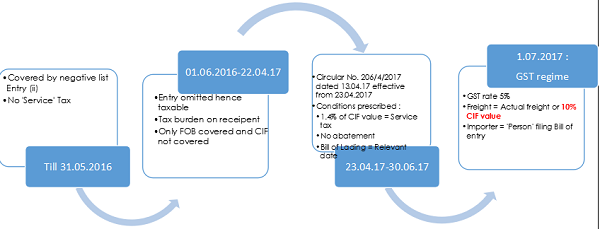

The Service regime has change from positive list to negative list w.e.f. 01-July-2012. Thereafter any services other than services which falls under the ambit of Section 66D i.e Negative list shall be subject to Service tax. Further, there was a mega exemption Notification 25/2012-Dated 20.06.2012 vide which various services were exempted and said notification has underwent various amendments from time to time. In this article, we shall discuss the Applicability of “Service tax on Ocean freight” paid along with value of goods in case of Import of goods. After the introduction of negative regime the provision related to Ocean freight underwent sea of changes which can be understood from below mentioned flow chart.

The Circular No. 206/4/2017 dated 13.04.17 effective from 23.04.2017 has resulted in catastrophe across Industry. The government vide said circular has clarified levy of service tax on the services provided by a person located in non-taxable territory to a person located in non-taxable territory, by way of transportation of goods by a vessel from a place outside India to the customs station in India.

Further, in terms of para 4 of said circular the abatement in terms of N.No.26/2012-ST dated 20.06.2012 has rendered the notification redundant and void.

The competitiveness of the market has led to stiff margins and the importer of goods are working on wafer thin margins. For instance, the pre-circular regime, importer was earning 2.5% on value of goods imported assuming Rs.1000, so the profit is Rs.25. Post-circular the importer is liable to pay 1.4 % of CIF value towards Service Tax, 0.05% Krishi Kalyan cess and 0.05% Swach Bharat cess totalling to 1.5% of CIF, in this case importer will be liable to pay Rs.15 on the import value of Rs.1000 (CIF).

Importer has suffered Rs.15 loss due to uncertainty which was never perceived by the importer pre-circular. This is classic example why this has ripple effect as the bankers would have estimated the revenue and profit on the basis of pre-circular and the very economic viability of the importer comes under threat. Therefore, the imports which are generally financed will cause NPA due to uncertainty in law. Even, otherwise the legal position of this circular which is discussed later part is not sustainable in the authors opinion.

Some pertinent questions arise on the issue which is mentioned below:

1. Whether the demand raised due to subsequent interpretation adopted in the circular is legally correct?

2. In case the demand is legally sustainable, what shall be the value on which Service tax on Ocean freight shall be payable?

3. Whether abatement in terms of N.No.26/2012-ST dated 20.06.2012 shall be available to importer ?

4. What is relevant date for computing import of Service of Ocean freight?

We shall deal the said questions in seriatim:

1. Whether the demand raised due to subsequent interpretation adopted in the circular is legally correct?

1. Amendment and juxtaposition

The provision pertaining to taxability i.e. Reverse Charge Mechanism draw its power from – Section 68(2) of Finance Act,1994 reads

“If any taxable services provided or agreed to be provided by any person who is located in a non-taxable territory and received by any person located in the taxable territory then Service tax on said service is liable to be paid by person receiving service”

Section 68(2) read with entry no 10 of N.No.30/2012-ST dated 20.06.2012 which is as below.

| Sl.No. | Description of a service | Percentage of service tax payable by the person providing service | Percentage of service tax payable by the person receiving the service |

| 10 | in respect of any taxable services provided or agreed to be provided by any person who is located in a non-taxable territory and received by any person located in the taxable territory | Nil | 100% |

Further vide N.No.16/2017-ST dated 13th April,2017 the said liability has been shifted to importer of goods into India. The amendment (i) in rule 2, in sub-rule (1), in clause (d), in sub-clause(i), for item (EEC), the following shall be substituted, namely:-

