Chanakya’s words summarize the whole GST process – ‘even if something is very difficult to be achieved, one can obtain it with penance and hard work’. If we take into consideration the 29 states, the 7 Union Territories, the 7 taxes of the Centre and the 8 taxes of the states, and several different taxes for different commodities, the number of taxes sum up to a figure of 500! Today all those taxes will be shared off to have ONE NATION, ONE TAX right from Ganganagar to Itanagar and from Leh to Lakshadweep.

– Narendra Modi, Prime Minister of India,

Dedicating GST to the nation – 1st July 2017; Central Hall, Parliament of India

A Story of Extraordinary National Ambition

When in the history of global economy did a project unfold that involved a constitutional amendment which took 6 years of discussion but got passed by the Union Parliament and got ratified by 16 States, all in a period of just two months? Where else were 5 laws (Central Goods and Services Tax Act, State Goods and Services Tax Acts, Integrated Goods and Services Tax Act, Union Territory Goods and Services Tax and the Goods and Services Tax (Compensation to the States) Act) made in 16 languages with the approval of the federal Parliament and 31 state legislatures involving 200 pieces of delegated legislations? When was the last time that a mandate evolved from 18 meetings over a period of 10 months chaired by the Union Finance Minister involving the participation of Ministers representing the Finance Ministries of all States after prolonged negotiations and compromises? How often do political parties from across the ideological spectrum come together to support the will espoused by the current dispensation? When did we last hear of more than 500 officers of the Union and State administrations working behind the veil of the political mandate to ideate, conceptualise, draft and present the superior and subordinate legislations? Can you imagine of 200,000 officers from across the length and breadth of a nation as culturally diverse as India coming together to implement in a uniform manner a tax reform that will fundamentally alter the way every business functions? Which other country has envisaged and realized such a momentous transformation that directly and indirectly impacts more than One billion people?

This is a story of extraordinary national ambition – unparalleled in the history of global economy – the story of the Goods and Services Tax (GST).

The Goods and Services Tax

GST is a consumption tax based on the credit-invoice method where only the value addition at each stage is taxed, with seamless flow of credit along the supply chain. It subsumed in its ambit a large number of consumption taxes that previously existed in India, administered separately by the Centre and the States, resulting in a greatly rationalized taxation structure.

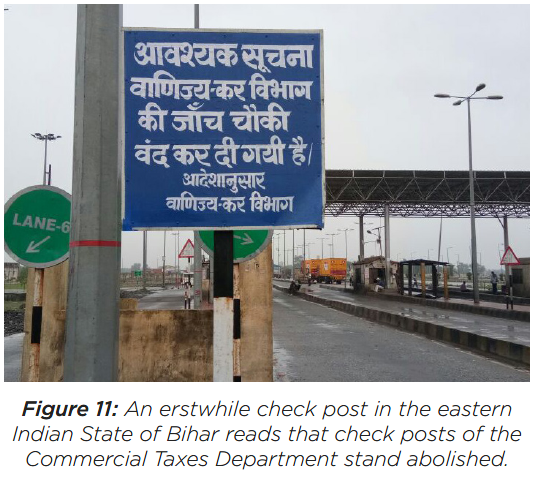

The umbrella system of GST inter alia integrated the tax administrations of the Federal and State Governments, making it a single interface for the taxpayers, creating an IT backbone that would match the details of inward & outward supplies at the level of line items, eliminating the cascading effect of taxes thereby making the country’s exports more competitive in the global market and finally removing once and for all the age-old system of check posts for inter-State movement of goods. Besides altering the industrial landscape of the country, GST is also a never-heard-before experiment in fiscal federalism. Cutting across ideologies, politicians, policy makers and tax administrators negotiated, bargained and arrived at decisions – all in the interest of greater common good. The legislations that made up GST were put in public domain for feedback multiple times at each stage, empowering all the stakeholders to deliberate on what kind of future they wanted to help design, in the truest spirit of democracy.

Primarily, GST is a tax levied on the supply of goods and services. In case of an inter-state supply, it is called integrated tax, levied by the Federal Government, administered jointly by the Centre and the States and later apportioned between them. In the case of an intra-state supply, it is levied in two components – the federal tax, levied by the Federal Government and the state tax/union territory tax, levied by the respective administrations.

Genesis of GST

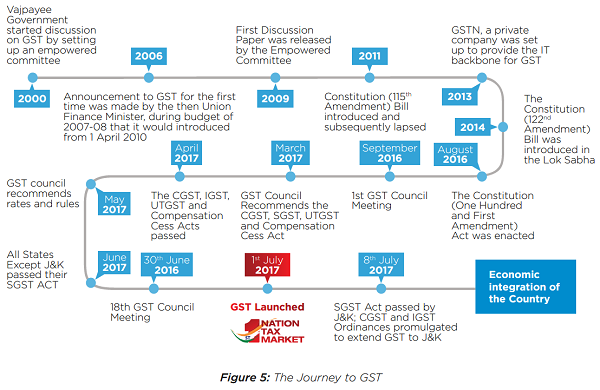

The Kelkar Task Force on the Fiscal Responsibility and Budget Management (FRBM) Act, 2003 suggested a comprehensive GST based on the Value Added Tax principle. The proposal to introduce a National-level GST was first mooted in the Budget Speech in the year 2006. The responsibility of preparing a Design and Road Map for the implementation of GST was assigned to the Empowered Committee of State Finance Ministers (EC). Based on inputs from the Government of India and the States, the EC released its First Discussion Paper on Goods and Services Tax in November 2009. The Constitution (115th Amendment) Bill was introduced in the Lok Sabha in March 2011. However, the issue of payment of compensation to the States for loss of revenue remained an important bone of contention between the Centre and the States, and in the face of resistance in the Parliament, the Constitution (115th Amendment) Bill was referred to the Standing Committee on Finance for examination. Deliberations between the Centre and the States on the Constitutional Amendment Bill continued in the Empowered Committee till the dissolution of the 15th Lok Sabha in May 2014, however no consensus could be formed around the contentious issues of compensation, treatment of petroleum products and subsuming of entry tax. The amendment bill lapsed with the dissolution of the 15th Lok Sabha.

