GST – A PRACTICAL BUSINESS TAX Versus PRACTICAL BUSINESS CHALLENGES

“The ones, who are crazy enough to think that they can change the world, are the ones who do.”

― Steve Jobs, Selected Writings

CAUTION

The information contained in this white paper on GST can disturb you by making you realise as to where you are lacking in your zest to accurately and perfectly implement GST in your organisation.

You are requested to read it slowly, carefully and completely so that actual business challenges can be realised and you can come out of the superficial layers floated by some school of thought on GST.

GST- A Practical Business Tax

GST is a tax known throughout the world as practical business tax.

It is not a “tax on income” but “a tax on business” as settled in courts of law in various country having GST regime. Thus, it was coined to be a practical business tax.

GST – Anticipation in Business

Every person connected with tax, finance, procurement, IT, marketing, etc. are busy with either training or understanding as to what exactly GST will bring to them and their business.

GST- A Collective Exercise

First time in the history of any tax implementation various departments will have collective role to play and most prominent will be Finance, Accounts & Indirect Tax.

This will be supplemented by procurement & marketing in co-ordination with IT department.

GST –Perceptions in Trade

GST as understood by people at large has been contained to their company itself. They have focus only on certain factors: Training, Changes, Challenges, Requirement, etc. to suit the era of GST.

GST- A Puzzle Unplugged

At times, people talk about GST impact & analysis. They worry about various how, when, where, but, if, why, etc.

But, we at AMLEGALS found that the focus is only 50% to the effect and in those 50% changes, the anticipations are restricted to the in-house business operations alone.

GST- Demand & Focus

GST demands much wider focus with a special focus on the sensitive and grey areas. Therefore, if these areas are not taken care of or are not even focused at, then we are afraid that it will lead to unforeseen losses and liabilities in coming days.

The first and foremost requirement is to observe, analyze & track your present transactions, contracts and future commitments.

A self-assessment of transaction should be the base and the first acid test before holding hand of any GST advisor.

The GST is a new levy but transactions are old so realize the golden rule that transactions will rule but GST management have to be chalked out to suit your business.

GST- A Management

GST will require a thoughtful management of the following “5 factors”:

a) GST Impact

b) GST Adaptability

c) GST Transactions

d) GST Risk

e) GST Reviews

Out of these “5 factors”, wherever GST is in operation around the world, only “a” to “c” was focused and it brought reward of litigation finally.

We always insist and advice on a balanced approach and GST Risk & GST Review Management will play a significant role in coming days even in business.

GST- Risk Management versus Business Risk

Businesses have to be streamlined and new commercial mantras will dominate in market to change the equilibrium in every sector.

The businesses have to be reviewed from 360° angle to identify the following:

a. Inter state

b. Intra state

c. Interdependencies between various functions

These “3 i factors” will be very critical.

GST – Technology in Time

The best technology has to be adopted in shortest possible time.

A holistic approach should be adopted to choose the best option in technology. The GST platforms have already been made by various technology players.

To ease the burden of cost of IT implementation at the end of organisations, the Government of India has validated certain GST Suvidha Providers (GSP) so that India becomes ready for GST with the comfort of economy as well. It is quite economical and comes with various options with advisors on their panel as well.

GST- Dual Implementation

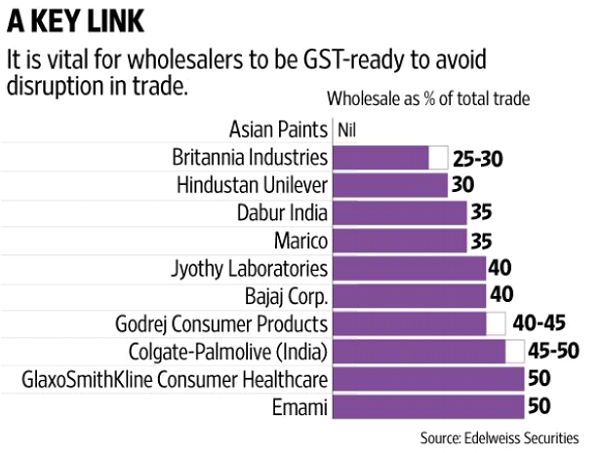

The companies have to identify their ratio of wholesale to retail operations so that a dual model is adopted to implement GST without any hurdles.

The companies have got to think for implementation of GST at their vendor‟s and channel partners at the earliest possible so that seamless GST can be really implemented.