“(EEC) in relation to services provided or agreed to be provided by a person located in non-taxable territory to a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India, the importer as defined under clause (26) of section 2 of the Customs Act, 1962 (52 of 1962) of such goods;”;

In case of CIF transaction of import of goods, the shipping line provides the services to supplier of goods and actual receiver of Ocean freight service is supplier of goods and the importer is merely beneficiary of this service. In the authors opinion, the importer in case of CIF transaction cannot be said as receiver of service and therefore the provision of section 68(2) read with entry no 10 of N.No.30/2012-ST dated 20.06.2012 shall not be applicable.

ii. Dual taxation:

The importer who files Bill of Entry (BoE) before custom authority pays the CVD and SAD on CIF value in terms of Section 14 of Customs Act, 1962 read with Rule 10 of Customs Valuation (Determination of Value of Imported Goods) Rules, 2007. Once the value of freight becomes the part of value of goods then Service tax cannot be levied on same value as transaction cannot be both as “Import of goods and Import of service”.The value of Ocean freight service is already included in the CIF value and on such value duty is already paid. Hence, liability of service tax on same value tantamount to dual taxation which is against the basic spirit of law and same is legally incorrect. Further, the Government wants the importer to pay Service tax on value of Ocean freight which is otherwise included in the CIF value. This contention has been confirmed by Hon’ble Mumbai Tribunal. The relevant extract of said Judgement is as mentioned below:

In the matter of United Shippers Ltd.v/s Commissioner of Central Excise reported at [2015] 57 taxmann.com 429 (Mumbai – CESTAT) wherein

“Section 66, read with section 67, of the Finance Act, 1994 and sections 12 and 14 of the Customs Act, 1962 – Charge/levy – Service Tax – Where a transaction involves a customs transaction and a service transaction, it is necessary to decide where customs transaction ends and service transaction begins – Question of rendering any service in respect of such goods by way of cargo handling or otherwise can take place only after customs transaction is completed – Therefore, if an activity is part of import transaction leviable to import duty or some charges are includible in customs value, it cannot be charged to service tax [Paras 5.2 and 5.3] [In favour of assessee]”

Further in the matter of Commissioner v/s United Shippers Ltd. Reported at 205(39) S.T.R. J369 (S.C) the Hon’ble Supreme Court has confirmed the view of CESTAT.

Therefore this levy is undoubtedly is a tax on value which has already suffered tax and therefore it amounts to double taxation and same has been held legally incorrect by Apex court as mentioned above.

2. In case the demand is legally sustainable, what shall be the value on which Service tax on Ocean freight shall be payable?

If we presume that the Service tax is at all payable on Ocean freight service, then the next question comes whether what should be the value of such service. In terms of Section 67 of Finance Act, 1994 read with Valuation rules Service Tax (Determination Of Value) Rules, 2006then value of such taxable service shall be the gross amount charged by the service provider for such service provided or to be provided by him. In case of Ocean freight service the value of actual ocean freight charged by Service provider (shipping line)shall be the value of such service. In case the actual value of service is not available then in terms of Rule 8C of value of Service shall be actual freight paid or 10%of CIF if actual freight value is not available. The actual freight value may be obtained from shipping line for said Import of goods. The invoice of shipping line or freight certificate from shipping line may be documents for actual freight value.

Further the actual service of Ocean freight is received by Supplier of goods and Importer is no aware of any details of actual freight paid to such supplier, to comply with the condition to produce the details of actual freight is almost impossibleconditions and therefore cannot be fulfilled. This is settled law that if any condition which imposed to fulfilled the compliance of law and same is impossible then it shall presumed to be presumed to be fulfilled for the compliance of said law to that extent and reliance has been placed on below mentioned judgement.

“In the matter of SRF v/s Union of India reported at

As mentioned above the importer is left with no choice except to follow the alternate mechanism of valuation which is 10% of CIF value. The relevant extract of rules which requires to follow alternate mechanism is as mentioned below:

(ii) in rule 6,-

(a) after sub-rule (7C), the following sub-rule shall be inserted with effect from 22nd January, 2017, namely :-

“(7CA) The person liable for paying service tax for the taxable services provided or agreed to be provided by a person located in non-taxable territory to a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India, shall have the option to pay an amount calculated at the rate of 1.4% of the sum of cost, insurance and freight (CIF) value of such imported goods.”

