THE FILE ENCLOSED DESCRIBES THE FULL DETAILS OF REGISTRATION (SECTION 22 TO 30) AS WELL AS COMPOSITION SCHEME (SECTION 10).

REGISTRATION UNDER GST CGST ACT, 2017

Section 22 : Person liable for Registration

Section 23: Person not liable for Registration

Section 24 : Compulsory Registration

Section 25 : Procedure for Registration

Section 26 : Deemed Registration

Section 27 : Special Provisions related to CTP & NRTP

Section 28 : Amendment of Registration

Section 29 : Cancellation or Surrender of Registration

Section 30: Revocation of Cancellation of Registration

SECTION 22: PERSON LIABLE FOR REGISTRATION

- Person whose Aggregate Turnover* exceeds the minimum threshold limit.

- Where Business of a Taxable person has been transferred(including Succession) to another person as a going concern, the later should be liable to register from the date of transfer.

- Demerger/Amalgamation of 2 Companies, Transferee shall be registered as on the date from giving effect to High Court order.

- Person who was registered under previous law (ex. VAT)

- * Aggregate Turnover – Value of all outward supplies of person having same PAN on all India Basis.

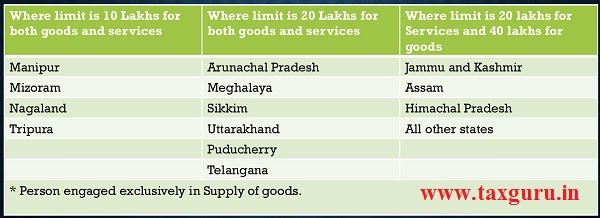

MINIMUM THRESHOLD LIMIT

SECTION 23: PERSON NOT LIABLE FOR REGISTRATION

- Person supplying goods or services which are wholly exempt or not liable to tax

- An agriculturist, to the extent of supply of produce out of cultivation of land.

- Category of persons specified by notification issued by government

♦ Person supplying such goods or services where tax is to be paid by the recipient under reverse charge

♦ Handicraft Dealers making Inter State Supply having aggregate turnover up to 20 lakhs

♦ Supplier of services who supply services through Electronic commerce operator where aggregate turnover is not exceeding 20 lakhs

♦ Casual taxable persons making taxable supplies of handicraft goods having aggregate turnover up to 20 lakhs

♦ Persons making inter State supplies of taxable services upto 20 lakhs

SECTION 24 : COMPULSORY REGISTRATION

- Person making inter state Taxable supply

- CTP making Taxable Supply

- Person who is required to pay tax under RCM

- NRTP making Taxable Supply

- Every ECO who is required to collect tax at source under section 52

- Person who is required to pay tax u/s 9(5)

- Person who is required to Deduct tax u/s 51,whether or not separately registered under the act

- persons who make taxable supply of goods or services or both on behalf of other taxable persons whether as an agent or otherwise

- Input Service Distributor whether or not separately registered under this Act

- every person supplying online information and database access or retrieval services from a place outside India to a person in India, other than a registered person

- persons who supply goods or services or both, other than supplies specified under subsection 5 of section 9 through such electronic commerce operator who is required to collect tax at source under section 52

SECTION 25 : PROCEDURE FOR REGISTRATION

- Person who is liable for registration u/s 22 or 24 – apply within 30 days of becoming liable

- CTP & NRTP – At least 5 days before commencement of business

- Single Registration for Single State however where multiple POB are there, separate registration may be granted for each POB.

- Voluntary Registration may be taken.

- Person who has obtained or person who is required to be obtained more than one registration, whether in one state or UT or more than one state of UT, then for each such registration be treated as distinct persons for the purpose of this act .

- AADHAR Authentication of the applicant mandatory from 01/04/2020 where applicant fails to undergo AADHAR authentication, the registration shall be granted only after physical verification of the principle place of business in the presence of the said person.

- PAN is required for registration but person who are required to deduct tax u/s 51 registration may be done with TAN.

- NRTP- Passport can be used for registration

- Suo moto Registration can be done by dept if person doesn’t apply for registration even when becoming liable.

- If Registration applied within 30 days of becoming liable; effective date will be, date of becoming liable, Otherwise grant of registration certificate.

- Bank account details now can be given after registration but up to 45 days from the date of grant pf registration or the date of furnishing return under section 39 (Which ever is earlier). If this provision is violated (Rule 10A) registration is liable to be cancelled. (NN 31/2019 CT dated 28.06.2019)

SECTION 26 : DEEMED REGISTRATION

- Registration under GST is not tax Specific which means there is single registration for all the taxes i.e. CGST,SGST,IGST,UTGST and cesses.

- Further Rejection of application in one tax is deemed to be rejected in all taxes.

