INPUT TAX CREDIT

(Chapter-V of Model GST LAW)

Relevant Definitions –

1. Taxable Person –

Means a person who carries on any business at any place in India/State of …………….. and who is registered or required to be registered under Schedule III of the Act. [Section 2(96) r/w section 9]

2. “Input tax in relation to taxable person, means

i. The( IGST & CGST/IGST & SGST) charged on any supply of goods and/or services to him

ii. Which are used,or intended to be used

iii. In the course or furtherance of his business

iv. And includes the tax payable under reverse charge[Section 2(57)]

3. Electric Credit Ledger:-

The input tax credit ledger in electronic form maintained at the common portal for each registered taxable person in the manner as may be prescribed in this behalf.[Section 2(41)]

Section 16(1)

Every registered taxable person be entitled to take credit as the manner specified u/s 35 of input tax admissible to him &

The said amount shall be credited to the electronic credit ledger of such person.

Section 35 :- Manner of utilization of Credit:-

The amount available in the electronic credit ledger may be used for making any payment towards tax payable under the Act or Rules. The manner of utilization, conditions and time

lines would be prescribed.

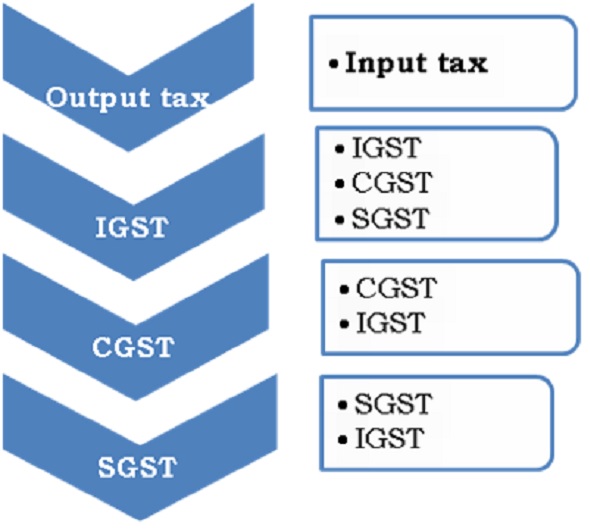

The Electronic Credit Ledger has only three Major Heads of Credit:

Hence cross-utilization of credit in respect of CGST & SGST is not admissible i.e., the CGST credit cannot be utilized for payment of SGST and vice versa.

Illustration:-

Let us assume, rate of CGST @ 10%, SGST @10% and IGST @20%

| Particulars | A

(Maharashtra) |

B

(Maharashtra) |

C

(Madhya Pradesh) |

| Tax Invoice

A -> B B -> C C->Customer |

Cost of goods Rs. 100 + CGST @10% Rs. 10 + SGST @10% Rs. 10 Total Rs. 120 |

Cost of Goods Rs. 200

+ IGST @20% Rs. 40 Total Rs. 240 |

Cost of goods Rs. 300 + CGST @10% Rs. 30 + SGST @10% Rs. 30 Total Rs. 120 |

| Credit Utilisation |

Payment of IGST Rs. 40 LESS – CGST @10% Rs. 10 SGST @10% Rs. 10 Payable in Cash Rs. 20 |

Payment of CGST Rs. 30 Less -IGST Rs. 30 Balance Payable NIL Payment of GST Rs. 30 Less IGST Rs. 10 Balance SGST payable Rs. 20 |

2. Eligibility of input tax credit on inputs held in stock and contained in semi-finished and finished goods held in stock: The credit on inputs held in stock and inputs contained in semi-finished goods and finished goods held in stock is available in the following manner:

| S.N. | Eligible persons | Credit entitled | As on | Restriction/conditions |

| 1 | Person applied for registration within 30 days from the date of liability to pay tax register and registered | Inputs held in stock and inputs contained in semi-finished or finished goods held in stock

|

The day immediately preceding the date from which he becomes liable to pay tax | -> Cannot avail credit of goods and/or services after 1 year from tax invoice date

-> The amount of credit calculated as per GAAP |

| 2 | Person applied for registration after 30 days from the date of liability to pay tax, registers and registered

|

NA | NIL | |

| 3 | Person who is not required to register, but obtains voluntary registration | required to register, but obtains voluntary Inputs held in stock and inputs contained in semi-finished or finished goods held in stock

|

The day immediately preceding the date of registration | |

| 4 | Person ceases to pay composition tax Inputs held in stock and inputs contained in semi | finished or finished goods held in stock The day immediately preceding the date from which he becomes liable to pay tax under regular scheme | Person ceases to pay composition tax Inputs held in stock and inputs contained in semi |

3. No input tax credit shall be allowed after the expiry of one year from the date of issue of tax invoice.

4. proportionate credit:-

The goods & / or services are used by the register taxable person partly for

|

Particulars |

Credit Admissible |

| Business & taxable supplies (including zero – related supplies) | Credit Allowed |

| Other purpose & non-taxable supplies (including Exempt supplies) | Not Allowed |

5. In case of Sale, merger, Amalgamation, Lease or Transfer of the Business input tax credit remains unutilized in the books of accounts allowed to be transferred.