As per industry practices it appears that the actual freight generally is 1-2% which is actually paid and this presumption costs the taxpayer almost 10 times the realistic value this pose a serious threat to many business in India.

3. Whether abatement in terms of N.No.26/2012-ST dated 20.06.2012 shall be available?

In terms of N.No. 26/2012-ST dated 20.06.2012 under entry no 10 (Amended by N.No. 8/2015 ST dated 01.03.2015) wherein the abatement of 70% is granted from taxable value of Ocean freight. Also the abatement is always available QUA VALUE and it deducted to determine the taxable value. The relevant entry is reproduced below:

| Sr. No. | Description of Taxable service | Percentage (Taxable value) | Conditions |

| 10 | Transport of goods in a vessel | 30% | “CENVAT credit on inputs, capital goods and input services, used for providing the taxable service, has not been taken by the service provider under the provisions of the CENVAT Credit Rules, 2004.” Inserted by notification 8/2016- service tax dated 1 March 2016 |

The only conditions for claiming abatement from the value of Ocean freight is that the Cenvat credit in respect of Inputs and Capital Goods should not be claimed by service provider. There is no doubt that service provider is located outside India (Taxable Territory) and Service provider is not registered in terms of Section 69 of Finance Act, 1994. Therefore the question of availing Cenvat credit doesn’t arise. The said abatement is therefore available on such service to the deemed recipient of service i.e Importer of Goods. Service tax cannot be demanded as value of freight already,however para 4 of Circular no. 206/4/2017-Service tax dated 23.04.2017 states that:

“However, in case of foreign shipping lines, their services being exports from their home country, are zero-rated in their home country and thus have suffered no taxes. Further the foreign shipping lines do not get registered in India and do not follow the provisions of Cenvat Credit Rules.”

- Rules Cannot Bypass The Act

The Supreme Court recently in Union of India v/s Inter Continental, India held that Board Circular cannot override Notification. It was held that after the notification is issued, Board cannot subsequently issue a circular and add a new condition which restricts the scope of the exemption notification. It is pertinent to note that Hon’ble Supreme Court on various occasion have held that “It is trite that rules cannot go beyond the statute.”

In Babaji Kondaji Garad v/s Nasik Merchants Co-operative Bank Ltd. (1984) 2 SCC 50., it was held that if there is any conflict between a statue and the subordinate legislation then statute will prevail over subordinate legislation. The same had been reiterated in CIT v/s S.Chenniappa Mudaliar (1969) 74 ITR 41 (SC).Further, it is also a well-established principle that Rules are framed for achieving the purpose behind the provisions of the Act as held in CIT v/s Taj Mahal Hotel (1971) 82 ITR 44 (SC)case.

- Delegation of Legislative Power is very much required however unlimited delegation may invite despotism uninhibited

In Gwalior Rayon Co v. Asst.Commissioner of Sales Tax, KHANNA,J., said:

“The rule against excessive delegation of the legislative authority flows from and is a necessary postulate of the sovereignty of the people.” The Apex Court in Registrar Coperative Societies v. K.Kanjabmu observed: “delegation unlimited may invite despotism uninhibited.”

There is no abdication of legislative functions so long as the legislature has expressed its will on a particular subject matter, indicated its policy and left the effectuation of the policy to subordinate legislation provided the legislature has retained the control in its hand with reference to it so that it can act as a check or a standard and prevent the mischief by subordinate legislation when it chooses to or thinks fit.

While it is recognized that the doctrine of excessive delegation ought not to be applied in a pedantic manner because in the modern complex world, it may be difficult for the legislature to state policies or formulate standards very articulately and power has to be given to the Administration in broad terms to make rules according to the needs of the situation.But still the courts must ensure that the doctrine does not become just an incantation or an empty formality. The statement of policies in the statutes enable the courts later to apply the doctrine of ultra vires to delegated legislation in a more meaningful and effective manner.