In June 2014, the draft Constitution Amendment Bill was sent to the Empowered Committee after approval of the new Government. Trust deficit plagued all dialogues between the Centre and the States on GST. States had apprehensions about surrendering their taxation jurisdiction, treatment of petroleum products, subsuming of taxes such as entry tax and purchase tax and getting adequate compensation for any loss of revenue for five years. The Union Finance Minister met with the Chairman of the Empowered Committee and Finance Ministers of States on 3rd July 2014 and 11th December 2014. He further met the Chairman of the Empowered Committee and Finance Ministers of Gujarat, Haryana, Punjab, Tamil Nadu and Karnataka on 15th December 2014. All the pending contentious matters were resolved in these two meetings, wherein it was decided that a provision would be inserted in the Constitution Amendment Bill itself for payment of compensation to the States for the first five years post implementation of GST and that the GST Council would recommend the date on which GST would be made applicable on petroleum products. In terms of this broad consensus, the Government sought the approval of the Cabinet to introduce the revised Constitution (122nd Amendment) Bill in the Parliament. The Constitution (122nd Amendment) Bill, 2014, was thus introduced in the Lok Sabha on 19th December 2014.

In the meanwhile, to bridge the trust deficit, the Union Finance Minister also obtained the approval of the Cabinet for paying compensation to the States for loss of revenue caused to them on account of reduction in the rate of CST from 4% to 2%, for the years 2010-11, 2011-12 and 2012-13, over a three-year period beginning 2014-15. This had been a long-standing demand of the States and non-payment of this compensation amount in the past years had adversely affected the deliberations between the Centre and the States.

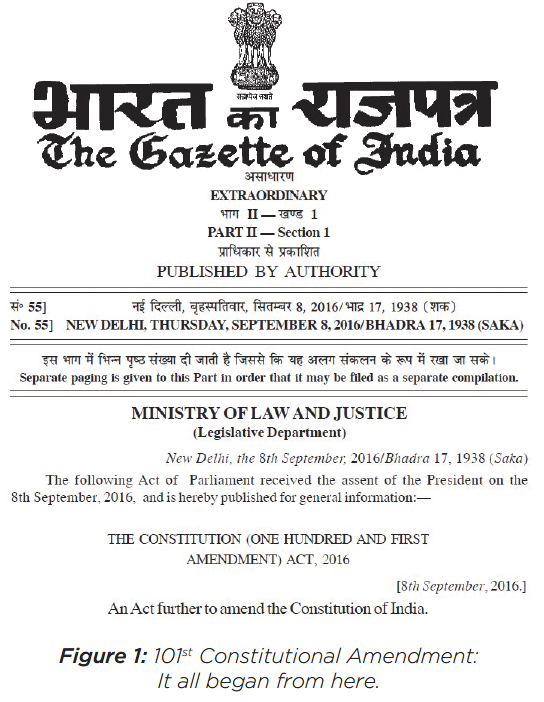

The Constitution (122nd Amendment) Bill was passed by the Lok Sabha on 6th May 2015, and was sent to Rajya Sabha for consideration. In Rajya Sabha, the Bill was sent to a Select Committee for examination on 12th May 2015. The Select Committee submitted its report on 22nd July 2015. Thereafter, the Bill was passed by both Houses of the Parliament on 8th August 2016. After ratification by 50% of the States, the Constitution (101st Amendment) Act, 2016 was assented to by the President on 8th September 2016. After the passing of this first and biggest hurdle, the process for bringing this historic reform acquired significant momentum.

The GST Council – Beginning of a new journey

The fifteenth day of September in 2016 saw a new chapter in the history of India’s Centre-State relations, with the formation of the GST Council, courtesy the Constitution (101st) Amendment Act, 2016. The Council was formed after close to one and a half decades of deliberation. The Council, represented by all the 29 States and 2 Union Territories with legislature, is the first Centre-State body vested with full decision-making powers and whose control over the fiscal health of the country is immediate. Decisions in the Council are taken by a majority of not less than three-fourths of the members present and voting. The Centre has a weightage of one-third of the total votes cast, while the States, taken together, have a weightage of two-thirds of the total votes cast, thus ensuring that every decision of the Council has to happen with the consent of both the Centre and the States. However, the unique feature of the GST roll-out is that the Union Finance Minister as Chairperson, GST Council, ensured that no decision was put to vote and instead, every decision of the Council was arrived at by consensus. Even contentious decisions were subject to discussions, however lengthy, but eventually, everyone was taken on board, in the true spirit of cooperative federalism. Every meeting of the Council is an exercise in federal policy-making. In the 10 months that the Council has been in existence, there have been 18 meetings, averaging a remarkable 2 meetings per month! The meetings have not been restricted to New Delhi alone and have also been held at locations like Udaipur, Rajasthan and Srinagar, Jammu & Kashmir, thereby symbolizing how the States too are equal partners in this journey.

Peculiarity of the Indian GST Model

The Indian model of GST is unique in the sense that it is one of few countries in the world that have implemented a dual structure (other examples being Canada and Brazil), thereby ensuring that both the Centre and the States have an equal stake in the case of intra-State supplies of goods or services. Another notable aspect about the Indian GST model is the invoice-matching system that has been implemented. An estimated three billion invoices are expected to be matched on a monthly basis to ensure seamless flow of credit among the taxpayers.

Another standout feature of GST is that the Government was more proactive and receptive to change than the industry. Be it the number of times the laws and rules were put out in the public domain, the plethora of stakeholder consultations that the bureaucrats had with members of various sectors, or the press releases and updates via various social media outlets, often quashing unsubstantiated and mischievous rumours, the Government has indeed set a new template for proactiveness and reform. These distinguishing factors indeed make the Indian GST model unique compared to the rest of the world.