The chain of ITC is dependent between the supplier and receiver. Hence, no chain can be left unattended.

The dual adaptability of GST is actually seamless GST implementation.

GST- Burdening Terminologies

We have come across clients, from entire country, with common viral fever traits especially in the persons dealing in indirect tax to the effect that they are burdened with following heavy terminologies:

a) Transition & Mapping

b) Impact Analysis

c) Implementation

d) Core Team Formation

e) ITC Matching

Trust, GST is not a monster that

people make hues and cry about. It is at par with what is prevailing in excise, vat, etc. but it has been blended with certain changes and the only requirement is REALISATION & PRECAUTION, otherwise it will be a monster of litigations.

GST- Locking & Unlocking

The moot question of GST and its implication during and after transition can be unlocked after realising certain basic aspects that there is no need to panic at all.

There are certain sectors say pharmaceutical, where the stockists of medicines and CFA are looking to decrease their stock under the guise that how the stock will be tallied and Input Tax Credit (ITC) will be available during transition phase.

People are burying their face below data in one or other sheet under the guise of mapping whereas, the simple logic to GST is to check two phases as below:

Pre GST Phase – 4 T

Nature of Transaction

Reason of such Transaction

Manner of Transaction

Document for such Transaction

Post GST Phase- 4 T

Nature of Transaction

Reason of such Transaction

Manner of Transaction

Document for such Transaction

“Find Out differences in all 4 T under both the phases, if there is difference in any of the 4T, then work upon that specific T. The reason is that today also all goods are sent, stored, warehoused, accounted for and/or delivered under documents only.

GST- Transition is Inventory Management

“In post GST also, the document will be there , only nature of tax and place of levy has changed. It is not that the document will be done for the first time.

AMLEGALS strongly advises that don‟t panic but simply focus on better inventory management and devise an internal system at every business centre to team up to linkup the stored goods with document and GRN no‟s or any other assigned numbers. This will ease up the phase of transition.

The inventory management is a collective effort of stores, marketing, logistics, excise, procurement and finance/account department.

It is a matter of realisation that today also one has to show and establish the duty paid nature of goods which are sent from factory to warehouse for stocking and its subsequent clearance under commercial invoice. The duty paid nature of goods is established by linkage of stock under commercial invoice with excise invoice.

“This linkage formula already exists but for claiming ITC during transition , more cautious approach has to be adopted. Further, the inventory management has to be elevated to the next level of linkage with duty paid nature of such goods. There is no need to panic under the guise of mapping for transition.

GST – Documentation via Transition

The transactions which existed in pre GST era will also exist in post GST era but with slight variation only. However, the factor which shall be very crucial will be documentation.

The transactions need to be documented to have smooth transition to GST era. The entire loop of GST rests upon documentation and so any failure in its sequence will break the link with creation of confusion and ambiguity in the team work.

GST – A Conclusion & Realisation

The challenge is not only to implement GST but to prevent the miscarriage of GST.

GST is a loop which cannot be read, understood, analysed, perceived, and implemented with superficial approach but with a vision of start to end alone.

GST will rule the business and one who could factor the GST at right time and right place will result an x factor in competition of business.

GST requires a dual approach and it cannot be decided merely on the basis of some data but actually it mandate the requirement of understanding the heart and soul of business.

AMLEGALS always emphasise that it‟s your business so understand it in real sense and then team up with a GST advisor in such a manner that the heart and soul of a business comes first before acting upon the advice on GST implementation.

Wish you all a successful GST era!

About Author

Mr. Anandaday Misshra is a practicing Advocate specializing in Litigation & Advisory for almost last 2 decades at High Court of Gujarat, other High Courts of India, Appellate & Arbitral Tribunals, Civil Courts, etc.

He is an expert of the law domain focusing majorly on Indirect Taxes (GST), Arbitration, Commercial, Company & Corporate Laws and IPR.

The author can be reached at anand@amlegals.com

Disclaimer: The information contained in this document is intended for informational purposes only and does not constitute legal opinion, advice or any advertisement. This document is not intended to address the circumstances of any particular individual or corporate body. Readers should not act on the information provided herein without appropriate professional advice after a thorough examination of the facts and circumstances of a particular situation. There can be no assurance that the judicial/quasi-judicial authorities may not take a position contrary to the views mentioned herein.

Download Article in PDF Format