Point no-1

Whether we need to update the information and transition period in classification, every year?

As we know ministry of MSME has issued a notification as on 26th June 2020 which notifies certain criteria for classifying the enterprises as micro, small, and medium enterprise and specifying the form and procedure for filling memorandum w.e.f 1st July 2020.

So here the point of discussion is-

Updation of information and transition Period in classification

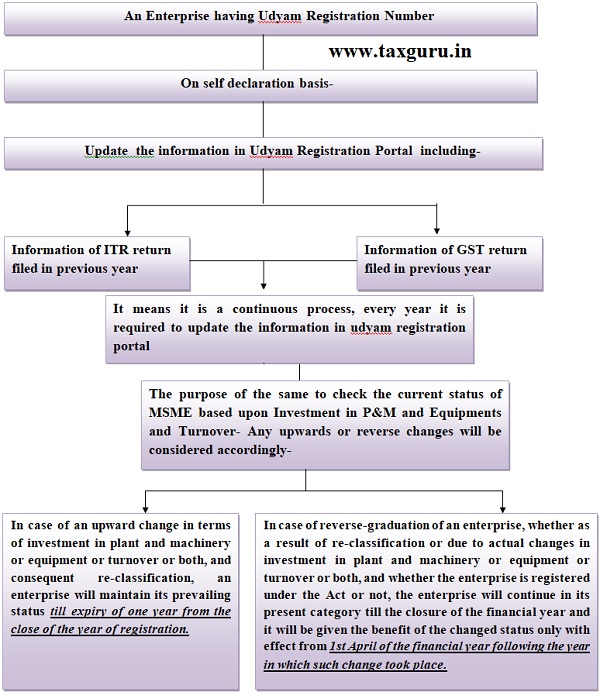

1. An enterprise having Udyam Registration Number shall update its information online in the Udyam Registration portal, including the details of the ITR and the GST Return for the previous financial year and such other additional information as may be required, on self declaration basis.

2. Failure to update the relevant information within the period specified in the online Udyam Registration portal will render the enterprise liable for suspension of its status.

3. Based on the information furnished or gathered from Government’s sources including ITR or GST return, the classification of the enterprise will be updated.

4. In case of graduation (from a lower to a higher category) or reverse-graduation (sliding down to lower category) of an enterprise, a communication will be sent to the enterprise about the change in the status.

5. In case of an upward change in terms of investment in plant and machinery or equipment or turnover or both, and consequent re-classification, an enterprise will maintain its prevailing status till expiry of one year from the close of the year of registration.

6. In case of reverse-graduation of an enterprise, whether as a result of re-classification or due to actual changes in investment in plant and machinery or equipment or turnover or both, and whether the enterprise is registered under the Act or not, the enterprise will continue in its present category till the closure of the financial year and it will be given the benefit of the changed status only with effect from 1st April of the financial year following the year in which such change took place.

Point No-2:

Whether there is required to file Form CFSS 2020 in case of any form or any documents filed for FY 2019-20 on or before 30th September 2020.

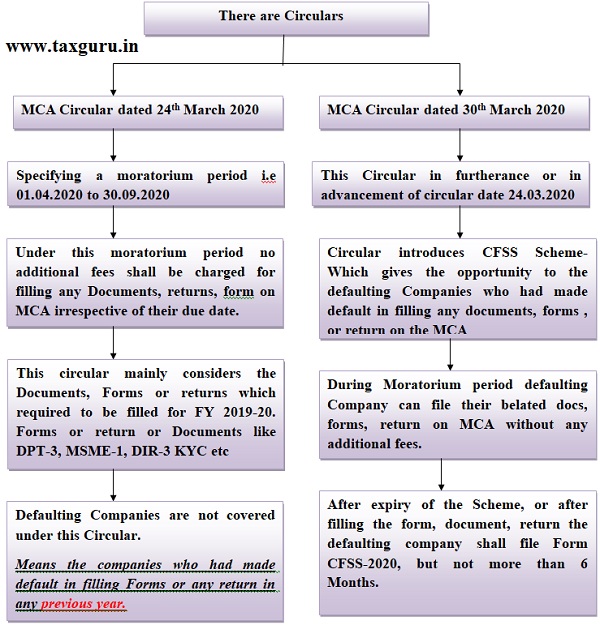

*Note- CFSS is not overriding the Circular dated 24.03.2020. CFSS is in furtherance of the Circular date 24.03.2020.

Hence as per the Circular dated 24.03.2020 the due date of filling documents, Return, & Forms (FY- 2019-20 whose due date was falling in between April 2020 to 30 Spt. 2020 in normal situation ) is 30th September 2020 Irrespective of their due dates, due to CoVID 19.

Hence, there is not any question of CFSS because CFSS is only for defaulting company and CFSS is in force from 1st April 2020 to 30th September 2020.

In such a case no need of filling CFSS relating to Documents, Returns or Forms whose due date was falling between April to Spt 2020 in normal situation because they already under moratorium period as per Circular date 24.03.2020 i.e the due date 30.09.2020.

CFSS is only for defaulting Company who had made default in filling documents, Forms, Returns, in any previous year.

Author Bio

If you read the circular dated 24.03.2020 read with 30.03.2020. It is very clear that 30.03.2020 is complete big form of moratorium. But for immunity it is mandatory to file CFSS form. You can raise such query with MCA also or can take opinion of any CS firm. use the law of interpretation.

Moratorium was simple combined circular. Which came with detailed scheme in cfss. Cfss also provide moratorium

Further if u say moratorium is there for all forms from April to September, then why ministry came with specific scheme for charged for April to Sept?

Bcoz if moratorium not overrides then charge form also part of moratorium and doesn’t required specific scheme

Circular dated March 23, 2020 talked about moratorium from April to Sep 2020 but linked it to fresh start (thereby not only covered new filings coming up as per due date but also the belated filings)

It also talked about the fact that circular specifying detailed requirements in this regard would be issued separately.

On March 30, Ministry issued a circular regarding CFSS.

Circular began w ith “ In Furtherance of the Circular dated 24th March….

And gone on talk about moratorium period (Apr to Sep) and compliance ritual i.e CFSS form filing.

Hence:

Moratorium period of Apr to Sep is for all filings( new and old forms); and

CFSS Form is required to be filed after Sep 2020 for all forms filed after due date : for example, if you file DPT 3 today- then you must fole CFSS form as there is a delay of 1 day.

Further if u read definition of defaulting companies in cfss circular its no where mentioned thay defaulting companies means which made default in filing of form till 31.3.2020.

As per definition if company fails to file any form, return, document shall be considered as defaulting company.

That form can be related to any period till duration of scheme i.e. 31.9.2020.