Making of the law

The making of the GST law was indeed a mammoth exercise and over a period of one year, around 40 officers worked very closely under the leadership of a team of 10 senior officers to make this law a reality. A law committee was constituted for the same in 2009 to work on the Constitutional Amendment and to prepare a discussion paper on GST. The Empowered Committee had been working on the design of GST for almost a decade and the first committee then had three sub-committees which started working on Revenue Neutral Rate (RNR), threshold, dual control, exemptions, taxation of inter-state supplies and determination of place of supply. In 2012, an IT (Information Technology) Committee was also constituted.

The IGST model adopted was one out of twelve models examined in detail by the Centre and the States. Between 2003 and 2006, much deliberation on taxation of services and vesting of powers to the States to collect tax on services had taken place. This actually led to the 72nd Constitutional Amendment vide which entry 92C (Taxes on services) of the Seventh Schedule of the Constitution of India was inserted. Work slowed down from 2011 to 2014. In 2014, it gained momentum.

The drafting of the law began in 2014. Three sub-committees were again constituted to work on different aspects of law, i.e., rates, exemption, supply, registration, dispute resolution, IGST, ITC (Input Tax Credit), settlement etc., and designing of detailed business processes including those of registration, return, refund, payment and IGST settlement. By September 2016 the sub-committees gave a report on major areas including forms and returns.

Finally, on completion of the final rounds of vetting by the Department of Legal Affairs and the Legislative Department of the Union Ministry of Law, the GST laws – CGST, SGST, IGST, UTGST and Compensation were passed by the respective legislatures of the Centre and States between April to July 2017.

| S.No. | Name of the State | Date on which SGST Act passed in the Assembly | S.No. | Name of the State | Date on which SGST Act passed in the Assembly |

| 1. | Telangana | 9th April 2017 | 17. | Maharashtra | 22nd May, 2017 |

| 2. | Bihar | 24th April, 2017 | 18. | Tripura | 25th May, 2017 |

| 3. | Rajasthan | 26th April 2017 | 19. | Sikkim | 25th May, 2017 |

| 4. | Jharkhand | 27th April, 2017 | 20. | Mizoram | 25th May, 2017 |

| 5. | Chhattisgarh | 28th April, 2017 | 21. | Nagaland | 27th May, 2017 |

| 6. | Uttarakhand | 2nd May, 2017 | 22. | Himachal Pradesh | 27th May, 2017 |

| 7. | Madhya Pradesh | 3rd May, 2017 | 23. | Delhi | 31st May, 2017 |

| 8. | Haryana | 4th May, 2017 | 24. | Manipur | 5th June, 2017 |

| 9. | Goa | 9th May, 2017 | 25. | Meghalaya | 12th June, 2017 |

| 10. | Gujarat | 9th May, 2017 | 26. | Karnataka | 15th June, 2017 |

| 11. | Assam | 11th May, 2017 | 27. | West Bengal | 15th June, 2017 |

| 12. | Arunachal Pradesh | 12th May, 2017 | 28. | Punjab | 19th June, 2017 |

| 13. | Andhra Pradesh | 16th May, 2017 | 29. | Tamil Nadu | 19th June, 2017 |

| 14. | Uttar Pradesh | 16th May, 2017 | 30. | Kerala | 21st June, 2017 |

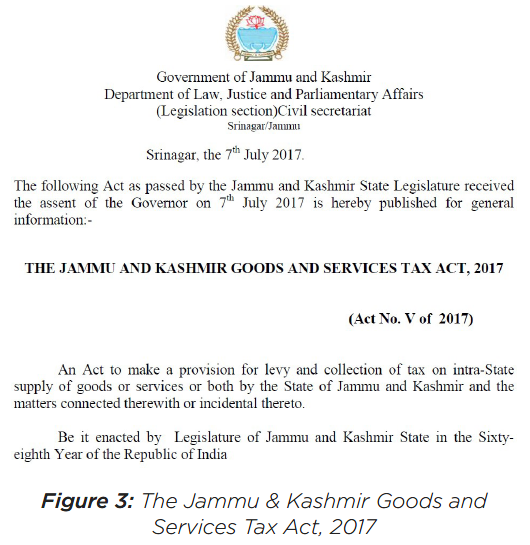

| 15. | Puducherry | 17th May, 2017 | 31. | Jammu & Kashmir | 7th July 2017 |

| 16. | Odisha | 19th May, 2017 |

Table 1: Dates on which the SGST laws were enacted by the states

Treading Together with Trade: Committees & Sectoral Groups

To ensure that the trade and industry are given adequate opportunities to represent their cases and offer their feedback, eighteen sectoral groups were formed, consisting of senior officials from both the Federal and State Governments. The eighteen sectors are as below:

| 1 | Banking, Financial & Insurance | 10 | Government Services |

| 2 | Telecom | 11 | Food Processing |

| 3 | Exports | 12 | E-Commerce |

| 4 | IT / ITES | 13 | Big Infrastructure |

| 5 | Transport & Logistics | 14 | Travel & Tourism |

| 6 | Textiles & Footwear | 15 | Handicrafts |

| 7 | MSMEs | 16 | Media & Entertainment |

| 8 | Oil & Gas | 17 | Drugs & Pharmaceuticals |

| 9 | Gems & Jewellery | 18 | Mining |

Table 2: List of Sectoral Groups constituted to look into Industry representations

