Want for pile of information, abysmal Infrastructure, resistance to the simplicity, stringent timelines, want of tax, Uncool Performa of GSTR 1, 2 and 3 – sum it up and you get GSTR 3B. The name GSTR 3B was first heard sometime in April 2017, when the 2nd version of draft return rules were released. While the specified format as is prevalent today, didn’t came out until the final rules were published vide Notification No. 10/2017-CT dated 28 June 2017.

Since the very first due date of the very first GSTR 3B (July 2017), the times have been chaotic. The format of return is very casual and tries to capture as much information as possible in the garb of consolidated figures. In my heart of hearts, add a few more information and this return could be an ideal regular return through-out. Anyways, as the things got going, the return errors multiplied in numbers. As per the published figures, the patterns shows that on an average only 60% taxpayers have been able to file the GSTR 3B returns for all the months. Let’s set one thing straight, GSTR 3B once submitted/ filed, is not revisable (credit goes to the structure of GSTN), any error has to be corrected in the subsequent months’ return. Owing to countless difficulties faced by trade, the Central Government issued Circular 26/2017-CT dated 29 Dec 2017 to apprise the trade as to how the errors of GSTR 3B are to be corrected/ rectified. Through the present article and a sample data, an attempt has been made to bring out about logics as to how the errors in GSTR 3B should be corrected/ rectified.

1. The Logics

There are some principles articulated after handling some messed up cases, they could be read in the beginning or at the end. At the end final adjustment months’ GSTR 3B;

- The figures in GSTR 3B are bound to differ from GSTR 1 and GSTR 2, GST 3 (if any), so necessary reconciliations would be part of life

- All Adjusted Tax Liabilities (Forward Charge) should be equal in total compare to the Correct Tax Liabilities (Forward Charge) – All Taxes individually as well as consolidated

- All Adjusted Tax Liabilities (Reverse Charge) should be equal in total compare to the Correct Tax Liabilities (Reverse Charge) – All Taxes individually as well as consolidated

- At the Input Tax Credit should be equal in total compare to the Correct Input Tax Credit

- There should never be a “Negative Figure” in any field (the website doesn’t allow you to put negatives anyways)

- All Adjusted Debits in Electronic Cash Ledger (‘ECaL’) should be equal in total compare to the Correct Debits in ECaL – All Taxes in consolidated, however may differ monthly.

- All Adjusted Debits in Electronic Credit Ledger (‘ECrL’) should be equal in total compare to the Correct Debits in ECrL – All Taxes in consolidated, however may differ monthly.

- Availing of ITC can be deferred to avoid absurd tax positions and refund formalities

- 2. Sample Correction Sheet

- 3. Understanding the Performa of GSTR 3B

- 4. Understanding CBEC Circular 26/2017-CT dated 29 Dec 2017

- 5. Corrections of Errors

- 5.1 Over-reporting of RCM Liability

- 5.2 Under-reporting of RCM Liability

- 5.3 Over-reporting of FCM Liability

- 6. Reporting corrections for Exports Supplies

- 6.1 Export under Rebate:

- 6.1.1. Export Supplies not reported in GSTR 3B altogether:

- 6.1.2 Export Supplies under-reported in GSTR 3B:

- 6.1.3 Export Supplies over-reported in GSTR 3B:

- 6.2 Export under LUT/ Bond:

- 6.2.1 Export Supplies not reported in GSTR 3B altogether:

- 6.2.2 Export Supplies under reported in GSTR 3B:

- 6.2.3 Export Supplies over reported in GSTR 3B:

- 7.1 Over-Reporting of ITC

- 7.2 Under-reporting of ITC

- 8. Other considerations:

2. Sample Correction Sheet

A Sample Excel Sheet can be found at

https://taxguru.in/wp-content/uploads/2018/05/GSTR-3B-Corrections.xlsx wherein sequential adjustments have been in succeeding months’ GSTR 3B to rectify the errors of over-reporting of Output tax (FCM), Under-reporting of Output Tax (RCM) and Over-reporting of ITC (FCM). The sheet also forms the basis of some illustrations below;

