii) security or cleaning or housekeeping services performed in such educational institution;

(iv) services relating to admission to, or conduct of examination by, such institution; upto higher secondary.

The most significant element to be noted is (b) shall be applicable only to the institution providing services by way of pre-school education and education up to higher secondary school or equivalent and not to other educational institutions.

So it is clear that any service received by an educational institution other than those institution providing services by way of pre-school education and education up to higher secondary school or equivalent shall pay tax for services received as provided in (i) to (iv) of (b) stated above.

Thus from the above, it appears that the obstacle is faced by the educational institutions providing services by way of-

- education as a part of a curriculum for obtaining a qualification recognised by any law for the time being in force; ( most of the University and College’s are covered)

- education as a part of an approved vocational education course.

Thus in this article, the problems faced by the students of University and College which are covered within the meaning of educational institution are discussed.

NOTIFICATIONS

| The Board vide Notification No. 12/2017- Central Tax (Rate) dated 28th June 2017, Sl. No.66, Heading 9992, states that Services provided by an educational institution to its students, faculty, and staff; is exempt. |

Analysis

Therefore from the above notification, it is clear that GST shall not be collected by an educational institution for services provided by it to its students, faculty, and staff.

The term educational institution has been defined as-

“educational institution” means an institution providing services by way of,-

(i) pre-school education and education up to higher secondary school or equivalent;

(ii) education as a part of a curriculum for obtaining a qualification recognised by any law for the time being in force;

(iii) education as a part of an approved vocational education course;

| The Board vide Notification No. 46/2017-Central Tax (Rate) dated 14th November 2017 states that supply of food or any other article for human consumption or drink, provided by a restaurant, eating joint including mess, canteen, shall be taxable at 5%, other than those located in the premises of hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes having declared tariff of any unit of accommodation of seven thousand five hundred rupees and above per unit per day or equivalent, provided that credit of input tax charged on goods and services used in supplying the service has not been taken. |

Analysis

So it is understandable from the above notification that the mess or canteens outsourced contractor shall collect 5% GST from the educational institution for the service supplied provided that he shall not avail the benefit of Input Tax Credit.

CIRCULAR

| The Board, provided Clarifications regarding GST on College Hostel Mess Fees vide Circular No. 28/02/2018-GST dated 08th January 2018,

The educational institutions have mess facility for providing food to their students and staff. Such facility is either run by the institution/ students themselves or is outsourced to a third person. Supply of food or drink provided by a mess or canteen is taxable at 5% without Input Tax Credit [Serial No. 7(i) of Notification No. 11/2017-Central Tax (Rate) as amended vide Notification No. 46/2017-Central Tax (Rate) dated November 14, 2017 refers]. It is immaterial whether the service is provided by the educational institution itself or the institution outsources the activity to an outside contractor. |

Catch – 22 Notification and the Circular

Circular No. 28/02/2018-GST dated 08th January 2018, states, it is immaterial whether the service is provided by the educational institution itself or the institution outsources the activity to an outside contractor, the educational institution shall collect 5% without Input Tax Credit, thus the circular is in contrary to the Notification No. 12/2017- Central Tax (Rate). Whereas the notification states services provided by an educational institution to its students, faculty, and staff is exempt.

Since there is ambiguity among the notification and the circular, a couple of authorities had been referred,

[State of Madhya Pradesh & Anr. vs. G.S. Dall & Flour Mills (1991) 187 ITR 478 (SC)] has held that a circular or a direction cannot be permitted to curtail the provisions of the Act. They cannot curtail the statute or whittle down its effect. Instructions cannot cut down the scope of a notification prescribing qualifications for a certain exemption.

The Hon’ble Supreme Court pronounced its decision in the case of M/S. Sandur Micro Circuits Vs Commissioner of Central Excise, Belgaum ( 2008-TIOL-148-SC-CX) that, the issue relating to effectiveness of a circular contrary to a Notification statutorily issued has been examined by this Court in several cases. A Circular cannot take away the effect of Notifications statutorily issued.

And hence when there is a conflict between a notification and a circular, the notification shall prevail.