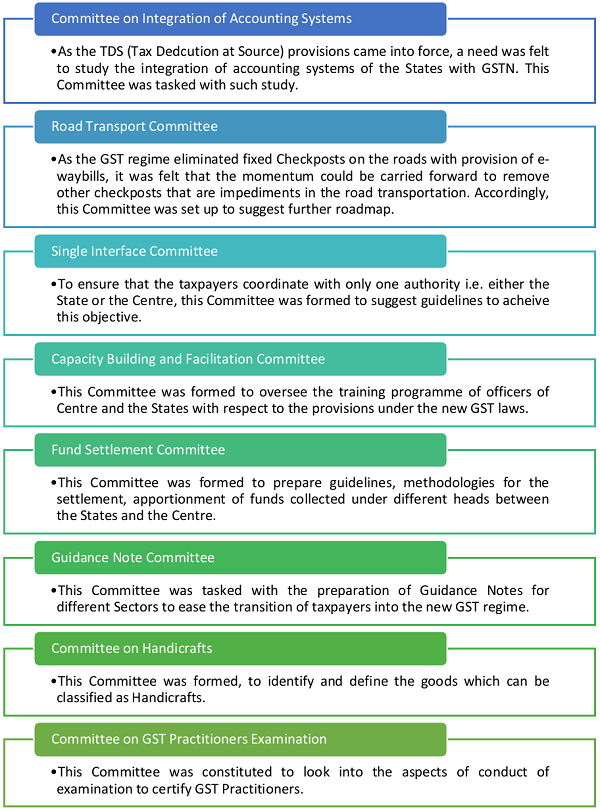

In addition, to look at various aspects of the rollout – eight standing committees were formed as shown below:

| 1 | Law Committee | 5 | Publicity and Outreach Committee |

| 2 | Information Technology Committee |

6 | Capacity Building and Facilitation Committee |

| 3 | Single Interface Committee | 7 | Fund Settlement Committee |

| 4 | Fitment Committee | 8 | Guidance Notes Committee |

Table 3: List of Standing Committees constituted for GST Rollout

Figure 4: Image Courtesy: The Economic Times, India

Journey to GST

GST could not have come at a more opportune time for India. The nation is at that critical stage of its evolution where we are poised to take off to the next level of socio-economic development and need that catalytic jump that will propel us there. What makes the implementation of GST from 2017 particularly noteworthy is how it sits at the culmination of a plethora of local and global developments, much of it deliberately and strategically planned. Among the notable policy moves taken by the Government is the Jan Dhan Yojana, a national mission of financial inclusion to ensure access to financial services namely Banking, Savings & Deposit Accounts, Remittance, Credit, Insurance, and Pension in an affordable manner. It is by now well-known that one of the intended benefits of GST is the formalisation of a major chunk of the informal economy, thanks to the requirement for a registered recipient of supply to pay GST under reverse charge, if the supplier is not registered, thus greatly disincentivizing evasion of taxes. This transition from an informal channel to a formal setup would have caused much hardship to the large number of people employed. However, with the opening of a staggering 300 million accounts courtesy the Jan Dhan Yojana, this transition has been eased to a large extent. GST has also made payment through electronic means mandatory, taking forward the Government’s campaign for cashless payment, which is an integral part of the Digital India program.

The Government of India has made linking of PAN (Permanent Account Number – a unique identity for payment of direct taxes) with Aadhaar (a unique identification number issued by the Indian government to every individual resident of India) mandatory. The GSTIN (a unique identification number issued by the GST Network for taxpayers under the GST Law) is also linked to the PAN and the PAN is mandatory for any import or export activity. Thereby, GST, for the first time, brings about a direct handshake between the direct and indirect taxes (including Customs Duty).

GST and Direct Taxes in India – A Perspective

Under GST, the cascading effect of Federal and State level taxes will be considerably reduced. Consequently, as newsupplies flow into the market, there would be reduction in embedded taxes on inputs resulting in cost savings on intermediate inputs. This should reflect in higher profits and higher direct tax revenues. GST is a paradigm shift from physical control to account-based control at transactional levels. Most taxpayers would now be required to file comprehensive monthly returns of their supplies and purchases of intermediate goods and services. The cumulative effect would be to restrict the scope for year-end manipulation of sales and purchases. To this extent, there should be a positive impact on profit disclosures. Exchange of data between the GST administration and the Direct Tax Administration would also enable the Direct Tax Administration to undertake real-time verification for better monitoring of tax collection. As is well known, GST is a destination based consumption tax; the income tax is also designed as a consumption-based direct tax. The introduction of GST is also expected to trigger a shift from the unorganized sector to the organized sector. This shift should benefit direct tax collection too. GST is expected to provide an impetus to economic growth. Higher economic growth should translate to higher direct tax revenues. Internationally, introduction of GST has indeed resulted in higher direct tax collections.

What other taxes are impacted by GST and in what manner?

The acronym good and simple tax for GST stands its worth when one looks at the number of different taxes and cesses which got subsumed into it. Seven federal and eight state taxes saw their dusk with the dawn of GST. While these subsumed taxes got a lot of coverage and attention, the great number of surcharges and cesses which have been abolished escaped the eye. In addition to the indirect taxes, GST will have an impact on the enforcement of the Black Money Act, Benami Transactions (Prohibitions) Act and several other laws.

| Federal Taxes | State Taxes |

| Central Excise Duty | State VAT |

| Duties of Excise (Medicinal and Toilet Preparations) |

Central Sales Tax Purchase Tax |

| Additional Duties of Excise (Goods of Special Importance) | Entry Tax Luxury Tax |

| Additional Duties of Excise (Textiles and Textile Products) | Entertainment Tax (except those levied by the local bodies) |

| Additional Duties of Customs (CVD) | Taxes on lotteries, betting and gambling |

| Special Additional Duty of Customs (SAD) | Taxes on advertisements |

| Service Tax |

Table 4: Federal and State Taxes subsumed in GST

| Federal Taxes | State Taxes |

| Central Excise Duty on tobacco & tobacco products and petroleum products (petroleum crude, high speed diesel, motor spirit, natural gas and aviation turbine fuel) | 1. CST on petroleum products (petroleum crude, high speed diesel, motor spirit, natural gas and aviation turbine fuel)

2.State Excise Duty and VAT on potable alcohol 3. Entertainment Tax to be levied only for the benefit of local bodies 4.Duty on sale of electricity 5. Taxes on vehicles |

