An introduction:- An E-way bill previously in VAT regime well known as road permit, E-sancharan, way bill, E-sugam, ST Form-10, Form-61 &62, Form-DIX, Form-402 & 403, Form-38, Form-26, JVAT-504G, Form-16, Form-49, Form-35, Form-40, Form-33, Form-32, F0rm-25 & Form-50 etc. different states, different names. In some state it was being issued by manually or some states was online generation processor. But now it has been old. I can say old days has been gone now. Now all processor will be online /digitalize. There is no processor for issue a manual e-way bill. The Govt. is going to be implement a very hassle free system to reduce time wasting and will save cost of a large industry back bone.

Now there is only one name, one way bill i.e. E-way bill. One Great Nation, One GST or One E-way bill.

As we all know that E-way has been introduced since 16th Jan-18 on temporary basis. Now from tomorrow 1st Feb-2018 it is going to be implement Nationwide. States list are increasing very fastly. Most of states are going to be implement both Intra-State and Inter-state basis e-way bill. Where more than 13 states has been confirmed for the same.

There are few states which are also going to implement Intra-State basis e-way bill from 1st of May-18 or 1st June-18.

Important E-way bill relates forms:-

FORM GST EWB-01:- E-Way Bill FORM GST, EWB-02:- Consolidated E-Way Bill FORM GST, EWB-03:- Verification Report FORM GST, EWB-04:- Report of detention Form, GST ENR-01:- Application for Enrolment under section 35 (2), [only for un-registered persons], FORM GST INV – 1:- Generation of Invoice Reference Number.

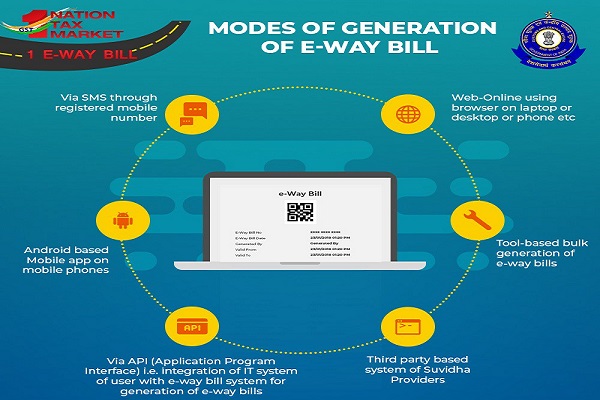

Important six modes of generation of E-way bill:-

1. Web-online browser on laptop or desktop or phone etc.

2. Via SMS through registered mobile No.

3. Android based mobile app on mobile pones

4. Via API(Application Programme Inteface) i.e.integration of IT System of user with e-way bill system for generation of e-way bills

5. Third party based system of Suvidha Providers

6. Tool based bulk generation of e-way bills.

A list of E-way bill benefits:-

1. Easy and quick generation of e-way bill.

2. No waiting time at check post and faster movement of goods thereby optimum use of vehicle/resources as there are no check post in GST regime

3.Taxpayers/Transporters there is no need to visit any tax officers/checkpost for generation of e-way bill/movement of goods across states

4. User friendly portal and SMS bases bill generation systems

5. Check and Balance for smooth tax administration and process simplification for easier verification of e-way bill by tax officers.

Condition for generation e-way bill:-

1. The value of inter-state supply is more than Rs. 50,000/-

2. Consignor or Consignee any one can generate the e-way bill

3. If Consignor or Consignee both don’t generate the e-way bill and value of goods more than Rs. 50,000/- then responsibility of the generating e-way bill will be of the transporter.

4. It can not be generate manually. It can be generate computerized only.s

5. The system mandates generation of E-Way Bill by a registered person when he effects a transportation of good worth above fifty thousand beyond 10 km. the EWB has to be generated before the transportation starts. The EWB is valid for one day for transportation up to 100 km. for 200 km, the validity is two days.

6. To generate an e-way bill, the supplier and transporter will have to upload details on the GSTN portal, after which a unique e-way bill number (EBN) will be made available to the supplier, the recipient and the transporter on the common portal.

7. An E-way bill contains two parts- Part A to be furnished by the person who is causing movement of goods of consignment value exceeding Rs.50,000/- and part B (transport details) to be furnished by the person who is transporting the goods.

