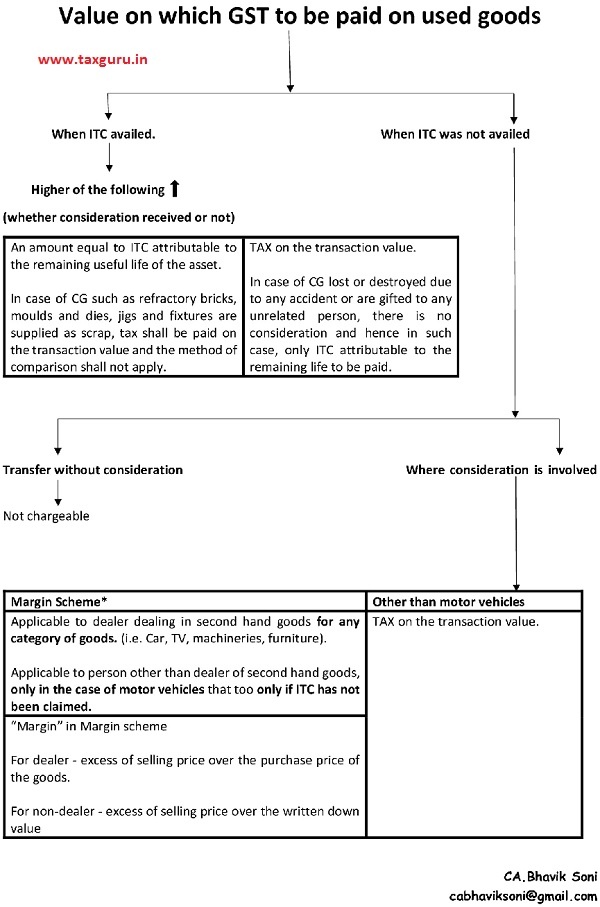

The implications of tax on sale of used assets is one of the most complex things faced by an assessee. However, under GST, Government has tried to simplify the said issue by removing multiple and complex restrictions on cenvat credit availability on sale or disposal of used assets and introduced more liberal provisions as compared to previous regime.

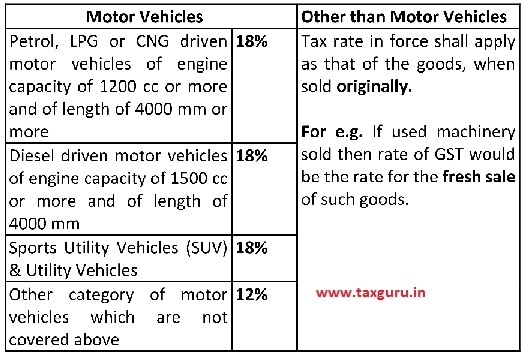

Supply goods under GST can be of Fresh Goods and Used (Second Hand) Goods. For the purpose of taxability under GST and ease of understanding, Second Hand Goods are further bifurcated as follows: Motor Vehicle and Other than Motor Vehicle. Motor Vehicles include car, trucks, vehicles used to transportation of goods and other passenger vehicles.

To more simplified the said provisions, we summarised all situations in a tabular mode.

*The margin scheme was implemented for a dealer dealing in second hand goods who does not claim ITC on the goods purchased and who sells the goods as such or after minor processing which does not change the nature of the goods. Vide Ntfn No. 8/2018-Central tax (Rate), dated 25/01/2018, the margin scheme was made applicable to all taxpayers on the sale of motor vehicle held as capital asset. It is pertinent to note that the margin scheme is applicable for a dealer other than a person dealing in second hand goods, only in the case of motor vehicles, that too only if input tax credit has not been claimed.

GST rate on Used Goods

Value on which GST to be paid is depend on the various situation as mentioned in chart. And yes, GST if applicable, should be mentioned in invoice.

Should the invoice mention GST amount and should it be on sale value?