Table 5: Federal and State Taxes not subsumed in GST

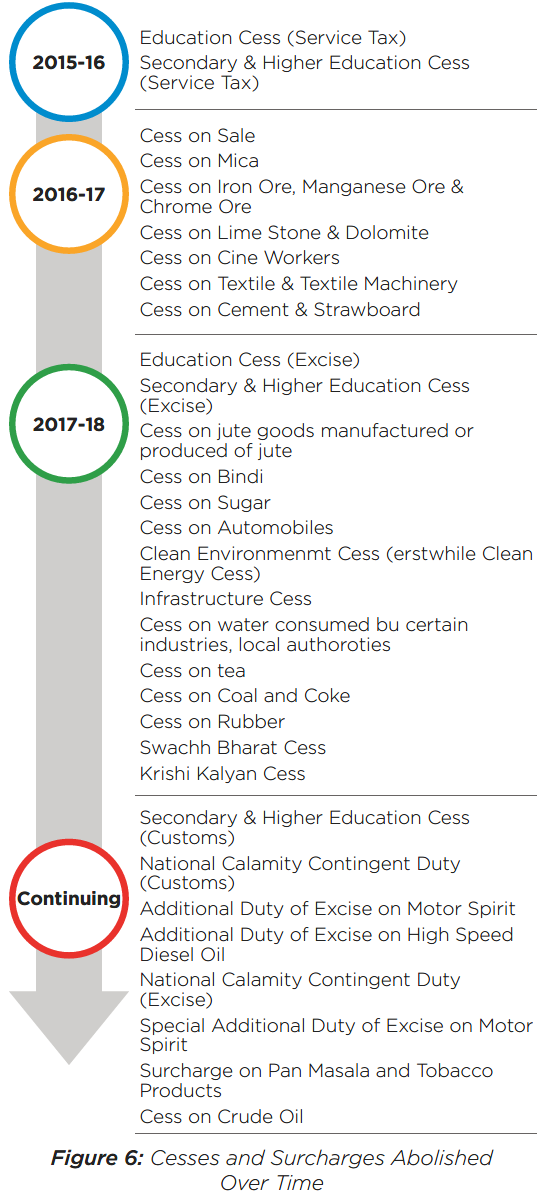

The process of simplifying tax structure by abolishing the cesses has been an ongoing process which gained maximum impetus in the run-up to GST. While education cess and secondary and higher education cess for services had been abolished on the year 2015, for goods these were exempted and the abolition happened in the taxation amendment act, 2017. Similarly, cess on cement and strawboard were exempted in 2016 and abolished in 2017, along with six other cesses. Fourteen cesses were abolished through The Taxation Laws (Amendment) Act, 2017.

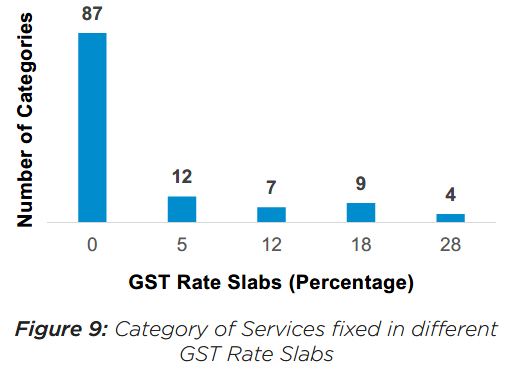

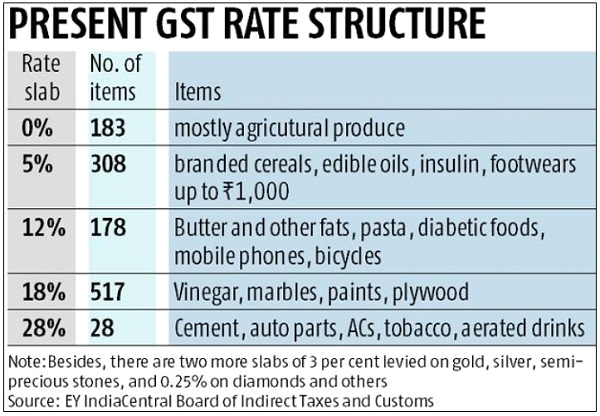

Story of the rates – Fitment Committee

The rates of 1,211 commodities and 119 categories of services were decided in a two-day meeting in the beautiful valley of Kashmir, lending further impetus to the roll out of GST. This humongous task of fitting the commodities and services into appropriate rate slabs, when accomplished in two days (backed by long periods of dedicated hard work and research based on the existing incidence and industry health) was a breakthrough indeed. The rates and the exemptions were to be notified in coordination with all the States so as to ensure that if someone referred to a notification number, it talked about the same issue across the country. Multiple drafts were worked on, feedback from all over incorporated as appropriate, previous notifications modified, rescinded or amended and on 28th June 2016, two days before the implementation, all the information was put in public domain in the legal lingua-franca..

Though seven rates were fixed for goods and five rates for services, it was indeed a great update from the mesh of rates and exemptions which Indian indirect tax structure was earlier.

* In addition, a special rate of 3% was fixed for gold & other ornaments and a rate of 0.25% was fixed for rough diamonds

Zero rating concept

One of the most important advantages of GST is that it removes cascading on taxes. This is most material in case of exports. Earlier, embedded taxes at various levels of the value chain made our exports costlier and thus uncompetitive in the international market. Even if refund of taxes paid on exports at the last or penultimate stage was available, there remained some amount of cascading of taxes. To correct this distortion, the concept of zero rating has been adopted in GST. All goods and services forming a part of the final value of the end-product/service are exempt from taxes by way of refund to the suppliers or by the mode of supply on bond/letter of undertaking. Thus, not only is there no embedded tax for the exporter, but also, there is no blockage of capital for the exporters and their suppliers, thereby incentivizing exports.

