Summary: The eligibility of Input Tax Credit (ITC) on construction of immovable property under Sections 17(5)(c) and 17(5)(d) of the CGST Act, 2017 is a contentious issue. ITC is disallowed for goods or services used for constructing immovable property, except for plant and machinery (P&M). The absence of a clear definition of “immovable property” and varied interpretations of “P&M” have led to significant disputes. While ITC is unambiguously ineligible for factory buildings or interior works and eligible for P&M used directly for production, challenges arise in borderline cases like lifts, transformers, or HVAC systems. Judicial precedents under older laws, such as the Central Excise Act, have guided classifications based on tests like object and nature of annexation, permanence, and marketability. However, these classifications often leave room for interpretation. The Delhi High Court’s decision in Bharti Airtel Ltd. v. Commissioner provided clarity by treating telecommunication towers as movable property, allowing ITC. As GST law continues to evolve, reliance on earlier legal frameworks, case law, and the definition of P&M remains crucial for determining ITC eligibility.

(SECTION 17(5)(c) & 17(5)(d) OF THE CGST ACT, 2017)

1. WHAT IS COVERED IN THIS ARTICLE?

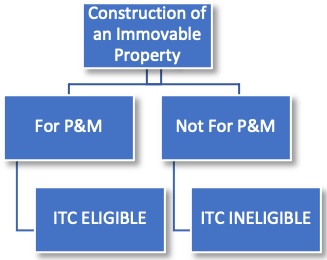

Input Tax Credit (ITC) on inward supplies for construction of an immovable property is blocked U/s 17(5)(c) and 17(5)(d) of the Central Goods and Services Tax Act, 2017 (‘Act’) to the extent of capitalisation. However, ITC is available if it is a construction of Plant & Machinery (‘P&M’), even if immovable. The absence of definition of the term ‘immovable property’ under the Act coupled with varying interpretations of this term and ‘P&M’ by AARs & AAARs remain a significant concern for claim of ITC. In the coming years, the terms ‘construction of an immovable property’ and ‘P&M’ are likely to be subjects of judicial debate in this context. Below, I outline the reasons for raising this concern.

2. WHERE LIES THE POSSIBLE DISPUTE?

The key challenge lies in identifying ‘immovable property’ and ‘P&M’ for the purpose of Section 17(5)(c) and 17(5)(d). For the sake of convenience, the said inward supplies are categorised into three broad categories:

Category-1: ITC on inward supplies for construction of a factory building, false ceiling and other interior works forming part of the building, landscaping etc. – ITC is NOT eligible and this is not in doubt.

Category-2: ITC on inward supplies for construction of Plant & Machinery, although immovable, which are used directly for manufacture of taxable goods/provision of taxable services – ITC is eligible and this is also not in doubt.

Category-3: ITC eligibility on inward supplies other than mentioned in Category-1&2 (Example: Lifts, transformer, electrical panel boards/fittings, solar plant, effluent treatment plant, HVAC etc.) is where the challenge lies. Are such supplies movable or immovable property? Are such supplies in the nature of ‘P&M’? This Article revolves around these two questions.

3. ITC ELIGIBILITY REVOLVES AROUND TWO TERMS – ‘IMMOVABLE PROPERTY’ & ‘PLANT AND MACHINERY’

As per Section 17(5)(c) and 17(5)(d), ITC shall NOT be available on:

(c) works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service;

(d) goods or services or both received by a taxable person for construction of an immovable property (other than plant and* machinery) on his own account including when such goods or services or both are used in the course or furtherance of business.

* The Finance Bill, 2025 has substituted “plant or machinery” with “plant and machinery”, retrospectively, w.e.f. 01.07.2017, to nullify effect of Safari Retreats case [2024] 90 GSTL 3 (SC).

For the purpose of this article, the provisions of Section 17(5)(c) & 17(5)(d) can be summarised as under:

4. HOW TO IDENTIFY IF IT IS A CONSTRUCTION OF AN ‘IMMOVABLE PROPERTY’?

As mentioned above, ITC on ‘construction of an immovable property’ is eligible only if it is a P&M. Hence, it is pertinent to ascertain if a construction has resulted in an ‘immovable property’. The term ‘immovable property’ is not defined under the GST law. With no major decisions from the Courts on the subject matter under the GST law, help ought to be sought from the General clauses Act, 1897, Transfer of Property Act, 1882 and judicial precedents.