The above discussion clearly brings out that the circular is over reaching its judicial mandate and therefore the circular is utra vires Notification 26/2012-ST dated 20.06.2012 and legally incorrect. Further, the circular is not binding on assesse it is clarificatory in nature.Hence, the judicial review based on the precedents shows that Importer can claim the benefit of abatement and pay the tax on taxable value of 30% of Ocean freight.

4. What is relevant date for computing import of Service of Ocean freight

For discussing the relevant date it is necessary to discuss – Point of taxation rule

Point of taxation in respect of persons required to pay tax as recipients of service in respect of services notified in Section 68(2) of Finance Act 1994 would be date on which payment is made. If payment is not made within 3 months of invoice date, immediate date would be considered as point of taxation.

The question is whether the person in-charge of vessel who has been made liable for service tax payment can be considered as recipient of service though he is not receiving the service. Even if yes, the point of taxation would be date of payment for the service. In this case, no payment would be made by person in-charge of vessel.

This notification seeks to introduce a new Rule 8B in the Point of Taxation Rules, 2011 to prescribe point of taxation for the subject services. This amendment has been made with retrospective effect from 22.01.2017. The said rule lays down the Point of taxation as, 8B.

“Determination of point of taxation in case of services provided by a person located in non-taxable territory to a person in non-taxable territory.-

Notwithstanding anything contained in these rules, the point of taxation in respect of services provided by a person located in non-taxable territory to a person in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India, shall be the date of bill of lading of such goods in the vessel at the port of export.”

In our view in case of import of Ocean freight services is coming along with goods which is being imported. The services cannot be imported without or prior to importation of goods. In case of import of goods the import is considered when Bill of entry is filed, further the duty is payable at the rate prevailing on the bill of entry date. Therefore, services which is attached to transportation of goods can be termed as import into India from the date when said goods is received at Indian port and Bill of entry for home consumption is filed.

In case of Rule 8C the point of taxation is deemed to be the date of ‘Bill Of Lading’ instead of ‘Bill Of Entry’ which is arbitrary and legally incorrect.

Though the author is of the opinion that the same is not correct but the presumption if explicitly provided needs to be complied as the computation may be assumed for reference of date.

Way Forward

Investigations across country are being conducted by various Government agencies based on Circular No.206/4/2017-Service Tax dated 13.04.2017 which appears to be baseless and legally not sustainable.

- Author is of the strong view that there is no liability of Service tax on Ocean freight as same amounts to double taxation and said issue is squarely covered by Hon’ble Supreme Court Judgement.

- Further, if we presume that the Service tax is at all payable on Ocean freight then benefit of abatement is available from the value of ocean freight. Also in absence of actual freight,if the importer wish to pay tax on 10% of CIF value (Alternate Mechanism) then also the said abatement @70% in terms of N.No.26/2012-ST is available.

- In similar matter Mohit minerals Pvt. Ltd.Vs Union of India filed vide SCA No. 726 of 2018 the said issue is pending before Hon’ble Gujarat High Court. If same is decided in favour of assessee then the amount paid if any towards such liability, then same is eligible for refund.

- Further, the issue has suffered multiple amendments since introduction of negative list and also involves double taxation which is legally untenable therefore penalty should not be imposableand same can be contested before authority based on legal provisions mentioned above.

CA Abhishek Chopra practises exclusively in GST law.

Adv.(CA) Nipun Singhvi is practising Advocate before High Court and Supreme Court.

Author Bio

This is an excellent article covering the nuances of the issue in a very lucid but clear manner. Even if Mohit minerals pertain to GST exclusively, the author is an erudite on the subject. Well done.

the same ocean freight issue exists in GST also. it would have been more relevant to discuss the issue under GST context than to do a post mortem of an extinct tax 2 years ago. Also the caselaw Mohit minerals Pvt. Ltd.Vs Union of India SCA No. 726 of 2018 quoted above in under GST & not service tax.