3. Understanding the Performa of GSTR 3B

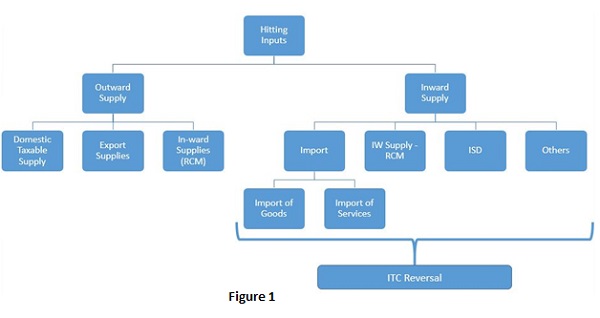

GSTR 3B as ridiculous as it appears, happens to be twice the pain. On the face of it, GSTR 3B is divided in 5 Tables, out of which only 3 hits tax calculation, meaning thereby the rest of the 2 are un-necessitated anarchy. The division of 2 relevant tables can be understood by following diagram;

As can be seen, there are 2 Tables, which hits the calculation of tax in a return i.e. Outward Supplies and ITC – Inward Supplies. The function of these 2 makes up the 3rd Table – Offsetting Table, which is merciless. Therefore all caution should be exercised while filing these Tables.

The 2 Tables are further sub categorized into numerous specific information. A closer looks makes it clear that all specific information that are sought, is individually linked with some imitating information sought in GSTR 1 and GSTR 2.

4. Understanding CBEC Circular 26/2017-CT dated 29 Dec 2017

The impugned Circular tends to classify errors in 7 types and provides resolution through the adjustment of subsequent month(s) returns. The circular then makes a matrix of these 7 errors based on the status of return at the time of error viz. (1) Figures can be edited (2) ECaL error (3) 3rd Table – Off setting has been done (4) Return has been Filed.

The errors at first 2 status viz. (1) When Editing is alive is rectifiable in the same months’ returns itself in as much as the portal permits the correction before Off setting of liabilities while (2) the error at ECaL is an error of wrong deposits. The core issues discussed herein are the cases where GSTR 3B has been off-set/ Submitted/ Filed. The rectifications principles at (3) and (4) stage viz. After Off-set/ Submitted/ Filed, discussed in the circular are briefed as below;

| S. No. | Error | Resolution | Interest Implications |

| 1 | Liability is under-reported | Liability may be added in the return of subsequent month(s). | Interest Payable |

| 2 | Liability is over-reported | (1) Liability may be adjusted in return of subsequent month(s) or

(2) Refund may be claimed where adjustment is not feasible. |

No |

| 3 | Liability is wrongly reported | (1) Under-reported liability may be added in next months’ return

(2) Over-reported liability may be adjusted in the return of subsequent month(s) or Refund may be claimed where adjustment is not feasible |

Interest Payable on under-reported liability |

| 4 | ITC is under-reported | Un-availed ITC may be availed in subsequent month(s) return | No |

| 5 | ITC is over-reported | Pay (through cash) / Reverse such over reported ITC in return of subsequent month(s) | Interest Payable |

| 6 | ITC taken wrongly | (1) Un-availed ITC may be availed in subsequent month(s) return

(2) Pay (through cash) / Reverse such over reported ITC in return of subsequent month(s) |

Interest Payable on over-reported ITC |

| 7 | Incorrect payment in ECaL Tax-Codes | No Correction required in GSTR 3B, though following actions may be taken;

(1) Add Cash to correct Tax-Code (2) Carry Forward Excess deposited Tax or claim Refund |

No |

5. Corrections of Errors

With above background, illustrations can be discussed vis-à-vis implementation of above Circular at the same time attempting some synch with GSTR 1. At the same time common perceptions are also dealt with.

5.1 Over-reporting of RCM Liability

As can be drawn from Figure 1, it can be seen that Table 1 (Outward Taxable Supplies) contain 3 different information viz. (1) Outward Taxable supplies (2) Export Supplies (3) Inward Supplies taxable under RCM. In case an error has been committed in any of these field, the rectification in next months’ GSTR 3B should be done in the same particular field only. Take for an example, that inadvertently IGST-RCM tax in July GSTR 3B was over-reported as INR 100,000 instead of INR 20,000. Reference is drawn to S. No. 2 of the Circular to rectify such error. As per the resolution provided, INR 80,000 of IGST-RCM tax can be reduced in subsequent months’ return. Following cautions should be taken care of;

- Corresponding taxable value (if shown incorrectly) to INR 80,000 should also be reduced in the adjustment month

- INR 80,000 is on account of IGST-RCM, therefore it should not be adjusted against CGST-RCM or SGST-RCM

- Reduction cannot be such that either of CGST-FCM, SGST-FCM, IGST-FCM becomes negative, therefore in case INR 80,000 are not exhausted in subsequent month, it should be carried forward for adjustment in next months’ GSTR 3B

- If needed necessary, any un-exhaustible amount of IGST-RCM may be adjusted against IGST-FCM, such adjustment seems to be permitted since the words used in Circular are “Liability” which covers both RCM Liability and FCM Liability.

