Tax policies play an important role on the economy through their impact on both efficiency and equity. A good tax system should keep in view issues of income distribution and, at the same time, also endeavor to generate tax revenues to support government expenditure on public services and infrastructure development.

Background –

Presently, the Central Government Levies Taxes – Central Excise Duty (on Manufacture of certain goods), Service Tax (on provision of certain services), Central Sales Tax (on Inter-State Sale of goods) & Similarly, the State Government levy tax on and on retail sales in form of Value Added Tax, entry of goods in the State in the form of entry tax, luxury tax, purchase tax etc.

There is a Cascading effect in present scenario since taxes levied by the Central Government are not available as set off against taxes being levied by the State Government & similarly certain taxes levied by State Government are not allowed as set off for payment of other taxes being levied by them.

Due to Cascading tax revenues, there is a differential impact on firms in the economy with relatively high burden on those not getting full offsets.

This argument can be extended to international competitiveness of the adversely affected sectors of production in the economy. Such domestic and international factors lead to inefficient allocation of productive resources in the economy. This results in loss of income and welfare of the affected economy.

For a developing economy like India it is desirable to become more competitive and efficient in its resource usage. Apart from various other policy instruments, India must pursue taxation policies that would maximize its economic efficiency and minimize distortions. Considering the fact, Kelkar Committee first recommended introduction of GST(by subsuming all the above mentioned indirect taxes–which would instantly spur economic growth)in India in 2004.

Introduction –

Introduction of GST would be a very significant step in the field of indirect tax reforms in India. By amalgamating a large number of Central and State taxes into a single tax and allowing set-off of prior-stage taxes, it would mitigate the ill effects of cascading and pave the way for a common national market.

“For the consumers, the biggest gain would be in terms of a reduction in the overall tax burden on goods, which is currently estimated at 25%-30%”

Introduction of GST would also make our products competitive in the domestic and international markets. There may also be revenue gain for the Center and the States due to widening of the tax base, increase in trade volumes and improved tax compliance.

Implementation of GST triggers the change in the Indian Tax structure and also the need arises to reorganize and renovate the business processes (which can be considered as an emerging opportunity to CA’s)

Genesis –

An announcement was made by the then Finance Minister Shri Chidambaram, in the Budget 2006-07, that GST would be introduced from April 1, 2010. Joint Working Groups of officials having representation of the States as well as the Center was set up to examine various aspects of the GST and draw up reports. Based on discussions within and between it and the Central Government, the Empowered Committee (which had formulated the design of State VAT was requested to come up with a road map & structure for the GST) released its First Discussion Paper on the GST in November, 2009. This spells out the features of the proposed GST and has formed the basis for discussion between the Center and the States so far.

Cut to the year 2016 when finally the Constitutional Amendment Bill on GST was passed by both the houses of parliament empowering Center and States to concurrently tax the supply of goods or services. “Yes, India being a federal republic consisting of states and Union territories opted for a dual model of GST” After much political squabbling and two central elections, GST is finally going to become a reality.

Goods & Service Tax –

GST (Proposed to be levied at all stages right from Manufacture up to final consumption with credit of taxes paid at previous stages available as set off – which minimizes the chance of Revenue Leakage) would be applicable on the supply of goods or services as against the present concept of tax on the manufacture and sale of goods or provision of services.

It is a Destination based tax on consumption of Goods & Services.

GST in India –

Ideally GST is implemented in a nation without state boundaries. In an ideal model of GST, there is no conflict of administrative power over the indirect tax. There is a single authority. An ideal GST can be a Central GST or a State GST.

India being a federal republic consisting of states and Union territories has opted for a dual model of GST where tax will be levied by the centre (CGST) and states (SGST) concurrently.

The Constitution (One Hundred and First Amendment) Act, 2016, through Article 246A and Article 269A of the constitution gives powers to the Union and State Government to levy and collect Goods and Service Tax.

Taxes on Alcoholic liquor for human consumption are not subsumed under GST and they are subject to State Excise Duties.

