Reversal of Input Tax Credit if payment not made within 180 Days for the supplies

Clause 2 of the GST draft ITC rules, read with section 16 of CGST Act, 2017, deals with such transactions. The rule requires to furnish the details of such supply and the amount of input tax credit availed of in form GSTR-2, in the following month of such transaction. It requires this shall be added to the output tax liability.The rule also provides such reversed amount is available for re-credit once the payment for the supplies are made.

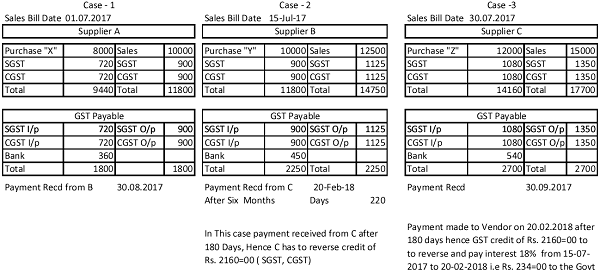

In this case, eventhough C has not paid to B within time, “C” has discharged GST liability, i.e. Rs. 450=00 has been paid to the Government for July Liability. Govt has received their GST on time. Actually “C” is suffered for Cash flow in this transaction. The Interest of Rs. 234=00 on late payment to “C” is taken by Government. Even though Govt has not loosed a single paisa, Govt taken interest portion from “C”. The Interest paid to Government by “C” should be credited to Mr. “B” credit ledger.

cannot understand