6. Conditions for availing input tax credit

1. Registered Taxable person must be in possession of a tax invoice, debit note, supplementary invoice.

2. He has received the goods and / or services.

3. the tax charged has been actually paid to the credit of appropriate Government by supplier and

4. Return u/s 27 has been filed.

Where the goods against an invoice are received in lots or installments, the register taxable person shall be entitle to the credit upon receipt of last lot of installment.

Here, the condition of 1 year for the date of issue of tax invoice for availing the credit is not applicable.

7. In case of supply of capital goods taxable person shall pay

i. an amount equal to input tax credit taken on such capital goods reduced by the percentage points as may be specified or

ii. transaction value of such capital goods which ever is higher.

8. A taxable person shall not be entitled to take input tax credit in respect of any invoice for supply of goods and/or services, after the filing of the return under section 27 for the month of September following the end of financial year to which such invoice pertains or filing of the relevant annual return, whichever is earlier.

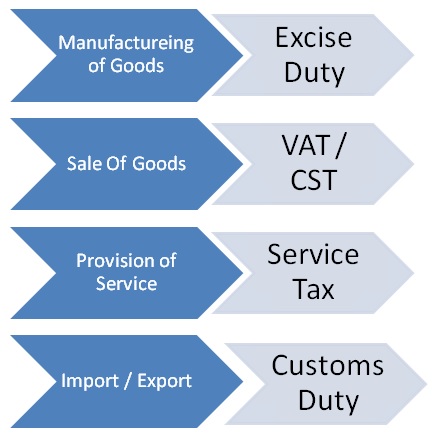

Current Tax Structure

Under GST Regime

SECTION 16A –TAKING INPUT TAX CREDIT IN RESPECT OF INPUTS SENT FOR JOB WORK

1) ENTITLEMENT OF CREDIT ON INPUTS & CAPITAL GOODS:-

A) INPUTS:-

i) The principal can take credit of input tax on inputs sent to job-worker for job work provided that the inputs,after completion of job-work are received back by him within 180 days of their being sent out.

ii) If input are sent directly to job-workers place without bringing to principal’s place of business-180 days counted from the date when it is received by job-worker

B) CAPITAL GOODS:-

i) The principal can take credit of Input Tax on Capital goods sent to job-worker,provided that the Capital Goods after completion of job-work received back by him within 2 years of being their sent out.

ii) If Capital Goods are sent directly to job-workers place without bringing to principal’s place of business-2 years counted from the date when it is received by job-worker.

Under the present tax system:-

Under Rule 4(6) of CENVAT CREDIT RULES 2004, final products are allowed to be cleared from the premises of job worker after the prior approval of Deputy Commissioner or the Assistant Commissioner of Central Excise (valid for three financial years) same provision not provided under GST LAW-SO what about credit admissibility under GST if the final product cleared from job-worker premises only.

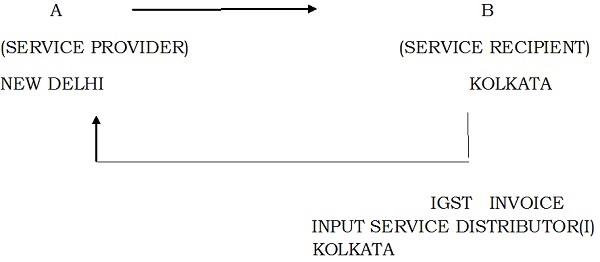

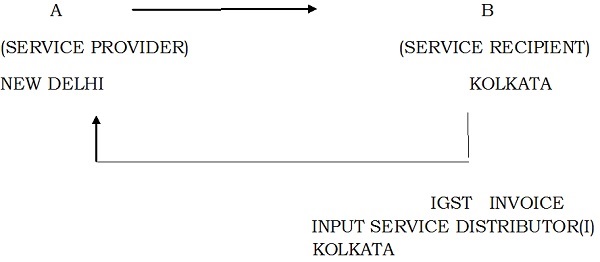

SECTION 17. MANNER OF DISTRIBUTION OF CREDIT BY INPUT SERVCIE DISTRIBUTOR(ISD):-

INPUT SERVICE DISTRIBUTOR:-

As per section 2

“Input Service Distributor” means an office of the supplier of goods and / or services which receives tax invoices issued under section 23 towards receipt of input services and issues tax invoice or such other document as prescribed for the purposes of distributing the credit of CGST (SGST in State Acts) and / or IGST paid on the said services to a supplier of taxable goods and / or services having same PAN as that of the office referred to above;

Explanation.- For the purposes of distributing the credit of CGST (SGST in State Acts) and / or IGST, Input Service Distributor shall be deemed to be a supplier of services.