8. Where the goods are transported by a registered person whether as consignor or recipient, the said person shall have to generate the e-way bill by furnishing information in part B on the GST common portal.

9. Where the e-way bill is not generated by registered person and the goods are handed over to the transporter for transportation by road, the registered person shall furnish the information relating to the transporter in Part B of FORM GST EWB-01 on the common portal and the e-way bill shall be generated by the transporter on the said portal on the basis of the information furnished by the registered person in Part A of FORM GST EWB-01

10. The validity of e-way bill depends on the distance to be traveled by the goods. For a distance of less than 100 Km, the e-way bill will be valid for a day from the relevant date.

11. For every 100 Km thereafter, the validity will be added one day from the relevant date. The “relevant date” shall mean the date on which the e-way bill has been generated and the period of validity shall be counted from the time at which the e-way bill has been generated and each day shall be counted as twenty-four hours

12. In general, the validity of the e-way bill cannot be extended. However, Commissioner may extend the validity period only by way of issue of notification for certain categories of goods which shall be specified later.

13. In exceptional circumstances, if the goods cannot be transported within the validity period of the e-way bill, the transporter may generate another e-way bill after updating the details in Part B of FORM GST EWB-01.

14. If the goods are either not transported or are not transported as per the details furnished in the e-way bill, the e-way bill may be canceled electronically on the common portal, either directly or through a Facilitation Centre notified by the Commissioner, within 24 hours of generation of the e-waybill.

15. E-way bill cannot be canceled if it has been verified in transit in accordance with the provisions of rule 138B of the CGST Rules, 2017.

Important information is to be given at E-way bill portal:

There are two parts of E-way bill generation-

Part-A:

GSTIN of recipient, place of delivery (PIN Code), invoice or challan number and date, value of goods, HSN code, transport document number (Goods receipt number or railway receipt number or Airway bill Number or Bill of Lading Number) and reasons for transportation;

Part-B:

Transporter details (Vehicle details)

Exemption

1. Goods with value less than Rs. 50,000/- not required to generate way-bill

2. Transport by non-motorised conveyances

3. Goods transported from international ports , etc, to hinterland ports for clearance by customs

4. Intra-state movement within a specific area as decided mutually by Centre-state

Why E-Way Bill is important in the overall GST Scheme ?

GST Being a self regulated law with integrated credit and #OneNationOneMarket benefit , it is expected for dealers to register and comply with timely recovery of GST and payment to the Government. Movement between state and within state in B2B transactions was earlier governed by various forms ( entry , declaration, transit and lower / nil tax rates) , which have been scrapped now. With the Unified system of E-way roll-out , it will be very important to improve the compliance level with more precision by using technology. Therefore to avoid mistake and hassle free e-way downloading & filling up in new GST regime , it has been demanded by States to open Suvidha Kendra and awareness campaigns.

It is true that when non-finance and non-tax people will prepare e-way bills using common ids , it may have errors which will prove fatal during random audit / detention of vehicle. To make the process smarter , either organization have to create robust communication and training framework or they can simply outsource the process to trained staff / service providers.

How to use GST Street to support in your e-way bill compliances ?

We will consult and design your compliance support center for whole India needs , use of GSTStreet unified proprietary Software , flexible pricing for services ( not product) and work flow management for E-way bill will be managed by our teams and our focus is to service large stakeholders like logistics companies, warehousing , e-commerce operators or consumer goods companies where volume and speed is the key. Our 400+ expert team will be available to support on dispute resolutions in 50+ cities if need arise. Our Objective is to ensure your e-way bills are generated flawlessly with dedicated & trained account management staff and you do not get compromised in your compliance because of the cost with efficiency involved.

Pricing Strategy :

High Volume Client – Monthly Retainer – One Staff for 2000 E-way bills

Mid Volume Client ( between 100 to 2000 EWB per month) – INR 50k pm

Low Volume Client ( less than 100 EWB per month) – INR 200 per EWB

Software Charges – Nil

Licensing Fees – Nil

Dispute Resolution / Representation – OPE on Actuals

Consultation : Blended rate of INR 2000 per hour