- It would be incorrect to neutralize INR 80,000 by availing corresponding ITC credit in Table 3, since such availing of credit itself will be considered as an error of S. No. 5 of the Circular. Although such position may be tested judicially.

- After applying above adjustments, any un-exhaustible amount out of 80,000 should only be claimed as Refund only. The presumption of Unjust Enrichment can easily be rebutted in such case.

5.2 Under-reporting of RCM Liability

Under-reporting of RCM Liability is an error covered by S. No. 1 of the Circular. Any under-reporting in RCM say, IGST-RCM should be adjusted only with IGST-RCM of next months’ GSTR 3B. Suppose the amount of under-reporting of IGST-RCM is INR 50,000, important points while correcting such error are as follows;

- In case the corresponding taxable value filed should also be increased

- In case the corresponding taxable value filed was not under-reported: The taxable value field doesn’t accept “zero”, therefore in any case there is no RCM liability in subsequent months’ GSTR 3B, a notional amount of “INR 1” can be inserted along with IGST-RCM of INR 50,000

- On the face the circular, it is not mandatory that all the under-reported Liability should be added in the same month, subject to the payment of Interest, the amount of INR 50,000 may be added in any subsequent months’ disregarding non-adjustment in any month.

- In any case, INR 50,000 should not be added in IGST-FCM, since that would constitute a fundamental error of non-recognition of RCM Liability, moreover, it’s another error than correction. Besides, RCM Liabilities needs to be paid by debit in ECaL as per Rule 85 (4) of CGST Rules, 2017, while not so necessary the case with FCM Liabilities.

5.3 Over-reporting of FCM Liability

Over-reporting of FCM is an error covered by S. No. 2 above. Suppose CGST-FCM and SGST-FCM was over-reported as INR 40,000 instead of INR 10,000. Such over-reported INR 30,000 CGST-FCM and 30,000 SGST-FCM can be adjusted in subsequent months’ GSTR 3B, following may be kept in mind

- Corresponding taxable value should also be reduced, as the case maybe

- CGST-FCM and SGST-FCM moves in sync without deviation, therefore adjustments are also only accepted in synch In case the errors are 30,000 CGST-FCM and 27,000 SGST-FCM, it is recommended that both CGST-FCM and SGST-FCM of subsequent months should be reduced only by INR 27,000

- Reduction cannot be such that either of CGST-FCM, SGST-FCM, IGST-FCM becomes negative, therefore any un-exhaustible tax should be carry forward for adjustment in subsequent months’ GSTR 3B.

- In case there is no CGST-FCM in subsequent month, but there is CGST-RCM, INR 30,000 should not be reduced against CGST-RCM, since that would again amount to non-reporting of taxes of RCM, violating Section 9 (3), 9 (4) of Central Goods and Services Tax Act, 2017 (‘CGST Act’) as the case maybe.

5.4 Under-reporting of FCM Liability

Under-reporting of FCM Liability is an error covered by S. No. 1 above. Any under-reporting in FCM say, CGST-FCM should be adjusted only with CGST-FCM of next months’ GSTR 3B. Suppose the amount of under-reporting of IGST-FCM is INR 50,000, important points while correcting such error are as follows;

- In case the corresponding taxable value filed was also under-reported: Corresponding taxable value should also be increased

- In case the corresponding taxable value filed was reported correctly: The taxable value field doesn’t accept “zero”, therefore in case there is no FCM liability in subsequent months’ GSTR 3B, a notional amount of “INR 1” can be inserted along with IGST-RCM of INR 50,000

- On the face the circular, it is not mandatory that all the under-reported Liability should be added in the same month, subject to the payment of Interest, the amount of INR 50,000 may be added in any subsequent months’ disregarding non-adjustment in any month.

