INTRODUCTION :-

A major concern for businessmen registered under GST is to avail Tax Benefit & Input Credit of Old Regime. In order to avail such benefit, a registered person is required to file TRAN-1 Within 90 days (28th Sep 2017 )of the appointed day, that is 01 July 2017.

Those who desirous of availing such credits for tax payment for the month of f July 2017, need to furnish TRAN-1 before filing Form 3B. For such person, date of furnishing TRAN-1 is 28th Aug 2017.

Step by step guidelines for filing of TRAN-1 according to dashboard of GSTN Portal will be certainly useful for businessmen and other registered person filing this return.

An attempt has been made to present it in easy to understand and self explanatory fashion.

TRAN 1 – TRANSITIONAL ITC / STOCK STATEMENT

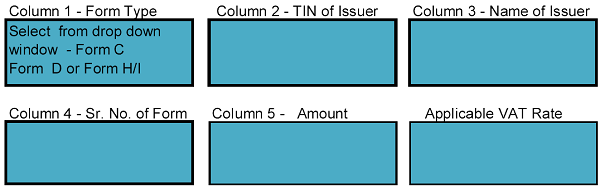

![]() (Column 1 , 2 & 3 of TRAN 1 will be auto populated on login in GST Portal)

(Column 1 , 2 & 3 of TRAN 1 will be auto populated on login in GST Portal)

TABLE 4 – . Whether all the returns required under existing law for the period of six months immediately preceding the appointed day have been furnished

TABLE 4 – . Whether all the returns required under existing law for the period of six months immediately preceding the appointed day have been furnished

(A registered person is not eligible for claiming transitional credit unless the answer for Table 4 above is YES – Sec 140(1)(ii) of GST Act 2017)

First page of GST Portal indicates the summary content of Table 5 to Table 12 of this Return .Click on each table, which will open the page where all required details need to be entered.:-

The explanatory notes and actions to be taken for each table are enumerated in succeeding paragraphs. The explanatory notes are given as footnote under each table

TABLE 5 – TAX CREDIT FORWARD IN RETURN FILED UNDER EXISTING LAW.

(Existing law means law which were prevailing in pre-GST regime implementation and subsumed in GST, i.e. Service Tax , VAT etc).

TABLE 5 (a) – The details need to be entered in following columns :-

Note (i) Section 140(1) of GST Act states that Registered taxable person shall be eligible to take credit of CENVAT CREDIT /VT -ITC carried forward in the return, furnished for the period, immediately preceding the appointed day ( 01 Jul 2017) subject to following conditions:-

(i) The said amount is admissible as ITC under this Act

(ii) The registered person has furnished the returns required under existing law ( pre-GST law i.e. service Tax , VAT etc) for the period of six months immediately preceding the appointed date (01 July 2017)

(iii) The said amount of credit does not relate to goods sold as exempted goods under relevant Government Notification in prevailing law at that point of time

Note (ii) Section 140(4)(a) states that any registered person who was engaged in supply of goods and services which were exempted ,in previous tax regime and such exempted goods & services have become taxable under GST Act , is eligible to take CENVAT credit . The said credit can be claimed to the extent of amount carried forward in returns furnished under pre-GST Law (i.e. Service Tax , VAT etc.)

TABLE 5 (b) DETAILS OF STATUTORY FORMS (‘C’ FORM ,’F’ FORM , ‘H/I’ FORM RECEIVED FOR WHICH CREDIT IS BEING CARRIED FORWARD:-.

Details in Table 5(b) need to be entered in following columns :-

TABLE 5(c) AMOUNT OF TAX CREDIT CARRIED FORWARD AS STATE/UT TAX

Details in Table 5(c) need to be entered in following columns :-

Footnote (i) – In pre- GST regime, Form C, F & H/I were to be issued for concessional tax rate on interstate supply , stock transfer & Import-export respectively. In case of non availability of these concessional forms in respect of business transaction, difference between normal tax rate and concessional tax rate is required to be paid by registered person. This amount need to be entered in Column 4 ,6 & 9 respectively of table 5 c.