4.1 Movable and immovable property as per General Clauses Act & Transfer of Property Act

As per Section 3(26) of the General Clauses Act, 1897: “immovable property” shall include land, benefits to arise out of land, and things attached to the earth, or permanently fastened to anything attached to the earth. Section 3(36) of the said Act defines movable property as “property of every description, except immovable property”.

As per Section 3 of the Transfer of Property Act, 1882 immovable property does not include standing timber, growing crops or grass. It further says that “attached to the earth” means:

(a) rooted in the earth, as in the case of trees and shrubs;

(b) imbedded in the earth, as in the case of walls or buildings; or

(c) attached to what is so imbedded for the permanent beneficial enjoyment of that to which it is attached.

4.2 Decisions under the Central Excise & VAT laws

It was this term (‘immovable property’) which ran a full round of litigation under the erstwhile Central Excise Act, 1944. Unfortunately, the lawmakers have ‘inherited’ this Central Excise issue to the GST tenure by not defining the term ‘immovable property’. In the context of the erstwhile Central Excise and VAT law, Courts decided on what tantamount to ‘movable’ or ‘immovable’ property. The following are the gist of various decisions of the Courts :

| S. No | Parties | Citation |

| 1 | Sirpur Paper Mills Ltd vs CCE | 1998 (97) ELT 3 (SC) |

| 2 | Triveni Engineering & Industries Ltd vs CCE | 2000 (120) ELT 273 (SC) |

| 3 | CCE vs. Josts Engineering Co Ltd. | 2002 (146) ELT 29 (SC) |

| 4 | Mallur Siddeswara Spinning Mills (P) Ltd v CCE | 2004 (166) ELT 154 (SC) |

| 5 | CCE vs. Solid & Correct Engineering Works | 2010 (252) ELT 481 (SC) |

| 6 | CTO v. Sadulshahar Krai Vikrai Sahakari | (2004) 135 STC 90 (Raj) |

| 7 | Jaiprakash Industries Ltd vs CCT | (2010) 36 VST 152 (UTK HC) |

- Nature of annexation: This test ascertains how firmly a property is attached to the earth. If the property is so attached that it cannot be removed or relocated without causing damage to it, it is an indication that it is immovable.

- Object of annexation: If the attachment is for the permanent beneficial enjoyment of the land, the property is to be classified as immovable. Conversely, if the attachment is merely to facilitate the use of the item itself, it is to be treated as movable, even if the attachment is to an immovable property.

- Intendment of the parties: The intention behind the attachment, whether express or implied, can be determinative of the nature of the property. If the parties intend that the property in issue is for permanent addition to the immovable property, it will be treated as immovable. If the attachment is not meant to be permanent, it indicates that it is movable.

- Functionality Test: If the article is fixed to the ground to enhance the operational efficacy of the article and for making it stable and wobble free, it is an indication that such fixation is for the benefit of the article, such the property is movable.

- Permanency Test: If the property can be dismantled and relocated without any damage, the attachment cannot be said to be permanent but temporary and it can be considered to be movable.

- Marketability Test: If the property, even if attached to the earth or to an immovable property, can be removed and sold in the market, it can be said to be movable.

The CBEC vide Order No.58/1/2002-CX dated 15.01.2002, issued under Section 37B of the CE Act also clarified regarding excisability of plant & machinery erected and installed at site which are in line with the above decisions. However, under GST law, ITC would be eligible even if the Plant & Machinery is immovable after installation/erection.

4.3 Breather from Delhi High Court in the context of Section 17(5)(d)

In a landmark decision the Delhi High Court in Bharti Airtel Ltd. v. Commissioner [2024] 169 taxmann.com 390 (Delhi) held that Telecommunication tower is NOT an immovable property for the purpose of Section 17(5)(d) of the Act. The High Court, following the decision of the Apex Court in Bharti Airtel Ltd. v. CCE 2024 SCC OnLine SC 3374, held that ‘telecommunication towers are liable to be treated as movable’ and that ‘telecommunication towers would not fall within the ambit of Section 17(5)(d) of the CGST Act’.

Therefore, one has to consider the provisions of the General Clauses Act, 1897, the Transfer of Property Act, 1882 and the rationale laid down by the Courts to decide if a property is ‘movable’ or ‘immovable’ for the purpose of Section 17(5)(c) and 17(5)(d).