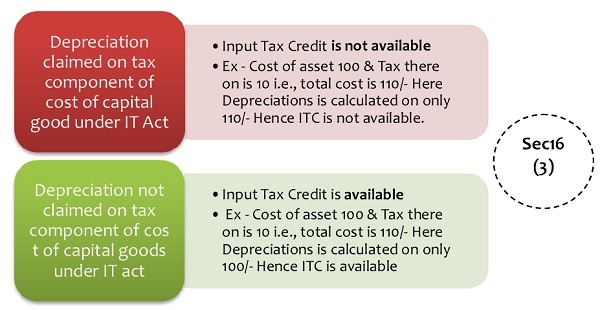

Chapter V – Input Tax Credit {It means credit of input tax}

Input Tax Credit is back bone of the GST regime & can be said as a mechanism to avoid cascading effect of taxes i.e., ‘tax on tax’. The procedures & restrictions laid down here are important to ensure seamless flow of credit in the whole scheme of taxation without any misuse.

| Section 16 | Section 17 | Section 18 |

| Eligibility & Conditions for taking ITC | Apportionment of credit & blocked Credits | Availability of Credit in special circumstances |

| Section 19 | Section 20 | Section 21 |

| Taking input tax credit in respect of inputs and capital goods sent for job work | Manner of distribution of credit by Input Service Distributor | Manner of recovery of credit distributed in excess |

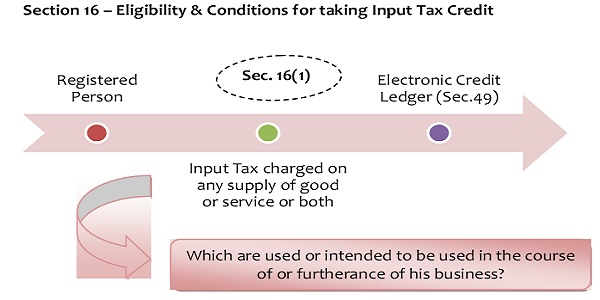

Section 16 – Eligibility & Conditions for taking Input Tax Credit

(a) Credit should be taken until the receipt of last instalment of goods (in case of goods received in instalments against a single invoice)

(b) Failed – amount equal to ITC availed along with interest will be added to output liability & such non payment of the value of invoice must be admitted in return filed for the month immediately following the period of 180 days from the date of issue of invoice.

* The said condition doesn’t apply for supplies which are payable under reverse charge basis.

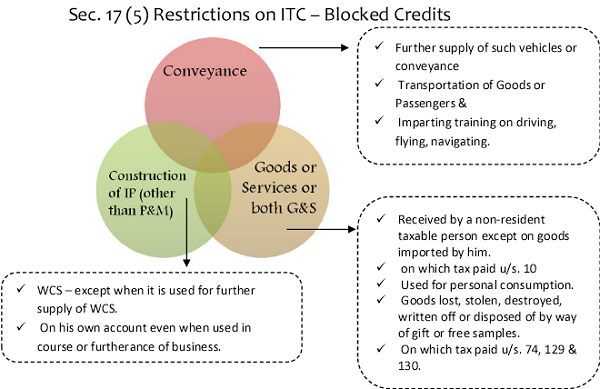

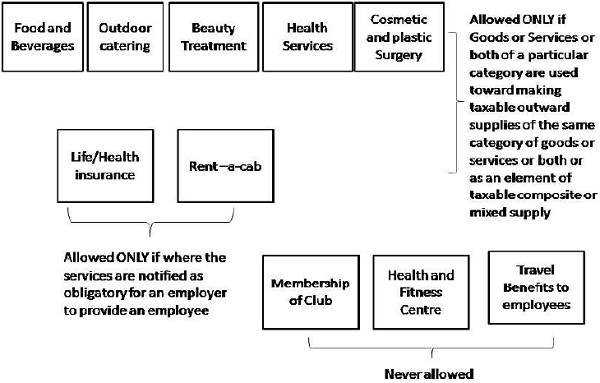

Section 17 – Apportionment of credit and blocked credit

ITC eligibility – based on usage in Business –

ITC eligibility – based on use of Inputs –

* Exempt Supply – Supply on which tax is paid on Reverse Charge, Transaction in securities, Sale of land and sale of building subject to clause (b) of Paragraph 5 of Schedule II.

Sec. 17 (5) Restrictions on ITC – Blocked Credits

Sec. 17 (6) – the government may prescribe the manner in which the credit referred to in sub sections (1) & (2) may be attributed.

Section 18 – Availability of credit in special circumstances

Registered Person – only Sec. 16(1) – admissible to take ITC, which will be credited to the Electronic Credit Ledger.