SECTION 27 : SPECIAL PROVISIONS RELATED TO CTP & NRTP

- Certificate of registration shall be valid for a period specified in the application for registration or 90 days from the effective date of registration whichever is earlier.

- Proper officer may extend it to further period of 90 days (GST REG 11 to be filed by taxpayer)

- Advance deposition for estimated tax liability at the time of filing of application for registration and also at the time of seeking extension for further period

- Amount paid to be credited to the electronic cash ledger

- Tax to be deposited by the casual taxable person will be “estimated net tax liability” after considering ITC

- In case of long running exhibitions (for a period more than 180 days), the taxable person cannot be treated as a CTP and should seek normal registration

SECTION 29 : CANCELLATION OR SURRENDER OF REGISTRATION

- Registration can be cancelled by the person or by the dept.

- Proper officer can cancel the registration where person contravene the provisions of the act (not filed returns for continues 6 months/3 consecutive tax periods where person is composition tax payer, did not started the business within 6 months etc.)

- Following are some other points based on which registration can be cancelled:

– does not conduct business from declared POB

– Issue invoices without supply of goods or services

– violates the provisions of anti profeetering u/s171

- If there is Suo moto cancellation by dept, SCN must be given. Reply of the same should be submitted within 7 days.

- Cancellation does not affect the liability of prior period.

- Cancellation order within 30 days against the application for registration filed by RP or the date of reply and direct him to pay arrears of any tax, interest or penalty

SECTION 29 : CANCELLATION OR SURRENDER OF REGISTRATION

Rule 21 A of the CGST Rules, 2017 provides for suspension of registration in the following

manner –

- Where application is made by the RP, registration suspend from the date of application or the date from which cancellation is sought (whichever is later) till the completion of proceedings to cancellation

- Where show cause for cancellation is issued by PO, suspension form the date determined by him by granting opportunity of being heard

- When registration is suspended, no taxable supply should be done and no need to file return

- Suspension deemed to be revoked upon completion of the proceedings of cancellation by the proper officer under rule 22 and such revocation shall be effective from the date on which the suspension had come into effect

SECTION 30: REVOCATION OF CANCELLATION OF REGISTRATION

- If Registration is being cancelled by the PO then RP can apply for Revocation of registration within 30 days from service of the order, subject to some conditions.

- PO can accept or reject the revocation application,however Opportunity of being heard to be given.

- Rule 23 of the CGST Rules, 2017 provides for process of revocation of cancellation of registration and includes the following

- No application for revocation shall be filed, if the registration has been cancelled for the failure to furnish returns, unless such returns are furnished and any amount due as tax, in terms of such returns, has been paid along with any amount payable towards interest, penalty and late fee in respect of the said returns

- Upon receipt of the information or clarification, the proper officer shall proceed to dispose of the application within a period of thirty days from the date of the receipt of such information of clarification from the applicant

- Returns for the period from date to cancellation to the date of revocation of cancellation to be filed within a period of 30 days from the date of revocation Revocation of the cancellation of registration by an order in FORM REG 22

SECTION 10 : COMPOSITION LEVY

- Eligibility to opt for Composition Levy:

– Aggregate Turnover in case of Goods Supplier – 1.5 Crore( 75 lakhs in special category states except Assam, J&K, Himachal Pradesh)

– Aggregate Turnover in case of Service Supplier – 50 Lakhs

- Rate of Tax:

– Manufactures(except pan Masala, tobacco,ice cream) – 1%(0.5% CGST, 0.5% SGST) of Turnover in state(Taxable as well as Exempt)

– Food Restaurant Services – 5%(2.5%CGST, 2.5%SGST) of Turnover in state (Taxable & Exempt)

– Other – 1%(0.5%CGST,0.5%SGST)(Only Taxable Turnover)

– Other Service Supplier – 6%(3% CGST, 3% SGST) (Taxable & Exempt)

SECTION 10 : COMPOSITION LEVY

- Registered Person converted into Composition : Effective date will be Beginning of FY.

- A person supplying Goods can opt for composition if his supply of services does not exceeds 10% of the turnover in PFY or 5 Lacs, Which ever is higher.

- While computing Turnover, Interest on loans deposit will not be considered.

- Bill of Supply shall be issued in place of Tax Invoice.

- A composition Tax Payer of Goods can Supply an inter state supply of services up to 5 Lacs or 10% of turnover and still be eligible for Composition Levy. But a Supplier of Services can not make any Inter state Supplies.

- CTP/NRTP can not opt for Composition.

- Composition will be not be granted if supplies are made through ECO.

- On Notice, Signboard mention – Composition Taxable person.

- On Bill of Supply mention- Composition tax payer not liable to collect tax on supplies.