5. HOW TO IDENTIFY IF CONSTRUCTION OF AN IMMOVABLE PROPERTY IS ‘PLANT AND MACHINERY’?

5.1 Definition of Plant & Machinery

If an inward supply is for ‘construction of an immovable property’, which is a ‘P&M’, then ITC can be availed. Hence, it is paramount to identify what ‘P&M’ is for the purposes of Section 17(5)(c) & 17(5)(d). The term ‘P&M’ is defined in Explanation to Section 17 as follows:

“Explanation.— For the purposes of this Chapter and Chapter VI, the expression “plant and machinery” means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services or both and includes such foundation and structural supports but excludes—

(i) land, building or any other civil structures;

(ii) telecommunication towers; and

(iii) pipelines laid outside the factory premises”.

It can be inferred from the definition that (a) apparatus, (b) equipment, and (c) machinery fixed to earth by foundation or (d) structural support that are used for making outward supplies are P&M for the purpose of Section 17(5)(c) and 17(5)(d).

5.2 Dictionary meaning of apparatus, equipment, machinery

Apparatus means: ‘A set of equipment or tools or a machine that is used for a particular purpose’ – Cambridge dictionary;

Equipment means: ‘The set of articles or physical resources serving to equip a person or thing: such as (1) the implements used in an operation or activity, (2) all the fixed assets other than land and buildings of a business enterprise, (3) the rolling stock of a railway’ – Merriam-Webster dictionary;

Machinery means: ‘A group of large machines or the parts of a machine that make it work’ – Cambridge dictionary;

It my view the terms ‘apparatus’, ‘equipment’ and ‘machinery’ are broad enough to cover most of the fixed assets used in a business i.e. HVAC, Transformers, electrical panel boards, firefighting system etc. for the purpose of Section 17(5)(c) and 17(5)(d). The undeniable facts are that (a) such goods are used in making outward supplies (b) the said inward supplies are not specifically blocked by Section 17(5)(c) and 17(5)(d) and (c) such inward supplies do NOT fall within the exclusion list of ‘P&M’ i.e. land, building, or any other civil structures, telecommunication towers and pipelines laid outside the factory premises. Hence, such inward supplies are P&M eligible for ITC even if considered as immovable.

5.3 Breather from CBIC on P&M

The CBIC clarified in Circular No.219/13/2024-GST [F.NO.CBIC-20001/4/ 2024-GST], dt.26-06-2024 that ‘PVC ducts’ and ‘manholes’ are covered “plant and machinery” as they are used as part of optical fiber cables (OFC) network for making outward supply of transmission of telecommunication signals from one point to another. The Circular further clarified that the ‘ducts’ and ‘manholes’ have not been specifically excluded from the definition of “plant and machinery” in the Explanation to Section 17 of the Act. This Circular is an important step forward to identify P&M for the purpose of Section 17(5)(c) and 17(5)(d).

6. DECISIONS FROM THE AAR/AAAR ON ‘IMMOVABLE PROPERTY’ AND ‘PLANT AND MACHINERY’

Let us take a look at the decisions by the AARs & AAARs which were rendered in the context of Section 17(5)(c) and 17(5)(d). All the decisions revolve around whether the inward supplies result in ‘construction of an immovable property’ and/or whether it tantamount to P&M. Many of the decisions of the AAR/AAAR, in my view, cannot be considered as final for multiple reasons (the reasons are given in the Notes alongside with gist of the AAR/ AAAR’s decisions below):

| S.

No. |

Inward supply | Whether ITC Admissible or not, as per the AAR/AAAR | Author’s Notes |

| A. | Pre-fabricated structures for construction of buildings, sheds etc. | ITC inadmissible on pre-fabricated shed, Paver Blocks and Rotary parking system since it is an immovable property – Sanghi Enterprises[1], Sundharams (P.) Ltd.[2] & Arthanarisamy Senthil Maharaj[3]. | ITC inadmissible. Although, it can be argued that pre-fabricated structures can be dismantled and shifted (i.e. ‘movable’), considering the definition of ‘immovable property’ under the General Clauses Act, 1897 & Transfer of Property Act, 1882 and the law laid down by the Apex Court, the same can only be considered as ‘immovable’ – Refer para 4.1 & 4.2 above. |

