While conceptualizing concept of GST, a 3600 view of business and economy was considered specially the nature of business and requirements of almost five crore Micro, Small and Medium Enterprises (MSMEs) and small traders who account for 25% of employment, 40% of industrial output and 45% of exports of the country.

To boosting the cost competitiveness of MSMEs and small traders and for simple compliance, Composition scheme a simple and easy scheme was introduced. The scheme helps small taxpayers get rid of complex GST formalities and pay GST at a fixed rate of turnover.

Getting registered under composition scheme is optional and voluntary. As per Sec 10. (1) of CGST, a Registered Person, whose aggregate turnover in the preceding financial year did not exceed Seventy Five Lakh Rupees, (Vide notification No. 8/2017-Central Tax, dated 27.6.2017, the limit of Rs. 50 lakhs has been raised to Rs. 75 lakhs for all states except for taxable person in the north eastern states and Himachal Pradesh) may opt to pay, in lieu of the tax, a levy at a fixed rate of turnover. Though the scheme is very beneficial for small tax payers, not may are enthused to opt for the same because of some restrictive provisions.

Let us discuss in this article comparison between Normal Scheme and Composition Scheme.

Registration:

In the normal case registration is required once threshold limit of Rs 20 L (Rs 10 L in case of Special Category States) crosses as per Sec 22 of CGST Act. However under composition scheme the limit of Rs. 75 lakhs has been fixed vide notification No. 8/2017- Central Tax, dated 27.6.2017, whereas for the states of Assam, Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Tripura, Sikkim and Himachal Pradesh, the limit is restricted to Rs. 50 lakhs. But on any given day, if turnover crosses the above-mentioned limit, then it becomes ineligible under composition scheme and has to fall under the regular scheme.

Easy Compliance:

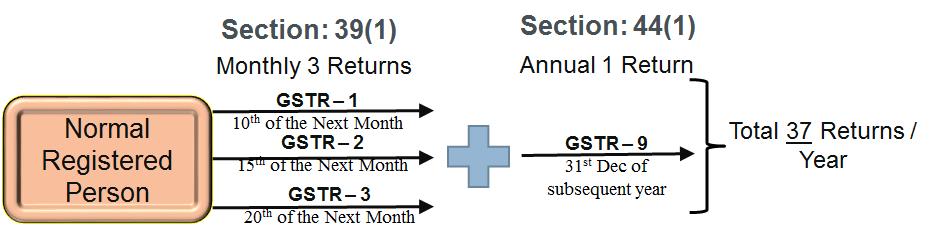

Under the normal scenario, a taxpayer under GST has to file minimum 3 returns monthly and one annual return, totaling 37 returns per annum. Whereas under composition scheme only 5 returns to be filed per year. (Return to be filed on Quarterly basis in Format GSTR-4 by 18th day after the end of each quarter [by 18th April, 18th July, 18th Oct., and 18th January- Section 39 (2) of CGST Act, 2017 and Rule 62 of CGST Rules. Annual Return to be filed in Format GSTR-9A – Section 44(1) of the CGST Act, 2017 and Rule 80 of GST Return Rules).

This is a greatest relief to the small tax payers and reduces their compliance related complexities and cost.

Comparative Cost Advantage:

Let us now discuss comparative cost advantages of both the schemes. For simplicity of comparison let us take two scenarios as below but operating under similar assumptions of receipts, tax rates and value addition.

- Supplier is Registered under Composition Scheme and supplying to registered business (B2B) and to the consumer (B2C).

- Supplier is Registered under Normal Scheme and supplying to registered business (B2B) and to the consumer (B2C).

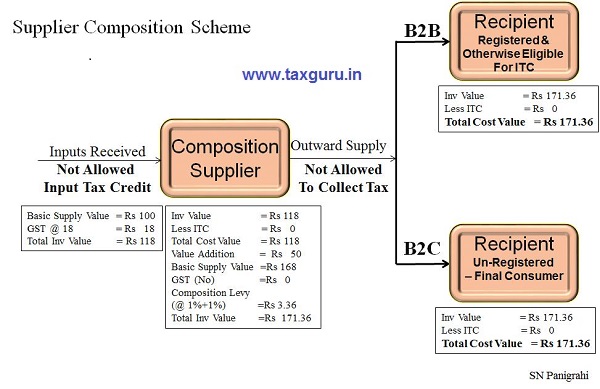

The calculations are shown below separately. From the calculations it is very clear that composition scheme is beneficial when supplying to final consumer (B2C) (Cost Value is Rs 171.36 compared to Rs 177 in case of Normal registered supplier). Where as in case of supplying to another business (B2B) it is not advantageous (Cost Value is Rs 171.36 verses Rs 150).