- In any case, INR 50,000 should not be added in IGST-RCM, one because that would necessarily require debit from ECaL, despite the fact sufficient ITC exist in ECrL, the other reason being to remain in sync with GSTR 1.

6. Reporting corrections for Exports Supplies

Regardless of errors, Export columns should be filed with every caution, in first place. But just in case, error occurs, rectification also needs to be exercised cautiously. Exports supplies can be affected in two ways (1) With taxes under Rebate or (2) Without taxes under LUT/ Bond.

6.1 Export under Rebate:

Export under Rebate prima facie means the taxpayer wants taxes back (from the government). Flurry of Circulars and Instructions have been issued under both GST Law as well as Customs Act regarding matching of particulars. All circulars correspond to the fact that Automatic Refund will be granted only when the specified Invoice and Shipping Bill particulars are contained and reconciled with GSTR 1 and consolidated amount is incorporated in corresponding GSTR 3B. Here is how errors on this count can be dealt with;

6.1.1. Export Supplies not reported in GSTR 3B altogether:

Since there is link up with GSTR 1, it is recommended that GSTR 3B should mirror GSTR 1. If Export supplies of July are not entered in GSTR 3B of February, they better be reported in GSTR 3B of March, furthermore, instead of reporting Invoice wise details in Table 6A of GSTR 1 of February, they should better be reported in Table 6A of GSTR 1 of March. Of course, Interest complications should be factored in. The purpose is to avoid Mismatches provided in Para 2 (iii) of Circular 05/2018-Customs dated 23 Feb 2018. Take an example, suppose 5 Export Invoices of IGST INR 10,000 each were raised in February, however, in GSTR 3B, tax was reported only INR 20,000. To rectify such error, in GSTR 3B of March INR 30,000 should be added in the export supplies column. Further 2 Tax Invoices should be reported in Table 6A of GSTR 1 of February, and 3 Tax Invoices should be reported in Table 6A of GSTR 1 of March so that both GSTR 1 and GSTR 3B mirror each.

6.1.2 Export Supplies under-reported in GSTR 3B:

The errors of under-reporting and over-reporting will necessarily lead to Physical Interface with the Jurisdictional Officer, more often in cases where reported amount qua Export Supplies reflect unmapped values. The best effort should be declaration of under-reported tax in GSTR 3B and mirror the same with GSTR 1. Suppose in above example, in February INR 15,000 were declared in Export supplies of GSTR 3B of March. Now it makes no difference that you over-report GSTR 3B of March with INR 30,000 or INR 35,000, since in any case, Refund to the tune of only INR 30,000 will be processed automatically. As far as balance of February’s refund goes, it appears that, manual refund process will have to be followed.

6.1.3 Export Supplies over-reported in GSTR 3B:

In case Export supplies of a particular months’ GSTR 3B have been over-reported, it is suggested that reduction-adjustment in subsequent months’ GSTR 3B should be done from the Domestic Tax amount, since that would not hurt the Export Value of that particular GSTR 3B. If the Tax on export supplies is reduced to cover up for the adjustment, it may again fall under the violation of Para 2 (iii) ibid. Further, the error resolution in S. No. 2 indicates towards “Liability” and not necessarily “Liability towards corresponding Column”.

6.2 Export under LUT/ Bond:

Export Turnover is required to be reported in GSTR 3B even if there is no tax. Although errors qua Export under Bond/ LUT doesn’t seems to be so obscure as compare to Export under Rebate, cautious exercise is always the heed, particularly a necessity if the taxpayer wishes to claim ITC Refund vis-à-vis Export Supplies. Errors on this count may be rectified as follows;

6.2.1 Export Supplies not reported in GSTR 3B altogether:

Again there is link up between GSTR 1 and GSTR 3B, one may refer the Refund Application Form RFD-01 on the portal. RFD-01, allows to be proceeded only when Export supplies are reported in the GSTR 3B. Take for an example, that if Export (Taxable) Value is not reported in GSTR 3B of February but Export Supplies under Bond are declared in Table 6A of GSTR 1 of February, even in such cases RFD-01 will not permit to proceed with ITC Refund because GSTR 3B is empty. Therefore GSTR 3B and GSTR 1 should mirror in this case also. Otherwise, Interface with Jurisdictional Officer will be required by filing Manual Refund Claim in Form RFD 01A.