| B. | Fees paid to architects, consulting engineers | ITC inadmissible on GST paid on Architect Service Fees and Interior Designing Fees as per Section 17(5)(d) –Varachha Co-op. Bank Ltd.[4] | ITC inadmissible. The services of architects, consulting engineers etc. in my view, form part of ‘construction of an immovable property’ and hence blocked U/s 17(5)(d). |

| C. | Civil works and structural support for overhead crane/P&M | ITC Admissible. ITC Admissible on overhead rails and gantry beams laid exclusively for the purpose of movement of overhead crane. Proportionate ITC is admissible on structural support for the crane by applying the given ratio – Coral Manufacturing Works India (P.) Ltd.[5] | ITC Admissible. The definition of ‘Plant and Machinery’ in Section 17(5) includes foundation and structural supports. Since Overhead Crane is a P&M, eligible for ITC, the structural support for the Crane is also eligible.

The AAR in Atriwal Amusement Park[6] held that steel and civil structures supporting the PVC Water Slides (P&M) is eligible for ITC. |

| D. | Detachable sliding and stackable glass partitions | ITC Admissible. Detachable sliding and stackable glass partitions eligible for ITC and will not be hit by Section 17(5)(d) – Wework India Management (P.) Ltd.[7] | ITC Admissible. Such goods are capable of being shifted without any major damage. The very purpose of such goods are to ensure portability for one reason or another. These days there are many goods such as Detachable cubicles, raised flooring etc. designed for portability. |

| E. | Lifts/ Elevators | ITC inadmissible. Erection, installation and commissioning of lift is an immovable property and is not P&M – Varachha (supra).

Once lift was installed and commissioned in building it became integral part of immovable property i.e. building – Las Palmas Co-op. Housing Society[8] |

ITC Admissible. The Gujarat High Court, in CIT v. Jyoti Ltd.[9], in the context of Development rebate under the Income Tax Act, 1961 held that Lifts are ‘machineries’.

Concise Oxford Dictionary: ‘lift’ means an apparatus for raising and lowering persons or things to other floors of building; Cambridge dictionary: elevator is a piece of equipment, usually in the form of a small room, that carries people or goods straight up and down in tall buildings. Merriam-Webster dictionary: elevator is a machine used for carrying people and things to different levels in a building. Hence, it can be well argued that ‘Lift’ is covered under P&M. Further, one could argue that Lifts are ‘movable’ since they are capable of being shifted from one place to another without causing much damage. |

| F. | Effluent/ Water/ Sewage treatment plant | ITC inadmissible. Effluent /Sewage/Water Treatment Plants are civil structures/ not covered under the definition of P&M – Colour band Dyestuff P Ltd.[10], Synergy Global Steel (P.) Ltd.[11] and Tarun Realtors (P.) Ltd.[12].

ITC partly Admissible on external sewage system – Nipro India Corpn. (P.) Ltd.[13] |

ITC Admissible partially. Effluent and sewage treatment plants involve civil, piping and mechanical work. While it can be said that the civil tanks and structures are ineligible, ITC ought to be extended to inward supplies on mechanical and piping works that are both movable and are P&M. |

| G. | Fire Protection Work, Fire safety extinguishers | ITC inadmissible. It does not fall under the definition of P&M as given in Explanation in Section 17/immovable as held in Nipro (supra), Varachha (supra) and Tianyin Worldtech India (P.) Ltd.[14] | ITC Admissible. The Fire protection work consists majorly of Fire extinguishers, fire hose reel, smoke/fire alarms, smoke/ heat detector, piping, sprinklers etc. Such inward supplies, in my view, are both movable as well as P&M (apparatus/ equipment/machinery). |

| H. | Electrical fittings such as Cables, Switches, NCB, Lighting system, Transformers, DG sets etc. | ITC inadmissible. Electrical fittings concealed into wall /floor of building, Transformer, Electrical Wiring/Fixtures, DG Sets, Sub-Station Work, DG Set Power Supply System, Lighting System Work, Emergency and Exit Light Fixtures, Telephone System, LAN System, after installation, are immovable properties – Varachha (supra), Tarun Realtors (supra) & Tianyin Worldtech (supra).