Footnote (ii) – Column 2 indicates CENVAT credit carried forward from pre-GST returns, during that period tax person should have availed credit against Form C, F,& H/I as the case may be ,and still these Forms are not received from buyer. Credit allowed for these form need to be reversed by indicating ITC reversible amount in column 7. Further , difference between normal tax rate and concessional tax is required to be paid and entered in column 4,6 &9 above. Net eligible ITC amount is arrived by column 2- (4+6+9-7) and will be entered in Column 10.

TABLE 6 – DETAILS OF CAPITAL GOODS FOR WHICH UNAVAILED CREDIT HAS NOT BEEN CARRIED FORWARD UNDER EXISTING LAW UNDER SECTION 140(2),

Sec 140 (2) states that a registered person shall be entitled to take credit on capital goods which was not carried forward in return filed under earlier law or Act..The only condition is that transferred ITC is eligible as credit both under earlier law as well as under GST.

Unavailed Central tax CENVAT credit in respect of Capital goods. Details required to be entered in Table 6 (a) under following columns :-

TABLE 6(b) UNAVAILED STATE TAX CENVAT IN RESPECT OF CAPITAL GOODS

Details required to be entered in Table 6 (b) under following columns :-

TABLE 7 – DETAILS OF INPUT HELD IN STOCK IN TERMS OF SEC 140(3), 140(4)(b) and 140(6).

TABLE 7(a) AMOUNT OF DUTIES AND TAXES ON INPUT CLAIMED AS CREDIT. Details required to be entered under following columns:-

TABLE 7 (b) – AMOUNT OF ELIGIBLE DUTIES AND TAXES /VAT/ET IN RESPECT OF INPUTS OR INPUT SERVICES UNDER SEC 140(5)

Sec 140(5) applies where inputs/input services received on or after the appointed day whereas the applicable duty/tax paid by the supplier under the earlier law. CENVAT credit in respect of such inputs shall be eligible subject to condition that invoice or duty paying documents has been recorded in the books of account within thirty days from the appointed day.

Details in Table 7b are required to be filled in following columns :-

TABLE 7 (c) – AMOUNT OF VAT AND ENTRY TAX PAID ON INPUTS SUPPORTED BY INVOICES /DOCUMENTS EVIDENCING PAYMENT OF TAX UNDER SEC 140(3), 140(4)(B) AND 140(6).

Section 140(3) states that any registered person who was engaged in manufacturing of exempted goods or provision of services & work contracts and said goods and services which have become taxable under GST Act, is eligible to claim ITC in respect of tax paid amount included in value of raw material stock, work In Progress or final products as on the date immediately preceding the appointed date (As on 30th June 2017).

Section 140(4)(b) states that any registered person who was engaged in manufacturing of exempted goods or provision of services & work contracts and said goods and services which have become taxable under GST Act, is eligible to claim ITC in respect of tax paid amount included in value of stock in semi finished or finished goods as on the date immediately preceding the appointed date. (30 June 2017)

Section 140(6) states that any registered person who was paying tax in the capacity of composite tax payer at a fix rates and become regular registered person, is eligible to claim ITC in respect of tax paid amount included in in stock, WIP or in final products as on the appointed date. (30 June 2017)

Details of such payments required to be filled in following columns :-

TABLE 7(d) – STOCK OF GOODS NOT SUPPORTED BY INVOICES /DOCUMENTS EVIDENCING PAYMENT OF TAX.

Details of input in stock are required to be provided in following columns :

CONCLUSION :- In conclusion, the approach adopted above is to put in place the procedure to be followed, the governing sections and the methodology to be adopted to avail Transitional credit while migrating from prevailing Tax regime to GST regime. Care has been taken to avoid complicated terminologies, so that the readers of this article understand the concept easily.

Any further queries , clarifications – assistance can be given to those who seek. The same may be e-mailed to 1706 anita@gmail.com

Author Bio