THE ISD MAY DISTRIBUTE THE CREDIT SUBJECT TO THE FOLLOWING CONDITIONS;-

namely:

(a) the credit can be distributed against a prescribed document issued to each of the recipients of the credit so distributed, and such invoice or other document shall contain such details as may be prescribed;

(b) the amount of the credit distributed shall not exceed the amount of credit available for distribution;

(c) the credit of tax paid on input services attributable to a supplier shall be distributed only to that supplier;

(d) the credit of tax paid on input services attributable to more than one supplier shall be distributed only amongst such supplier(s) to whom the input service is attributable and such distribution shall be pro rata on the basis of the turnover in a State of such supplier, during the relevant period, to the aggregate of the turnover of all such suppliers to whom such input service is attributable and which are operational in the current year, during the said relevant period.

Explanation –

For the purposes of section 17 and this section, the relevant period shall be-

(a) if the recipients of the credit have turnover in their States in the financial year preceding the year during which credit is to be distributed, the said financial year; or

(b) if some or all recipients of the credit do not have any turnover in their States in the financial year preceding the year during which the credit is to be distributed, the last quarter for which details of such turnover of all the recipients are available, previous to the month during which credit is to be distributed.(why allocation as per preceding year T/O)

A ) Distribution of credit where ISD & recipient of credit are located within the state:-

Section 17(2)

The Input Service Distributor may distribute, in such manner as may be prescribed, the credit of CGST and IGST as CGST, by way of issue of a prescribed document containing, inter alia, the amount of input tax credit being distributed or being reduced thereafter, where the Distributor and the recipient of credit, being a business vertical, are located in the same State. – CGST ACT

The Input Service Distributor may distribute, in such manner as may be prescribed, the credit of SGST and IGST as SGST, by way of issue of a prescribed document containing, inter alia, the amount of input tax credit being distributed or being reduced thereafter, where the Distributor and the recipient of credit, being a business vertical, are located in the same State. – SGST ACT

i) Under CGST & SGST ACT – Distribution of IGST

As in ISD definition itself it has been provided that ISD is deemed supplier of service then credit of IGST will be distributed as CGST & SGST under CGST Act & SGST Act respectively (within the state)

The intension of government is only to avoid revenue loss as if IGST would have been distributed as IGST only then while utilizing it against SGST state would have lose revenue.

II) Under CGST & SGST Act distribution of CGST & SGST

i.) CGST will be distributed as CGST under CGST Act &

ii) SGST will be distributed as SGST & SGST Act .

B) Distribution of Credit where ISD & recipient of credit are located in different states:-

SECTION 17(1)

The Input Service Distributor may distribute, in such manner as may be prescribed, the credit of CGST as IGST and IGST as IGST, by way of issue of a prescribed document containing, inter alia, the amount of input tax credit being distributed or being reduced thereafter, where the Distributor and the recipient of credit are located in different States. – CGST ACT

The Input Service Distributor may distribute, in such manner as may be prescribed, the credit of SGST as IGST by way of issue of a prescribed document containing, inter alia, the amount of input tax credit being distributed or being reduced thereafter, where the Distributor and the recipient of credit are located in different States. – SGST ACT

i) Under CGST & SGST Act-Distribution of IGST

i) IGST will be distributed as IGST

II) Under CGST & SGST Act- Distribution of CGST & SGST

NO SEPARATE PROVISION IN RESPECT OF OUTSOURCED MANUFACTURED UNITS IN GST LAW AS IN CURRENT LAW.

SEC 18-MANNER OF RECOVERY OF CREDIT DISTRIBUTED IN EXCESS:- ( section relevant to ISD cr.distribution only in other cases of excess credit or wrong credit utilization sec. 51 )

If input service distributor distributes the credit in excess Shall be recovered from such distributor along with interest as per section 36 & provisions of section 51 apply mutatis-mutandis for effecting such recovery.

Sec 51-… Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized

Sec 18(1) :- deals with a situation where the credit distributed is in excess of what was available for distribution whereas

Sec 18(2) :- deals with a situation where the distribution is correct but one of the locations gets more than what is entitled to.