ITC Admissible on sub-Station, DG Set, Power Supply System, Lighting System, Emergency & Exit Light Fixtures, Main Feeder Distribution, Socket Outlet Work, Public Address System, Telephone System, Lightning Protection System, LAN System – Nipro (supra). ITC eligible on wires/ cables, electrical equipment etc. used for transmission of electricity from power station of DISCOM to factory – Elixir Industries (P.) Ltd.[15] |

The electrical fittings when fixed to the earth or the building or civil foundation by nuts and bolts does not get assimilated with the earth or building permanently. Such affixing is only for the purpose of maintaining stability and to keep it wobble-free without any disturbance. This act does not make in ‘immovable’.

Substantial portion of the electrical fittings viz. Cables, Switches, Electrical panel boards, Transformers, DG sets etc. are capable of being shifted from one place to another without causing much damage. The CBIC, in the context of Optical Fiber Cables (OFC) network, clarified that ‘PVC ducts’ and ‘manholes’ are covered under P&M. The Delhi High Court in Bharti Airtel Ltd. (supra) held that Telecommunication towers are ‘movable’. In my view, such electrical fittings are both ‘movable’ as well as covered under P&M. ITC Admissible. |

| I. | Roof solar plant | ITC Admissible. Roof solar plant is affixed to foundation via nuts and bolts and therefore is not an immovable property but a plant and machinery – Varachha (supra). | Solar plant held as ‘movable’ property would help ITC claim on other similar goods that are affixed to foundation for maintaining stability. Also, the decision that solar plant is P&M would help ITC claim on other similar inward supplies. ITC Admissible. |

| J. | HVAC, Air-Conditioning System | ITC Admissible since HVAC equipment on the production floor is required to adhere to cleanroom environment conditions – Nipro (supra).

ITC inadmissible on Chiller, Air Handling Units etc. since they are ‘immovable property’ and also not P&M – Tarun Realtors (supra) & Varachha (supra). Airconditioning equipment, after installation becomes a part and parcel of immovable property – Tianyin Worldtech (supra). |

ITC Admissible. The major components of HVAC such as chiller, cooling tower, pump and Air Handling Unit are fitted to the ground for safety and proper running. HVAC plant can be shifted from one place to another without any major damage.

In a separate issue, Nikhil Comforts[16] argued before the AAAR that HVAC results in an ‘immovable property’ and therefore ‘works contract’ U/s 2(119) taxable @ 18%; AAAR held that it is not an ‘immovable property’ and the entire contract is taxable @ 28%. The Apex Court in Jaiprakash Industries Ltd. (supra), in the context of Central Excise, held that air conditioning plant can be removed from one place to another and hence cannot be treated as ‘immovable’. |

7. CAN A PORTION OF INWARD SUPPLY BE SPLIT INTO ‘MOVABLE’ & ‘IMMOVABLE’?

In a contract for inward supply, can one portion be treated as ‘construction of an immovable property’ and the other ‘movable property’? YES, for example, in a contract for interior works involving false ceiling, supply of working/conference tables, detachable cubicles etc., ITC can be availed on such portion that is movable and that tantamount to P&M. In such cases, it is advisable to have separate costs for each item in the agreement.

8. ‘USED IN THE COURSE OR FURTHERANCE OF HIS BUSINESS’ VERSUS ‘USED FOR MAKING OUTWARD SUPPLY’

To ascertain eligibility of ITC, movable property should pass through the test of Section 16(1) and 17(5) and immovable property (P&M) should pass through the test of Explanation to Section 17. The language used in the respective Sections to ascertain eligibility of ITC is different, as follows:

| Movable property (Section 16) | Immovable property (Section 17) |

| ITC is eligible if the goods/services are ‘used in the course or furtherance of business’. | ITC is eligible if the goods/services (P&M) are ‘used for making outward supply’. |

Can all the apparatus, equipment and machine used in the business be treated as ‘used for making outward supply’? In my view, the term ‘used for making outward supply’ (Section 17) is as broad as and similar to that of the term ‘used in the course or furtherance of business’ (Section 16). It is to be noted that Explanation to Section 17 has not used terms like ‘directly used’, ‘exclusively used’ etc. to narrow down the scope of claim of ITC. A narrow meaning therefore cannot be attributed to the term ‘used for making outward supply’.