Goods and Services Tax Network – the IT Platform

India aimed at achieving with GST, not merely a simplification of the tax structure, but also a systemic reform with transparency, efficiency and speed in implementation and administration of taxes. Technology was undoubtedly a major component of the solution devised to fulfil these objectives. Besides, GST being a destination based tax, inter-State Trade of goods and services (IGST) would need a robust settlement mechanism amongst the States and the Centre. This could have been possible only when there was a strong IT Infrastructure and Service backbone which enabled capture, processing and exchange of information amongst the stakeholders (including tax payers, Federal and States Governments, Accounting Offices, Banks and RBI). Additionally, in view of the sensitivity of the information that would be available with the agency which will put in place the IT Infrastructure, the Government needed to have strategic control over the agency. Thus was born the Goods and Services Tax Network (GSTN), a Special Purpose Vehicle, created by the Government of India and State Governments as a non-government, not-for-profit Company, which brings flexibility of the private sector with strategic control of the Government. The GSTN System Project is a unique and complex IT initiative – unique as it seeks, for the first time to establish a uniform interface for the tax payer and a common and shared IT infrastructure between the Centre and States; and complex in that it works towards integrating the 36 varied and disparate systems of the Centre and the States, at different levels of maturity.

The Himalayan magnitude of the GST process

- 8 Million registered business entities in GSTN

- 3 Billion invoices matched every month

- 200,000 tax officials involved in administering GST

- 6,000 outreach programs for taking GST to the trade and industry

The GST Common Portal developed by GSTN functions as the front-end of the overall GST IT eco-system where taxpayers register, prepare documents for payment through banks and will file returns. The IT systems of the Federal Government – Central Board of Excise & Customs (CBEC) and State Tax Departments function as backends that handle tax administration functions such as registration approval, assessment, audit, adjudication, etc. CBEC and nine States are developing their backend systems themselves whereas GSTN is developing the backend for the remaining 20 States and 7 Union Territories.

| Parameter | Description | Value |

| Number of taxpayers | Total number of taxpayers the system can handle without needing any additional hardware or change in architecture | 13 Million |

| Concurrency | Total number of user requests the system can process at the same time | 60,000 |

| No. of Sessions | Total number of users who are logged in with active sessions the System can handle before taxpayers are required to wait to enter the system (waiting lounge) | 150,000 |

| Data Storage | A measure of total number of data elements (invoices, returns, ledgers, logs, audit trail etc.) | 200 Terra Bytes for the first year |

Table 6: Parameters used for design of GST Systems

Architecture Principle

Owing to the enormity in scale and magnitude, the GSTN system has adopted a distributed and asynchronous design based on open source technologies in the big data space, in order to separate the submission and processing of data. This provides massive scaling capabilities to the GSTN system coupled with inherent security cover. The distributed architecture ensures that all data elements are separated and require software code to integrate, to provide meaning to the data being extracted. The multi-layered architecture comprises of a static dumb layer that interacts with taxpayer traffic, a stateless business logic layer, stateless processing layer and data storage layer. Every traffic is controlled using secure mechanisms before it gets passed on to the next layer.

How the GSTN system works

GSTN rolled out the registration module on 8th November 2016 to onboard taxpayers registered under Value Added Tax (VAT), Central Sales Tax (CST), Service Tax, Central Excise and other taxes to be subsumed in GST. By 20th July 2017, more than 6 million taxpayers from the old regime have been brought on to the new platform and more than 800,000 new taxpayers have sought registration.

Payment of taxes has also started from 1st July 2017 where one Challan is used for payment of all types of taxes through net-banking facility or over the counter facility of 25 authorized banks. One of the important indicators used in assessing ‘ease of doing business’ by World Bank is the ease of paying taxes. Designed as a self-service mode, which is simple and adaptable for mobile systems as well, the payment interface and multiple options to pay the tax will play a major role in this regard. Checking of claim of Input Tax Credit (ITC) is one of the fundamental pillars of GST, for which data of Business to Business (B2B) invoices have to be uploaded and matched. The invoice level data can be directly entered on the portal by the taxpayer. The system has been designed to handle upload of data of 3 to 4 billion business-to-business (B2B) invoices on this platform. This can be further expanded by adding more servers as the design is highly scalable.

Upload of B2B invoice data can be done on the portal or using the free offline tool developed by GSTN or through GST Suvidha Providers (GSPs) empanelled by GSTN. The platform design of the GST System enables upload of invoice data using Application Programming Interfaces (APIs) released to GSPs who also provide accounting, inventory and reconciliation services etc. based on industry specific requirements. The GST Common Portal will help buyers and sellers match their invoices for smooth flow of input tax credit to the buyer. A similar exercise will be done for inter-state supplies where goods or services will move from the state of origin to the state of consumption and so will the taxes. The claim of IGST and its utilization will be settled based on returns filed at the GST Common Portal. GSTN will create and maintain the information on IGST based on returns of taxpayers. This data will be used for settlement of funds between Centre and States.

Infrastructure

To achieve the aforementioned functionality and provide disaster recovery capabilities with zero data loss feature, the GST system has incorporated hardware across 4 data centres (Data Centre [DC], Near DC [NDC], Data Recovery [DR] and Near DR [NDR]) in two different geographies. The production system serving GST to taxpayers and officers, is mirrored across the data centres with same hardware in order to provide functionally active-active facility. This ensures the load distribution of taxpayer traffic is distributed equally between the two centres.

Ushering in a common market

The GST Common Portal will be the single interface for all taxpayers from any part of the country. Only in cases where a taxpayer is picked up for scrutiny or audit, will the taxpayer be required to interface with the respective tax authority. For all other cases (which is expected to be around 95-97%), the GST Common Portal will be the only interface for the taxpayer. The way it has been conceived and devised, the GST Common Portal truly promises to makes India a single, large market that promises to bring a multitude of benefits for the economy.

As on 22nd July 2017, more than 7 million taxpayers have registered or migrated to the GSTN Portal.