• Declaration in Form GST ITC 1 must be filled within 30 days from the date of becoming eligible to Input Tax Credit.

• Rule 5 requires a declaration to be filed containing details of stocks and capital goods along with a certificate from a Chartered Accountant or Cost Accountant where the credit so claimed exceeds Rs.2 Lakhs.

• Credit on Capital goods shall be reduced by five (5) % per quarter or part thereof from the date of invoice.

• Such credits are subject to verification of details furnished by the supplier in GSTR – 1 or GSTR – 4 on the common portal.

• Sec.18 (2) – Registered Person shall not be entitled to take ITC in respect of supply of goods or services or both to him after expiry of the one year from the date of issue of tax invoice relating to such supply.

• Change in constitution of registered person(Sec. 18 (3))

• Switches over from regular scheme to composition scheme – Pay & Exit Sec. 18 (4)

- Pay an amount by debiting Electronic Credit Ledger or Electronic Cash Ledger equivalent to ITC of Inputs held in stock, Inputs contained in Semi-finished or finished goods & capital goods on the day immediately preceding the date of such switch over.

- After payment balance of ITC in ECL– Lapse.

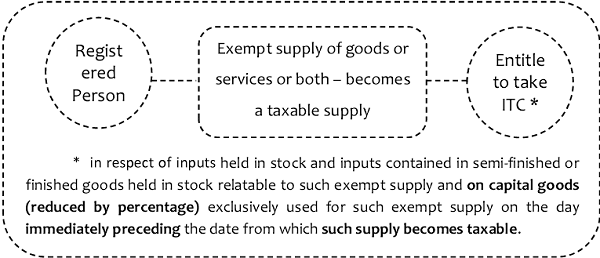

- The above provision is also applicable where goods or services supplied by registered person are absolutely exempt.

• Supply of Capital Goods or Plant & Machinery on which ITC already taken Sec.18 (6)

- ITC availed earlier (reduced percentage of deduction as may be specified) or

- Tax on Transaction value – whichever is higher.

Section 19 –Input Tax credit for Job work

• If the inputs/capital goods are not received back within one/three years (as the case may be) – it shall be deemed that such inputs had been supplied by the principal to Job Worker on the day when the said inputs were sent out.

• Rule 10 of ITC Rules are to be followed –

- Issue a challan (contain all details as required of an Invoice in Rule 8 of Invoice Rules) for transfer of inputs to the job-worker (to maintain paper trail of transaction)

- All challans issued in respect of inputs sent to job-worker and those received back are to be reported in GSTR-1

- In case of non receipt of the inputs within the time prescribed, the challan issued will be deemed to be invoice for the implied supply of inputs.

• Time limit is not applicable to moulds and dies, jigs and fixtures & tools.

Section 20 –Manner of distribution of Credit by Input Service Distributor

Procedure for distribution is given in Rule 4 of Input Tax Credit rules –

1) An Input Service Distributor shall distribute input tax credit in the manner and subject to the conditions specified below

a) The input tax credit available for distribution in a month shall be distributed in the same month and the details thereof shall be furnished in FORM GSTR-6 in accordance with the provisions of Chapter (Return Rules);

b) The input tax credit that is required to be distributed to one of the recipients ‘R1’, whether registered or not, from among st the total of all the recipients to whom input tax credit is attributable, including the recipient(s) who are engaged in making exempt supply, or are otherwise not registered for any reason, shall be the amount, “C1”, to be calculated by applying the following formula:-

C1 = (t1÷T) × C

Where,

“C” is the amount of credit to be distributed,

“t1” is the turnover, as referred to in section 20, of person R1 during the relevant period, and “T” is the aggregate of the turnover of all recipients during the relevant period;

Relevant Period –

(Author Abhinava Bhavani Prasad is a CA-Final Student, currently serving as an Article Trainee at Ganesh Prasad Chartered Accountants, Chennai & serving as an executive committee member of Chennai SICASA.)

Author Bio

can i claim input tax on repairing of building if yesor no which section

The goods rejected by us then sent the goods of party by Tax Invoice or Debit Note for taken the input tax credit. pl give me the positive response at my mobile & my mobile number – 9310955964

Reject raw material on tax invoice or debit note for taken the input tax credit as per Gst Act,

Please advise whether input tax credit is available to Cooperative Housing Society for sourcing goods & services or both for personal consumption of members.