Hence, all goods and services (P&M) that are ultimately used for and have nexus with outward supply, are eligible for ITC. Needless to say that the said goods are not found in the negative list in Section 17(5). In Bharti Airtel Ltd. (supra), the Apex Court, while interpreting Rule 2(k) of the CENVAT Credit Rules, highlighted the glaring distinction in the definition of “input” for ‘output service providers’ and “input” for ‘manufacturers’. The Court observed that a simpler phrase was used for ‘output service providers’ as compared to ‘manufacturers’, as follows.

| For manufacture | For providing output service |

| Thus, “input” in relation to manufacturing of final product would mean not only those which are directly used but also indirectly used not only for manufacture of final product whether contained in the final product or not but also used in relation to manufacture of final product or for any of other purpose. | However, as mentioned above when “input” has been defined with reference to providing output service, the definition clauses does not explain it so elaborately but merely uses the simple expression i.e. “used for providing any output service”. |

The Apex Court agreed with the decision of the Delhi High Court in Bharti Airtel Ltd. (supra) which held that “…all goods” mentioned under Rule 2(k) of the CENVAT Rules would cover all the goods used for providing output services except those which are specifically excluded in the Rules. It held that the definition is wide enough to bring all goods which are used for providing any output service” (emphasis ours).

8.1 The language in Section 17 is similar to what was used in the erstwhile CENVAT Credit Rules, 2004 (‘used for providing output service’) and hence clear inference can bd drawn from the decisions laid down in the said law. In the author’s view, the term ‘used for making outward supply’ is wide enough to cover all such immovable property (i.e. P&M) which have both direct and indirect nexus to the outward supply.

8.2 What is a tax law without two views!? In Konkan LNG Ltd. [2024] 164 taxmann.com 167 (Bombay),the High Court held that breakwater construction wall near its port-jetty to enable LNG Ship berthing during monsoons was used ‘solely for protecting vessels during unloading’ and not ‘for making outward supplies’. Thus the Court attributed a narrow meaning to the term ‘used for making outward supplies’ for the purpose of Section 17(5).

9. CONCLUSION

Huge investments are flowing into and expected to flow into India for setting-up manufacturing facilities and provision of services. Consequently, the stakes on ITC on capital goods is also high. With lack of clarity in the law and varied interpretations by the AARs and AAARs, it is only obvious that Adjudicating authorities would dispute the ITC claim on such inward supplies, resulting in multiple litigations. Hence, it is imperative that the Government clarifies the issues/amends the law appropriately – for example, under the erstwhile CENVAT Rules, ITC was not available on ‘construction or execution of works contract of a building or a civil structure or a part thereof’ (excluded from the definition of ‘inputs’/’input services’). This reasonably clear and concise language could be borrowed by the GST law.

Notes:-

[1] [2023] 98 GST 460 (AAR – TELANGANA)

[2] [2022] 138 taxmann.com 343 (AAAR-MAHARASHTRA)

[3] [2024] 166 taxmann.com 456 (AAAR-TAMILNADU)

[4] [2024] 82 GSTL 77 (AAAR-GUJARAT)

[5] [2023] 153 taxmann.com 227 (AAAR – TAMILNADU)

[6] [2020] 81 GST 22 (AAR – MADHYA PRADESH)

[7] [2020] 37 GSTL 136 (AAAR-KARNATAKA)

[8] [2020] 120 taxmann.com 128 (AAAR-MAHARASHTRA)

[9] [1987] 163 ITR 274 (Gujarat)

[10] Advance Ruling No. GUJ/GAANN2O23II9 dt.12.05.2023

[11] [2021] 124 taxmann.com 428 (AAR – HARYANA)

[12] [2020] 116 taxmann.com 201 (AAAR-KARNATAKA)

[13] [2018] 18 GSTL 289 (AAR – MAHARASHTRA)

[14] [2022] 90 GST 586 (AAR – UTTAR PRADESH)

[15] [2024] 165 taxmann.com 19 (AAR – GUJARAT)

[16] [2020] 122 taxmann.com 14 (AAAR-MAHARASHTRA)

Author Bio

Exceptionally well-written. The depth of research is evident, and the clarity with which complex concepts are explained is truly impressive. It’s clear that a lot of thought and effort went into organizing the ideas and presenting them in a way that is both engaging and informative. I particularly appreciate how the writer takes the time to anticipate potential questions or doubts the reader might have, and addresses them in a very thoughtful manner. Overall, it’s a highly insightful and carefully crafted piece that not only educates but also captivates the reader from start to finish.