Here, we will mainly discuss the common Departmental Audit undertaken under Section 65 of the CGST Act.

Audit under GST serves as the foundation of compliance monitoring. It ensures that taxpayers have paid the correct tax, claimed eligible Input Tax Credit (ITC), and complied with other provisions of the law.

(a) Types of GST Audits

1.Departmental Audit (Section 65): Initiated by the Commissioner or an authorized officer based on risk assessment or turnover thresholds. Conducted at the taxpayer’s premises or at the tax office.

2. Special Audit (Section 66): Directed by authorities when the nature of transactions is complex. Conducted by a Chartered Accountant or Cost Accountant nominated by the Commissioner

(b) Step-wise Audit Process

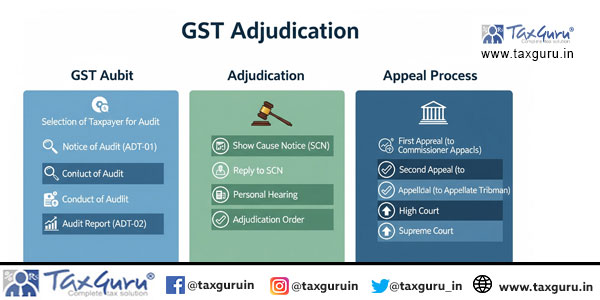

1.Notice Issuance (Form GST ADT-01): Authorities notify the taxpayer and request submission of records.

2. Examination of Records: Books of accounts, invoices, ITC registers, e-way bills, contracts, and returns (GSTR-1, GSTR-3B, GSTR-9, GSTR-9C) are scrutinized.

3. Audit Findings (Form GST ADT-02): Discrepancies, if any, are communicated to the taxpayer for explanation.

(c) Taxpayer Strategy

- Periodic Reconciliation: Periodic reconciliation of outward supply and ITC with GSTR-2B prevents disputes.

- Voluntary Payment: If discrepancies are genuine, paying tax and interest under Section 50 through Form DRC-03 before initiation of adjudication avoids penalties.

- Advance Planning: Maintain detailed working papers for ITC, contracts, and reconciliations to respond quickly.

2. GST Adjudication – determination of demand

Adjudication is the process of determining the actual tax liability when discrepancies remain unresolved.

(a) Legal Provisions

1.Section 73: For non-fraud cases such as short payment, non-payment, or incorrect ITC claims without intent to evade tax.

2. Section 74: For fraud/suppression cases involving willful misstatement or intent to evade tax.

(b) Step-wise Process

1.Show Cause Notice (SCN): Issued under Section 73 or 74 specifying the nature of demand (Form DRC-01).

2. Pre-SCN Payment Options:

-

- Section 73 cases: If tax + interest is paid before SCN, no penalty applies.

- Section 74 cases: If tax + interest is paid before SCN, a 15% penalty applies (lower than later stages).

3. Reply & Hearing: Taxpayer files a detailed reply, supported by reconciliations, documents, and legal precedents. A personal hearing is granted.

4. Adjudication Order (Form DRC-07): Final demand order is issued.

(c) Taxpayer Strategy

- Opt for Pre-SCN Payment: This saves penalty and closes the matter quickly.

- Cash Flow Management: Set aside funds for voluntary payment, reducing interest and penalty exposure.

- Strong Documentation: Contracts, agreements, invoices, and reconciliations strengthen defense.

3. GST Appeal – Structured dispute resolution

If taxpayers disagree with the adjudication order, they can approach the appellate mechanism.

(a) First Appellate Authority (Section 107)

- Appeal must be filed within 3 months of receiving the adjudication order.

- Mandatory Pre-Deposit:

- 100% of admitted tax liability.

- 10% of disputed tax liability.

(b) Appellate Tribunal (Section 109 / 112)

- Appeal against the order of the First Appellate Authority.

- For filing an appeal before the Appellate Tribunal, an additional pre-deposit is required so that the total comes to 20% of the disputed tax.

(c) Higher Appeals

1.High Court (Section 117): On substantial questions of law.

2. Supreme Court (Section 118): Further appeal on significant matters.

(d) Case Law Reference

- Canon India Pvt. Ltd. (2021): Reinforced jurisdictional discipline in issuance of SCNs.

- M/s Magma Fincorp Ltd. v. State of Jharkhand (2020-VIL-266-JHR): High Court observed that pre-deposit requirements are mandatory but protect taxpayers from coercive recovery.

- Armour Security (India) Ltd. v. Commissioner, CGST [2025-VIL-63-SC]: Supreme Court clarified parallel proceedings, balancing investigation powers with protection against duplication.

(e) Advance Planning for Appeals

- Cost-Benefit Analysis: Assess cost of litigation versus tax liability.

- Provisioning: Pre-deposits can lock working capital; provision for funds in advance.

- Strategic Timing: Evaluate whether voluntary compliance at the adjudication stage is better than prolonged litigation.

4. Use of Tax and Interest payment to save penalty

Timing of payment plays a crucial role in saving penalties and avoiding prolonged disputes:

1.During Audit: Voluntary payment via DRC-03 helps close issues.

2. Before SCN (Section 73/74): Saves penalty or significantly reduces it.

3. During Adjudication: Payment before the order reduces litigation risk.

4. Before Appeal: Pre-deposit of admitted tax + disputed tax percentage avoids further coercive recovery.

5. Practical guidelines for advance planning

- Maintain Real-Time Reconciliation: Between books, returns, e-way bills, ITC claims, and appearing in GSTR-2B.

- Payment of Tax on Advances Received: Against supplies of services and adjustment in invoices with tax thereon.

- Create GST Litigation Reserves: Separate provisioning for potential disputes.

- Regular Legal Health Checks: Engage professionals to conduct internal GST reviews.

- Documentation Discipline: Maintain proper contracts, invoices, and digital records.

- Strategic Decision-Making: Sometimes paying disputed liability is more cost-effective than prolonged appeals.

6. Illustrative Case Studies

1.Non-Fraudulent ITC Mismatch: A taxpayer reconciled ITC late, voluntarily paid tax + interest before SCN under Section 73, and avoided penalty.

2. Fraud Case Allegation: A business accused of suppression opted for pre-SCN payment with 15% penalty, which was far less than the 100% penalty that could have been levied later.

3. Appeal Planning: A company facing a disputed liability of ₹1 crore deposited 10% (₹10 lakh) at First Appeal and an additional 10% (₹10 lakh) at the Tribunal stage. By advance provisioning, it avoided liquidity shocks.

The journey of a GST taxpayer through Audit, Adjudication, and Appeal is not merely a legal process but a strategic financial decision-making path. Proactive reconciliations, timely voluntary payments, and well-planned litigation strategies can reduce penalties and save resources. Pre-deposits, though unavoidable at appellate stages, can be managed with advance planning. Ultimately, businesses that view GST compliance as an ongoing strategic function, rather than a reactive burden, will benefit from reduced litigation, stronger credibility with tax authorities, and optimized financial outcomes.

Author Bio