6.2.2 Export Supplies under reported in GSTR 3B:

It is again a crime to under-report Export (Taxable) Value, if one wishes to go for Online Refund Claim. ITC refund vis-à-vis Export formula requires Export (Taxable) Value in the numerator and denominator, therefore if correct figure of Export Value is not punched, Refund calculation will be on lower side.[1] Any increase-adjustment in GSTR 3B of a month should mirror GSTR 1.

6.2.3 Export Supplies over reported in GSTR 3B:

Adjustment should be made for the sake of fulfilling governments’ attempt to exploit data analytics (For real). If ITC Refund is not to be claimed, reduction in GSTR 3B should ideally be through corresponding Export (Taxable) Value figures. In case ITC Refund is sought, reduction should be made from Domestic Taxable Values so as to not hurt the Export Value of that particular GSTR 3B

7. Corrections over Input Tax Credits

7.1 Over-Reporting of ITC

- No. 5 of Circular covers cases where ITC has been over-reported. ITC reporting in GSTR 3B has 5 major sub classifications, unlike, reporting of Outward Taxable supplies, ITC Table provides a residuary field for reversal of ITC. Therefore any over-reported ITC should be done through this field. Other important things that should be kept in mind;

- CGST-ITC should be reduced against CGST-ITC only, so is the case for SGST and IGST

- If reducible amount is more than the ITC entitlement of adjusting months’ GSTR 3B, it will add to the tax liability which will be payable through debit in ECaL

- For the sake of repetition, it is suggested that over-reported RCM-tax should not be corrected as over-reported RCM-ITC claim. Instead RCM-tax should be rectified in terms of S. No. 2 of the Circular only.

7.2 Under-reporting of ITC

S. No. 4 of the Circular covers cases of under-reporting of ITC. Unlike the over-reporting, the ITC should be increased-adjusted in subsequent months’ GSTR 3B only through the relevant field.

- CGST-ITC should be increased against CGST-ITC only, so is the case for SGST and IGST

- If Import-ITC of INR 10,000 of July was not taken in GSTR 3B of February, it should be taken in Import-ITC field of GSTR 3B of March, to avoid possible mismatches with the Bill of Entry data that is there on ICEGATE portal.

8. Other considerations:

After adjustments have been done, certain calculations should necessarily be undertaken to ensure the veracity of adjustments. Further these calculations helps to clear big misconceptions and apparent errors as well.

8.1 Total (Adjusted) Output Tax Payable in all GSTR 3Bs in question should come equal to the Total (Correct) Output Tax Payable. All taxes should be equal individually as well. Take for following table;

Total Output Debits (Adjusted) |

Total Output Tax (Correct) |

||||||||

IGST |

CGST |

SGST |

Total |

IGST |

CGST |

SGST |

Total |

||

July (Wrong) |

11253832 |

5626916 |

5626916 |

22507664 |

July |

125750 |

5632204 |

5632204 |

11390158 |

Aug(Adj.) |

5656 |

6603394 |

6603394 |

13212443 |

Aug |

1180416 |

6598107 |

6598107 |

14376629 |

Sept(Adj.) |

2333 |

6721773 |

6721773 |

13445879 |

Sept |

22732 |

6721773 |

6721773 |

13466278 |

Oct(Adj.) |

3125 |

5658760 |

5658760 |

11320645 |

Oct |

22081 |

5658760 |

5658760 |

11339601 |

Nov(Adj.) |

1400 |

7333042 |

7333042 |

14667484 |

Nov |

1731430 |

7333042 |

7333042 |

16397514 |

Dec(Adj.) |

26040 |

5742655 |

5742655 |

11511350 |

Dec |

5718783 |

5742655 |

5742655 |

17204093 |

Jan(Adj.) |

5642 |

6438302 |

6438302 |

12882246 |

Jan |

629798 |

6438302 |

6438302 |

13506402 |

Feb(Adj.) |

1895998 |

6085139 |

6085139 |

14066276 |

Feb |

3763036 |

6085139 |

6085139 |

15933314 |

Total |

13194025 |

50209981 |

50209981 |

113613987 |

Total |

13194025 |

50209981 |

50209981 |

113613987 |

In left hand side Table – July GSTR 3B, IGST Tax was wrongly over-reported by INR 11,128,162 (difference between corresponding figures in right hand side Table), owing to this error, IGST Liability in subsequent months have been adjusted-reduced and finally exhausted in Feb 2018. Now that all errors have been rectified, the sum total of IGST Liability over 8 months in equal in both the left Table and right Table. The under-reporting of CGST and SGST in July has been exhausted completely by over-reporting CGST and GST in August, hence subsequently, no adjustments are taken there forth.