PRACTICE FOLLOWED BY THE UNIVERSITY OR COLLEGES

The practice followed by the University or College is analysed in detail,

Transaction – 1

Analysis of T1,

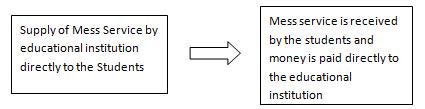

The University or College itself provides mess facility to the students, faculty, and staff, in this transaction,

a. If the Notification is followed, then no GST shall be collected by the educational institution from the students,

b. If the Circular is followed, then 5% GST shall be collected by the educational institutions from the students, there would be an increase of mess fee by 5%.

Transaction – 2

Analysis of T2,

The University or College outsources the supply of food to a contractor; the educational institution collects the fee and then pays it to the contractor,

In this situation when the food is supplied by the contractor, the contractor as per Notification No. 12/2017- Central Tax (Rate) collects 5% GST from the educational institution. As per the Notification No. 12/2017- Central Tax (Rate), the educational institution is not entitled to collect GST from its students, faculty, and staff. And, since majority of the service provided by the educational institution is exempt, it wouldn’t have any taxable output and the inputs are taxable and therefore the 5% GST paid to the contractor becomes cost for the educational institution, indirectly the educational institution hikes the mess fee and ultimately the students suffer and the Sl. No.66, Heading 9992, Notification No. 12/2017- Central Tax (Rate), becomes otiose.

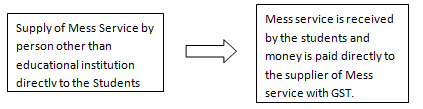

Transaction – 3

Analysis of T3,

The mess facility is being provided to the students directly by the mess who is other than the educational institution and the mess fees are directly collected by the supplier from the students, in this situation, the supplier collects 5% GST from the students.

COMPOSITE SUPPLY

When the educational institution itself having mess facility for providing food to their students and staff runs the mess facility and it charges the mess fee as onetime payment along with the tuition fee, then it becomes a composite supply, here the tuition fee charged for providing education is the principal supply which is an exempt supply and the restaurant service provided is ancillary supply, thus no GST shall be collected for the mess facility provided.

Now the question is whether the mess service provided by the college amounts to a composite supply when the mess fee is collected along with the tuition fee?

In the absence of Indian authorities on the question whether GST is applicable on the mess service provided by the college, guidance may be derived from the judgments of European Court of Justice (“ECJ”) on the same.

Brockenhurst College v Revenue and Customs Commissioners, [2017] EUECJ C-699/15

The issue before the ECJ was whether VAT was applicable to the restaurant services provided by the college. The ECJ held that such activities could be regarded as supplies ‘closely related’ to the principal supply of education, provided that those services were essential to the students’ education and that their basic purpose was not to obtain additional income for that establishment by carrying out transactions which were in direct competition with those of commercial enterprises liable for VAT. The Court noted that services offered in the present case, as part of the courses taught to its students, to a limited number of third parties, were substantially different from those habitually offered by a commercial restaurant and were aimed at a different public and the intention was not to generate additional income. Therefore, the ECJ held that the principal supply was that of education and the restaurant and entertainment services provided by the college were ancillary to this principal supply.

MISSING – “FACULTY”?

A clarification is required regarding “faculty”, the Notification No. 12/2017- Central Tax (Rate) states service provided by an educational institution to students, faculty, and staff is exempt, but the Circular No. 28/02/2018-GST, the term “faculty” has been omitted and only students and staff have been mentioned.

Clarification is required regarding whether the exclusion of the word faculty is a clerical error or whether it was the intention of the legislature to eliminate the term faculty or whether staff and faculty are to be considered one and the same?

SUGGESTIONS

1. To attain the real purpose of the exemption provided to the students in the law, under Notification No. 12/2017- Central Tax (Rate).

The benefit of exemption available to the pre-school and up to higher secondary school or equivalent, the same exemption should also be provided to the higher education providers such as universities and colleges.

If this benefit is provided to the Universities and Colleges then the Mess service received by them from an outsourced contractor would be an exempt supply and further it would not be a cost to the Universities or Colleges and the burden wouldn’t fall upon the students.

2. The board shall ensure that in future the circulars issued shall not be in contrary to the notifications as well the law.

CONCLUSION

To summarize, it is a paradoxical situation for the educational institutions whether to follow the notification or the circular where both are contradictory to each other. If very soon a clarification is not being provided, the educational institutions would charge 5% GST from the students, staffs, faculties, which is legally as well as ethically wrong. So it would be a kind act of the board to withdraw the circular and provide clarifications regarding it.

If a proper clarification is not provided in due course, then the notification stating exemption would be otiose.