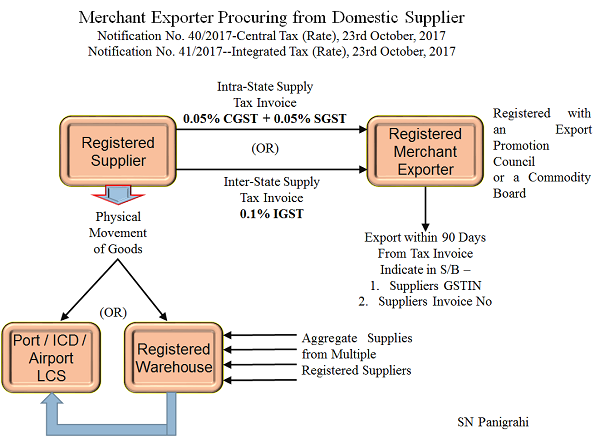

Procedures for Procuring Goods from Domestic Supplier by Merchant Exporter is prescribed in the following notifications

Notification No. 40/2017-Central Tax (Rate), 23rd October, 2017

Notification No. 41/2017–Integrated Tax (Rate), 23rd October, 2017

Notification No. 40/2017-Union Territory Tax (Rate), 23rd October, 2017

Similar Notification also in respect of SGST

The Procedures for Procuring from Domestic Suppliers by Merchant Exporter is :

1. Both the Supplier and Merchant Exporter must be Registered Persons

2. The registered supplier shall supply the goods to the registered recipient on a tax invoice Charging GST :

a. Intra-State – 0.05% of CGST + 0.05% of SGST

b. Inter- State – 0.1% of IGST

3. The registered recipient shall export the said goods within a period of ninety days from the date of issue of a tax invoice by the registered supplier;

4. The registered recipient shall indicate the Goods and Services Tax Identification Number of the registered supplier and the tax invoice number issued by the registered supplier in respect of the said goods in the shipping bill or bill of export, as the case may be;

5. The registered recipient shall be registered with an Export Promotion Council or a Commodity Board recognised by the Department of Commerce;

6. The registered recipient shall place an order on registered supplier for procuring goods at concessional rate and a copy of the same shall also be provided to the jurisdictional tax officer of the registered supplier;

7. The registered recipient shall move the said goods from place of registered supplier –

(a) directly to the Port, Inland Container Deport, Airport or Land Customs Station from where the said goods are to be exported; or

(b) directly to a registered warehouse from where the said goods shall be move to the Port, Inland Container Deport, Airport or Land Customs Station from where the said goods are to be exported;

8. When goods have been exported, the registered recipient shall provide copy of shipping bill or bill of export containing details of Goods and Services Tax Identification Number (GSTIN) and tax invoice of the registered supplier along with proof of export general manifest or export report having been filed to the registered supplier as well as jurisdictional tax officer of such supplier.

9. The registered supplier shall not be eligible for the above mentioned exemption if the registered recipient fails to export the said goods within a period of ninety days from the date of issue of tax invoice.

10. if the registered recipient intends to aggregate supplies from multiple registered suppliers and then export, the goods from each registered supplier shall move to a registered warehouse and after aggregation, the registered recipient shall move goods to the Port, Inland Container Deport, Airport or Land Customs Station from where they shall be exported;

11. In case of situation referred to in condition (vii), the registered recipient shall endorse receipt of goods on the tax invoice and also obtain acknowledgement of receipt of goods in the registered warehouse from the warehouse operator and the endorsed tax invoice and the acknowledgment of the warehouse operator shall be provided to the registered supplier as well as to the jurisdictional tax officer of such supplier; and

Comments :

Nominal Payment (0.1%) of GST and procedure of manual submission of Purchase Order, Copy of Shipping Bill, Copy of Invoice, Warehouse Acknowledgment, Copy of EGM etc is prescribed so as to track the Transactions, Monitor and control and ensuring actual exports are made.

In this regard following observations are made :

1. Merchant Exporter must procure the goods only from Registered Person

2. Manual Documentation resembling Previous Excise Regime are introduced in a major deviation from Heart of GST ie Digitalization.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author

Can be reached @ snpanigrahi1963@gmail.com

Author Bio

What if the registered supplier does not have an godown

And if he wants to aggregate goods and export?

Sir, Why FIEO Chairman, Export Promotion Council Chairmen raise objection against the notifications as copy of Custom’s Shipping Bill supply to supplier is exposure of Business Privacy of the Merchant Exporter. It is requested only Proof Export viz. AWB/BL would be provided which contains details of export cargo. Regards.

Dear Sir,

In This notification ” Registered suppliers” includes Manufacturer as well as Retailer ?

For Example A is manufacturer and B is Trader and C is Merchant Exporter

C can Buy the Goods from B under this notification 41/2017 and that goods are manufactured by A????

Dear Sir,

We are Merchant Exporter and have Membership with FIEO.

We have exported under payment of 18% GST with Bond / Bank Guarantee in Sept. 2017.

At present with new Rule under payment of 0.10% GST whether Bond Bank Guarantee or LUT is required

Is the registered recipient (trader from india)shall move the said goods from place of registered

supplier(manufacturer from india) to the retailer,( buyer from india)

Is the registered recipient (trader)shall move the said goods from place of registered

supplier(manufacturer) to the retailer,( buyer)

What is the meaning of registered warehouse.

Dear Sir,

We manufacture and supply goods to Merchant Exporter. As per the notification, Merchant exporter is liable to pay 0.1%of GST to us. So now what is the procedure of claiming ITC for domestic suppliers?

Dear Sir

I am a small exporter of auto parts,I get order from overeas buyer only when they need goods in small quantities

kindly guide me how to go about if a local dealer in Delhi or Chennai supplies goods to me