8.2 Total (Adjusted) Debits from ECaL and ECrL should be in consolidation be equal to the Total (Debits) in ECaL and ECrL respectively, had, the returns be filed correctly. The difference in individual debits may differ, because of the sequence of adjustments. The example in following table can be of assistance;

Debits in Credit Ledger (Adjusted) |

Debits in Credit Ledger (Correct) |

||||||||

IGST |

CGST |

SGST |

Total |

IGST |

CGST |

SGST |

Total |

||

July (Wrong) |

8584408 |

4620222 |

3964186 |

17168816 |

July |

125670 |

4471648 |

3939064 |

8536382 |

Aug (Adjusted) |

(0) |

3250437 |

3906473 |

7156910 |

Aug |

1174840 |

5051259 |

3931595 |

10157694 |

Sept (Adjusted) |

(0) |

2612622 |

2612622 |

5225244 |

Sept |

20399 |

4957751 |

2612622 |

7590772 |

Oct (Adjusted) |

(0) |

3050738 |

3050738 |

6101476 |

Oct |

18956 |

5650453 |

3142708 |

8812117 |

Nov (Adjusted) |

0 |

7324613 |

3371639 |

10696252 |

Nov |

1730030 |

6490245 |

3031458 |

11251733 |

Dec (Adjusted) |

– |

5736975 |

3098045 |

8835020 |

Dec |

3456262 |

2689379 |

2689379 |

8835020 |

Jan (Adjusted) |

(0) |

6094667 |

3005768 |

9100435 |

Jan |

624156 |

5470511 |

3005768 |

9100435 |

Feb (Adjusted) |

1531521 |

3821273 |

3821273 |

9174067 |

Feb |

1531521 |

3821273 |

3821273 |

9174067 |

Total |

10115928 |

36511547 |

26830744 |

73458219 |

Total |

8681833 |

38602519 |

26173867 |

73458219 |

At the end of adjustment process, it can be seen above, debits in all Taxes individually differs on monthly basis from the ones that should have been there had, the returns been filed correctly. However the consolidated figures of Debits in ECrL in both the Tables comes equal (bar some rounding off errors). So is the case with the ECaL as below;

Debits in Cash Ledger (Adjusted) |

Debits in Cash Ledger (Correct) |

||||||||

IGST |

CGST |

SGST |

Total |

IGST |

CGST |

SGST |

Total |

||

July (Wrong) |

2669424 |

1006694 |

1662730 |

5338848 |

July |

80 |

1160556 |

1693140 |

2853776 |

Aug (Adjusted) |

5656 |

3352956 |

2696921 |

6055533 |

Aug |

5576 |

1546847 |

2666512 |

4218935 |

Sept (Adjusted) |

2333 |

4109151 |

4109151 |

8220635 |

Sept |

2333 |

1764022 |

4109151 |

5875506 |

Oct (Adjusted) |

3125 |

2608022 |

2608022 |

5219169 |

Oct |

3125 |

8307 |

2516052 |

2527484 |

Nov (Adjusted) |

1400 |

8429 |

3961403 |

3971232 |

Nov |

1400 |

842797 |

4301584 |

5145781 |

Dec (Adjusted) |

26040 |

5680 |

2644610 |

2676330 |

Dec |

2262521 |

3053276 |

3053276 |

8369073 |

Jan (Adjusted) |

5642 |

343635 |

3432534 |

3781811 |

Jan |

5642 |

967791 |

3432534 |

4405967 |

Feb (Adjusted) |

364478 |

2263866 |

2263866 |

4892210 |

Feb |

2231516 |

2263866 |

2263866 |

6759248 |

Total |

3078098 |

13698433 |

23379237 |

40155768 |

Total |

4512193 |

11607462 |

24036113 |

40155768 |

The Fun Fact is merely because Debits in ECaL and ECrL differs individually on monthly basis, however the sum of both Debits in a month equals to the Tax Liability for the same month [both for Adjusted Figures as well as Correct Figures]. Illustratively, CGST – Aug – 6,603,394 = 3,250,437 + 3,352,956, can try it for any month.