Project SAKSHAM

The Cabinet Committee on Economic Affairs (CCEA) approved Project Saksham – to strengthen the backend IT infrastructure of the Federal Government – in September 2016 at a cost of $ 375 Million over a period of 7 years. The procurement was done through an open tender process on the central e-procurement portal.

SAKSHAM, meaning ‘capable’ in Sanskrit, has provided the much-needed augmentation of CBEC’s infrastructure for GST readiness, including the significant customs module. The delivery, installation and commissioning of equipment at the data centres and all major locations was completed in record time to enable implementation of GST. The hardware deliveries commenced in the 3rd week of December 2016 and the data centre readiness was completed for the primary and disaster recovery centres by March 2017.

The systems went live on 25th June 2017. The GSTN and CBEC systems have been exchanging electronic messages through APIs regularly since then. More than 200,000 registrants’ data has been received and processed by CBEC since 1st July 2017. The project includes equal capacity infrastructure at data centres in Delhi & Chennai, 24*7 IT maintenance & support services, two 24*7 Helpdesks – GST MITRA & SAKSHAM SEVA, a complete Disaster Recovery solution, a data replication solution that ensures no loss of critical data and a 24*7 Security Operations Centre (SOC). It also includes upgrade of Local Area Network (LAN) at more than 1200 locations, more than 300 new locations over the project period, and network connectivity from alternate service provider at 150 locations (our primary network service provider is BSNL).

It is indeed a remarkable achievement that the Indian Customs’ EDI (Electronic Data Interchange) Gateway (ICEGATE) transited to the GST era in the midnight of 30th June 2017 enabling the collection of the first GST payment in the form of IGST levied on imports and the Compensation Cess, in a significantly seamless fashion, thereby ensuring that there was absolutely no disruption in the import or export systems.

Training the workforce

The National Academy of Customs Indirect Taxes and Narcotics (NACIN) is the authorized organization for training all officers of the Federal and State Governments in India. In an ongoing effort, the following achievements are worthy of special emphasis:

Nearly 52,000 officers (from both the Centre and the States) have been trained by the National Academy of Customs Excise and Narcotics (now renamed as NACIN) from September 2016 to January 2017 through a multi-layered training program across India. This was the first structured program to train the indirect tax officials of the Centre and States in the concepts, processes and procedures of GST (based on the Model GST Law as it existed then). NACIN further held refresher trainings and is presently doing updated post-roll out training modules.

There are at present 25 source trainers (who were predominantly involved in the drafting of the laws and rules) and 310 Master trainers who have been instrumental in manning the seminars and other training programs across India. For the tax incidence to commence on 1st July 2017, it was very necessary that the industry and the officers – the two sides of the GST coin, be prepared and hence a great necessity was felt to indulge in massive outreach programs and campaigns. Dr. Hasmukh Adhia, Revenue Secretary, Government of India showed the way, by personally travelling to 14 states to conduct town-hall meetings, press conferences, seminars and other such interactions to educate the trade and other stake holders on GST. A dedicated website (https://gstawareness. cbec.gov.in) was specially created for the purpose.

| North | 1111 |

| South | 877 |

| Central | 764 |

| East | 1239 |

| West | 1050 |

| Total | 5041 |

Table 7: Outreach Programs conducted till July 2017

In an ongoing exercise, 20 institutes of repute certified as ‘Approved Training Partners’ to impart ‘quality training at reasonable cost’ to members of trade/industry and other stakeholders. 8140 participants trained so far. NACIN has produced learning material in English, Hindi and 10 Indian regional languages and they include Frequently Asked Questions (FAQ), Do You Know series etc.,

Publicity and Awareness campaigns

Over 65 advertisements were released in nearly 300 newspapers across India in Hindi, English & 16 regional languages. On the occasion of GST launch on 30th June – 1st July, 2017, coverage was extended to more than 700 newspapers. Informational advertisements covered important aspects of GST viz. Registration/Migration, Transition Provisions, Composition Scheme, Outreach Programmes, Nil/low GST rates for items of use by common man, FAQs on specific topics like those for traders, Composition levy, Clarification on rates of GST for restaurants, Raising GST invoice easily, Easy & Online Return filing, Easy Accounting/Maintaining of Records in GST, How to Export under GST etc.

GST Seva Kendras (GST helpdesk) are operational in nearly 4500 locations across the country to assist the taxpayers in their compliance liabilities. An exclusive Twitter handle @askGST_GoI was launched for answering GST-related queries and has more than 50,000 followers. More than 100 videos on GST learning, Speeches, Press Conference, etc. have been hosted on the Youtube channel GST_India. Video campaigns in Facebook and broadcasting media have also been carried out extensively. Outdoor campaigns through hoardings/unipoles/bridge panels/bus queue shelters etc. at more than 4300 important sites across the country, including Seat back display in Air India flights, Delhi Metro, Mumbai Local Trains, Railway stations across the country, trains etc. have been done. Display of GST advertisements on LCD/LED screens installed at strategic locations, viz. airport, railway stations public transport etc. have also been done.

Taxman and GST – a new chapter in every office

Under CBEC, the body of the Federal Government administering GST, 21 GST zones and 107 GST Commissionerates have been created. Zones and Commissionerates are congruous with state boundaries. Special focus has been given to the North-Eastern areas of India. 48 GST Audit and 49 GST Appeal Commissionerates have also been created. Similarly, the states have also undertaken an exercise to reorganise their offices in every district to create an adequate interface between the taxman and the taxpayer. To better serve the taxpayers and to handhold them during the mammoth reform, GST Seva Kendras have been set up in every GST Office.

Roll out – The Art of the Impossible

The 1st July 2017 roll out date was announced by the Union Finance Minister post the 9th GST Council Meeting held on 16th January 2017 in New Delhi.

The Union Cabinet, which met on 22nd June, 2017 under the Chairmanship of Prime Minister Narendra Modi acknowledged the contribution made by the Chief Ministers and Finance Ministers of all the States and all political parties which made it possible for GST to be implemented in the country from 1st July 2017.