Finally we may conclude that

- For B2B transactions, Composition Scheme is not Advisable

- However in case of B2C, it is advantageous

Limitations of Composition Scheme

Under Composition Scheme, GST should not be collected on outward supply and supplied against Bill of Supply instead of Tax Invoice. Since the outward supply is not taxed, input tax credit is not allowed. That is Composition dealers are not allowed to collect tax from the recipient of supplies, and are not allowed to take Input Tax Credit.

However there is no restrictions on inward supplies. The person registered under the scheme is allowed to get inputs from intra-state or inter-state or import source.

The other restrictions are

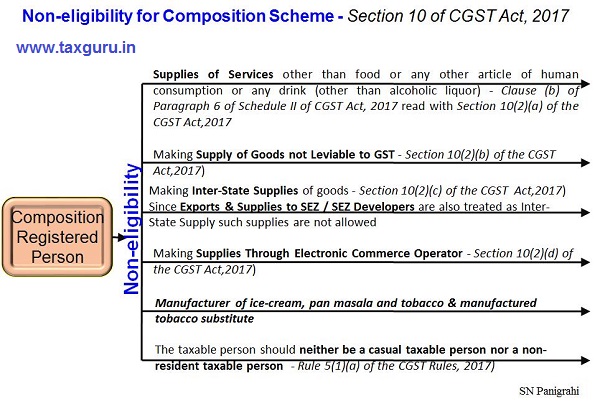

Any taxable person is not eligible for composition levy if he is,-

- Engaged in supplies of services other than supply of goods, being food or any other article of human consumption or any drink (other than alcoholic liquor) { Ref: Clause (b) of Paragraph 6 of Schedule II of CGST Act, 2017 read with Section 10(2)(a) of the CGST Act,2017);

- Making supply of goods not leviable to GST(Ref: Section 10(2)(b) of the CGST Act,2017);

- Making inter-state supplies of goods(Ref: Section 10(2)(c) of the CGST Act,2017);

- Making supplies through electronic commerce operator (Ref: Section 10(2)(d) of the CGST Act,2017).

- Being manufacturer of any notified goods (as may be notified by Government by issuing notification) (Ref: Section 10(2)(e) of the CGST Act,2017)

- Vide notification No. 8/2017-Central Tax, dated 27.6.2017, the Central Government has notified manufacturer of ice-cream, pan masala and tobacco & manufactured tobacco substitute from availing composition levy scheme].

- The taxable person should neither be a casual taxable person nor a non-resident taxable person; (Ref: Rule 5(1)(a) of the CGST Rules, 2017)

- Composition scheme is levied for all business verticals with the same PAN. A taxable person will not have the option to select composition scheme for one, opt to pay taxes for other.

Despite having advantage in case of B2C type of transactions, the scheme is not gaining popularity because of some of restrictive provisions.

At a Glance Comparison of Normal & Composition Scheme

Below presented at a glass comparison of both the schemes.

SN Panigrahi, GST Consultant, Author & Trainer can be reached @ snpanigrahi1963@gmail.com

Author Bio

normal sceme me man lo 5% jo gst pay kra fir wo mal unregistered ko sale kra tab kya muje itc ka benefits milega or government ko dubara 5% pay karna padega plz w 8595447312)

any body can understand clear picture of composition scheme, thank you sir

While opting for composition scheme you will have to reverse all input credit taken on available stock. If it is then what will be the rate of reversal. If a person is having large stock and opt for composition is not it make hardship to him. Will have to pay a large amount in lumpsum

Government of the day wants to bring everyone under tax net . Rs.2000000/- threshold limit and composition scheme like measures under GST are only an eyewash .The real intelligence behind GST is not to leave anyone without tax payment !!!

Very nice explanation. But one thing, A composition dealer will not take credit of GST paid on Reverse Charge method also. Every GST paid by him will lost in ITC claim and he has to pay 1% or 2% as the case may be from his revenue only. So selection of Composition scheme we have to take care of the Dealer’s operation of Business.

very good article thank you sir

Very clear explanation. Thanks sir

big thank you and keep it up sir

Thank you very much for clarification by comparison. Very helpful for non-accounts people.

Now I am very clear that I shouldn’t go for composition because

(a) I can’t provide services

(b) I can’t make interstate sales

Thanks again.

Author has explained the situation in both the cases very well & in a lucid manner. It is helpful for all Tax Professionals. Views expressed by the author in the article highly appreciated Sir. Thanks regards

Try to understand the system , only saying good , informative will not serve to complied with GST

( composite scheme )

very informative…..thanks a lot

Very Good analysis & comparison.

Very useful article.

If the Normal purchased from Composition.How the GST effect.

Very good article thank you

Good and elaborated article. Earlier also you wrote good articles. Congratulations Sir.,