8.3 Total Credit Taken must be certainly be equal in both the scenarios viz. the adjusted figures doesn’t mean that any credit should be taken in excess.

Summary of Debits in Cash Ledger (Adjusted) |

Summary of Debits in Cash Ledger (Correct) |

||||||||

IGST |

CGST |

SGST |

Total |

IGST |

CGST |

SGST |

Total |

||

July (Wrong) |

8584408 |

4620222 |

3964186 |

17168816 |

July |

658254 |

3939064 |

3939064 |

8536382 |

Aug (Adj.) |

(0) |

3250437 |

3906473 |

7156910 |

Aug |

2294504 |

3931595 |

3931595 |

10157694 |

Sept(Adj.) |

(0) |

2612622 |

2612622 |

5225244 |

Sept |

2365528 |

2612622 |

2612622 |

7590772 |

Oct(Adj.) |

0 |

3050738 |

3050738 |

6101476 |

Oct |

2710641 |

3050738 |

3050738 |

8812117 |

Nov(Adj.) |

4633336 |

3031458 |

3031458 |

10696252 |

Nov |

5188817 |

3031458 |

3031458 |

11251733 |

Dec(Adj.) |

3456262 |

2689379 |

2689379 |

8835020 |

Dec |

3456262 |

2689379 |

2689379 |

8835020 |

Jan(Adj.) |

3088899 |

3005768 |

3005768 |

9100435 |

Jan |

3088899 |

3005768 |

3005768 |

9100435 |

Feb(Adj.) |

1531521 |

3821273 |

3821273 |

9174067 |

Feb |

1531521 |

3821273 |

3821273 |

9174067 |

Total |

21294425 |

26081897 |

26081897 |

73458219 |

Total |

21294425 |

26081897 |

26081897 |

73458219 |

8.4 Interest Calculation

The fact that, adjustments are being undertaken in GSTR 3Bs, there is every possibility of past overstatement of ITC or understatement of Output Tax Liabilities. Interest is chargeable under Section 50 of the CGST Act, while its rate has been notified as 18% p.a. There are two school of thoughts, while paying calculating Interest;

- Interest to be calculated from the date of due date of month of which tax liability has arisen -> till the date said amount is paid by way of credit of ECaL via Form PMT 06. For e.g. suppose an Outward Tax Liability of INR 10,000 was under-stated in GSTR 3B of Aug, 2017. Such under-statement came to the notice of taxpayer on 25th Dec 2017, and he makes a credit to ECaL on 30th Dec 2017. Therefore as per this school of thought Interest should be paid for 100 Days viz. from 21st Sept 2017 till 30th Dec 2017.

- Another school of thought asks for calculation of Interest from the date of due of month of which tax liability has arisen -> till the correction of such tax liability in the next falling GSTR 3B. Take the above example, suppose the taxpayer files his GSTR 3B for Dec on 15th Jan 2018 after accounting the under-stated tax liability of INR 10,000. Accordingly, Interest calculation should be for 116 Days i.e. from 21st Sept 2017 till 15th Jan 2018, date on which tax liability was declared.

Section 50 (1) is reproduced below to gauge some sort of credibility out of the above schools;

50. (1) Every person who is liable to pay tax in accordance with the provisions of this Act or the rules made thereunder, but fails to pay the tax or any part thereof to the Government within the period prescribed, shall for the period for which the tax or any part thereof remains unpaid, pay, on his own, interest at such rate, not exceeding eighteen per cent., as may be notified by the Government on the recommendations of the Council.

Section 50 (1) clearly doesn’t lay down the dates for which Interest has to be paid, however it defines the Interest Period as “a period during which tax remains unpaid”. A tax remains unpaid, unless it is assessed, either by assessee or by the revenue. Chapter XII of CGST Act, defines variety of assessments, and prescribe how a tax is recovered under each of such assessment. At this juncture, a look at Section 59 is necessary;

59. Every registered person shall self-assess the taxes payable under this Act and furnish a return for each tax period as specified under section 39.

