This article has been written with an objective to consolidate all the relevant legal provisions relating to job work for educational purposes

“Job Work” has been defined Section 2(68) of the CGST Act, 2017 as follows:

“job work” means any treatment or process undertaken by a person on goods belonging to another registered person and the expression “job worker” shall be construed accordingly;

There are two important parts of the above definition:

| Any treatment or process | Goods belonging to another registered person |

|

|

Question now arises what about such activities where the treatment or process is being performed on goods belonging to un-registered person. We will come to this question in later part of our discussion.

Since, we are now clear with the definition of Job work, let us move to another question:

Whether Job work would amount to supply of goods or service?

Section 7(1A) of the CGST Act, 2017 read with Schedule II deems certain supplies to be treated as either supply of goods or services.

Entry No. 3 of the Schedule II provides that “any treatment or process which is applied to another person’s goods is a supply of services”

The said entry does not restrict itself only to such treatment or process which qualifies as ‘Job work’ under GST. It covers all transactions i.e. either Job work as per the above-mentioned definition or otherwise. Therefore, as discussed above, the activity of treatment or process not qualifying as ‘job work’ as the principal is un-registered, should amount to supply of service.

From the above-said entry, it is clear that Job work would amount to supply of service.

Specific Job work Provisions under GST laws

Section 143 – Job work Procedure

Section 19 – Taking Input tax credit in respect of inputs and capital goods sent for job work

Rule 45 of the CGST Rules – Conditions and restrictions of inputs and capital goods sent for Job work

Let us understand the above provisions by taking the following example:

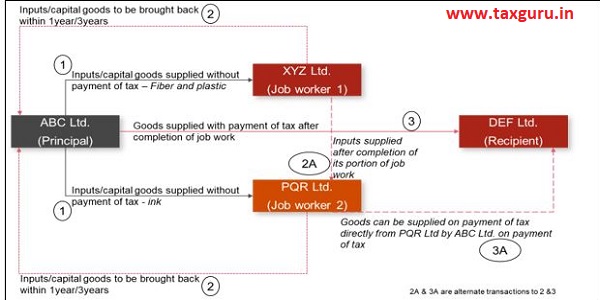

ABC Ltd. is in the business of manufacturing and supply of pens. For manufacturing such pen, the following are the major components are required – Fiber and plastic (for body of the pen) and ink for refills. ABC limited procures these raw materials and send further to the following entities:

XYZ Limited – Fiber and plastic for preparing the body of pen

PQR Pvt. Ltd. – ink for making refills

ABC Limited has also sent a machinery to XYZ limited for preparing body of the pen. Further, it has sent moulds to PQR Pvt. Ltd. to prepare the nib of the pen along with refill as per industry standards

Section 143 lays down the procedure for sending the inputs and capital goods to a job worker. As per the said provision, a registered person (‘Principal’) may send inputs or capital goods to a job worker without payment of tax subject to condition that such inputs or capital goods would be brought back within prescribed time period.

For purpose of this section inputs would also include the intermediate goods arising out of the job work process.

It further provides that inputs and capital goods may also be sent by the principal to a job worker and subsequently be sent to another job worker (i.e. ABC Ltd. may send the body of pen from the premise of XYZ Ltd. to PQR Pvt. Ltd.(for putting refills into such body) as well without payment of tax.

Section 143 also provides an option to principal to supply the final goods directly from job worker premises on payment of tax subject to condition that where the job worker is un-registered, the job worker’s premise has to be shown as additional place of business in the GST registration of the principal.

However, the supply of goods by principal to job worker without payment of tax is subject to certain condition prescribed under the said Section. Section 143 provides that

- Inputs and capital goods sent without payment of tax to job worker should be brought back after completion of job work or otherwise within one year and three years of being sent out, or

- Supply of inputs or capital goods from the premise of job worker on payment of tax or without payment of tax in case of export within one year and three years of being sent out,

Further, a second proviso has been inserted under Section 143 vide The Central Goods and Services Tax (Amendment) Act, 2018 (w.e.f 01 Feb 2018) which states that the time limit of one year or three years may be extended by the Commissioner for a further period of one year or two years respectively.

To summarize till here:

Moulds and dies, jigs and fixtures, or tools sent to job worker

The one important point to be noted here that the aforesaid restriction of timelines does not apply to moulds and dies, jigs and fixtures, or tools sent to job worker.

Therefore, such moulds and dies etc. may be sent to job worker without any restriction of bringing it back within prescribed timelines. There may be a case that such goods are permanently transferred by the principal to job worker.

Issue – As per entry 1 of the Schedule I of the CGST Act, 2017, permanent transfer of business assets without consideration should be deemed to be ‘supply’ and therefore subject to tax. Whether transfer of moulds and dies, jigs and fixtures or tools to job worker for indefinite period would subject to tax?

What will happen if inputs/ capital goods not brought back within prescribed timelines?

Where the inputs/ capital goods are not brought back within above mentioned timelines or not supplied with payment of tax from the business place of the job worker, it shall be deemed that such inputs or capital goods were supplied by the principal to the job worker on the day when the same were sent out

Accordingly, the principal would be liable to pay GST on the same along with applicable interest on such transfer of inputs or capital goods to the job worker

Issue –

If the inputs or capital goods are not brought back within prescribed timelines, the same would amount to deemed supply in the hands of principal However, such supply would not have any consideration as the same were supplied were FOC by the Principal to the job worker.

1. As per Section 7of the CGST Act, 2017, only supplies covered under Schedule I would be deemed to be supply without consideration. The above said transaction is not covered under Schedule I. In such case, can it be said to a ‘supply’ within ambit of Section 7 of the CGST Act, 2017?

2. What would be the valuation of such supply as per Section 15 of the CGST Act, 2017? As the provisions of Section 15, the valuation mechanism referred in CGST Rules can be adopted only when either supplier or recipient is related, or the price is not the sole consideration. The principal and job worker are unrelated parties and the goods had been supplied free of cost.

3. In case, the aforesaid transaction amount to supply, how would the provisions of the second proviso to Section 16(2) would be enforced (i.e. payment to the supplier within 180 days of the date of invoice) in case, job worker avails credit of tax charged by the principal, would it be liable to reverse the same within 180 days as there would be no consideration to be paid to the principal. Further, CGST rules deem the consideration to be paid only in two cases, supplies covered under Schedule I and value of supply on account of Section 15(2)(b) of the CGST Act, 2017

In Part 2 we will discuss the taxability of Section 19, Rule 45, procedures for movement of goods in case of job work and also the various rates applicable in case of job work.

Author Bio

Dear Nikhilji,

Greetings for the Day!!!

In the scenario that you have iterated here, would like to have some sort of further discussion regards to

1) Capital Goods Sent for Job Work

Here, can we say that for Capital Goods, definition of Job Work and Job Worker would not be attracted as person is not doing any treatment or process ON capital goods.

If so, do we need to further think on procedure to get back the CG withing 3 years or reversal of ITC in this regard.

In case of capital intensive industries, how can it be possible to get back and again provide machineries to its Job Workers???

Would like to have your opinion and guidance in this regard.

Thanking You in advance,

Regards,