Section 59, embosses the taxpayer with a responsibility of assessment viz. self-assessment. Also it provides the procedure by which the taxpayer has to take care such responsibility which is filing of returns under section 39. Therefore a conjoint reading of Section 59 and 39 makes it clear that a tax is assessed only when a return is filed. Conversely, until and unless a return has been filed, the tax remains un-assessed and hence un-paid. Therefore, Interest Period under Section 50 (1) should last till a return has been filed, making the 2nd view above a rationale one. As for 1st view is concerned, the credit to ECaL can be adjudged as merely a deposit and not tax payment. Unless a tax liability has been crystalized, ECaL balance remains as it is, judgment in case of Jay Shree Tea & Industries Ltd. vs CCE, Kolkata 2005 (190) ELT 0106 (Tri. – Kolkata) can be relied upon;

There is a distinction between the amount appropriate towards duty and amount deposited for payment of a duty. In a former case duty which has only been levied and paid evidently becomes the property of the Government and no person would be entitled to get it back unless there is a provision of law to enable that person to get the duty already appropriated back from the state or the Government. In the latter case, however, when an amount has been deposited to be appropriated thereafter towards duty which may fall due there having no appropriation, the property in money does not pass to the Government unless the goods are cleared and the duty is levied.

8.5 Use of Offline utility for correcting indifferent figures of CGST and SGST

Since February 2018, the online Form GSTR 3B maintains a sync between CGST and SGST at all the places. In fact, Form GSTR 3B permits punching in either one of the field, and the other field auto populates, with the same figures. Said sync was not there before February, therefore it might have happen that taxpayers had reported different figures in CGST and SGST fields.

Such errors can be cured through Offline Utility of furnishing Form GSTR 3B. Put in any figure, in the Excel offline utility and created a .json extension file by validating the same. The .json file can be edited with any text editor and any field can be punched with different figures for CGST and SGST. Once the editing is done, the .json file can be uploaded on the Online Portal, and it will accept the different figures for CGST and SGST.

To sum up, an effort has been made to provide guidance into correction of Form GSTR 3B. It has been a personal experience that the out of ~40% of taxpayers who have not filed GSTR 3B, a large portions have failed to do so out of the above noted errors. It is blessing that Circular 26/2017 offers some much needed statutory backing for the trade to do required adjustments. However, the concerns remains intact, that figures under GSTR 3B are not going to reflect the Financial Statements or the figures to be piled in Income tax declarations, is a worry in itself. Could the return revisions be an option?

Apologies for the Grammar.

Thank You

masachdeva@outlook.com

[1] Mathematics: A same change in Numerator and Denominator will increase the output

GSTR 3B for the month of April 2019 was not filed. kindly provide a solution to rectify the same.

We have wrongly reported Interest in GSTR 3B and filed return for the month of July 2017 (1st return under GST). Since the return was filed, we did not had option to amend, hence interest is also paid by Cash. How do we do corrections and claim refund

Well explained.?

Dear Madm,

AS suggested

1. I downloaded GSTR-1 from GST Portal

2. I uploadeded the zip file deleted from GSTR portal and uploadeded in GST tool

3. I deleted all files in GST tool and uploaded new (amended) file

4. I dowloaded the jason file from GST tool.

5. Comong back to upload the jason file I find that the original file submitted is not deleted in GST Portal.

What should i do?

Regards

Your reply

Dear Manchanda ji,

Hope you are doing well!

Once you have generated the JSON file using offline utility with all the invoices showing “D” as status, then kindly upload it on the portal and approximately after half an hour, all the invoices will be deleted from the portal.

I hope your query is now resolved.

My query again not replied

Dear Sir,

Thanks, but GST portal shows “filled” and the option to choose file does not emerge. When we click on same it asks for generate file and not choose.

Pl help solve the problem

Dear Mr. Manish Sachdeva,

I am amazed at your comprehensive mastery over GST system ! Start-up companies like ours greatly benefit from your expert comments on GST.

I have a small query. At present, our company has registered only one digital signature on GST website for uploading various returns. However, as abundant caution we want to register one more digital signature on the GST website for uploading various returns.

I have two queries in this regard: (1) Is it possible to register second digital signature on GST website to be used on ‘either/or’ basis ? (2) If yes, then how to proceed to register the second digital signature ?

Your kind guidance will be deeply appreciated.