The GST journey has just begun and this experiment in fiscal federalism will be a continuous and evolving process, typically embodying the colourful and at times, chaotic nature of Indian democracy. In days to come, the law and the procedures will mature and so will the attitude of the tax administration. The unique Indian story of GST will unfold and every manifestation of this story will be as remarkable as the one of its genesis.

GST may be a destination tax but for India it begins a new journey. It is a journey where India will awake to limitless possibilities to expand the economic horizons and loftier political visions. The old India was economically fragmented. New India will create one tax, one market, one nation. It will be an India where Centre and states work together towards the common goal of shared prosperity.

– Arun Jaitley

Finance Minister, Government of India & Chairperson, GST Council

1st July 2017; Central Hall, Parliament of India

A STORY OF EXTRAORDINARY

NATIONAL AMBITION

Journey continues..

APRIL 2019

GST Council Secretariat

A story of extraordinary national ambition, continued

The Goods and Services Tax

GST is a consumption tax based on the credit invoice method where only the value addition at each stage is taxed, with seamless flow of credit along the supply chain. It subsumed in its ambit a large number of consumption taxes that previously existed in India, administered separately by the Centre and the States, resulting in a greatly rationalized taxation structure.

The umbrella system of GST inter alia integrated the tax administrations of the Federal and State Governments, making it a single interface for the taxpayers, creating an IT backbone that would match the details of inward & outward supplies at the level of line items, eliminating the cascading effect of taxes thereby making the country’s exports more competitive in the global market and finally removing once and for all the age-old system of check posts for inter-State movement of goods.

Besides altering the industrial landscape of the country, GST is also a never-heard-before experiment in fiscal federalism. Cutting across ideologies, politicians, policy makers and tax administrators negotiated, bargained and arrived at decisions – all in the interest of greater common good. The legislations that made up GST were put in public domain for feedback multiple times at each stage, empowering all the stakeholders to deliberate on what kind of future they wanted to help design, in the truest spirit of democracy.

Primarily, GST is a tax levied on the supply of goods and services. In case of an inter-state supply, it is called integrated tax, levied by the Federal Government, administered jointly by the Centre and the States and later apportioned between them. In the case of an intra-state supply, it is levied in two components – the federal tax, levied by the Federal Government and the state tax/union territory tax, levied by the respective administrations.

Genesis of GST

The Kelkar Task Force on the Fiscal Responsibility and Budget Management (FRBM) Act, 2003 suggested a comprehensive GST based on the Value Added Tax principle. The proposal to introduce a National-level GST was first mooted in the Budget Speech in the year 2006. The responsibility of preparing a Design and Road Map for the implementation of GST was assigned to the Empowered Committee of State Finance Ministers (EC). Based on inputs from the Government of India and the States, the EC released its First Discussion Paper on Goods and Services Tax in November 2009. The Constitution (115th Amendment) Bill was introduced in the Lok Sabha in March 2011. However, the issue of payment of compensation to the States for loss of revenue remained an important bone of contention between the Centre and the States, and in the face of resistance in the Parliament, the Constitution (115th Amendment) Bill was referred to the Standing Committee on Finance for examination. Deliberations between the Centre and the States on the Constitutional Amendment Bill continued in the Empowered Committee till the dissolution of the 15th Lok Sabha in May 2014, however no consensus could be formed around the contentious issues of compensation, treatment of petroleum products and subsuming of entry tax. The amendment bill lapsed with the dissolution of the 15th Lok Sabha.

In June 2014, the draft Constitution Amendment Bill was sent to the Empowered Committee after approval of the new Government. Trust deficit plagued all dialogues between the Centre and the States on GST. States had apprehensions about surrendering their taxation jurisdiction, treatment of petroleum products, subsuming of taxes such as entry tax and purchase tax and getting adequate compensation for any loss of revenue for five years. The Union Finance Minister met with the Chairman of the Empowered Committee and Finance Ministers of States on 3rd July 2014 and 11th December 2014. He further met the Chairman of the Empowered Committee and Finance Ministers of Gujarat, Haryana, Punjab, Tamil Nadu and Karnataka on 15th December 2014. All the pending contentious matters were resolved in these two meetings, wherein it was decided that a provision would be inserted in the Constitution Amendment Bill itself for payment of compensation to the States for the first five years post implementation of GST and that the GST Council would recommend the date on which GST would be made applicable on petroleum products. In terms of this broad consensus, the Government sought the approval of the Cabinet to introduce the revised Constitution (122nd Amendment) Bill in the Parliament. The Constitution (122nd Amendment) Bill, 2014, was thus introduced in the Lok Sabha on 19th December 2014.

In the meanwhile, to bridge the trust deficit, the Union Finance Minister also obtained the approval of the Cabinet for paying compensation to the States for loss of revenue caused to them on account of reduction in the rate of CST from 4% to 2%, for the years 2010-11, 2011-12 and 2012-13, over a three-year period beginning 2014-15. This had been a long-standing demand of the States and non-payment of this compensation amount in the past years had adversely affected the deliberations between the Centre and the States.

The Constitution (122nd Amendment) Bill was passed by the Lok Sabha on 6th May 2015, and was sent to Rajya Sabha for consideration. In Rajya Sabha, the Bill was sent to a Select Committee for examination on 12th May 2015. The Select Committee submitted its report on 22nd July 2015. Thereafter, the Bill was passed by both Houses of the Parliament on 8th August 2016. After ratification by 50% of the States, the Constitution (101st Amendment) Act, 2016 was assented to by the President on 8th September 2016. After the passing of this first and biggest hurdle, the process for bringing this historic reform acquired significant momentum.

After over ten years of rigorous and widespread consultations, the Goods and Services Tax was implemented on 1st July, 2017. Since then, the GST Council, the apex body of policy formulation in the new indirect tax regime, has met 16 times. In these meetings, more than 150 agenda items were dealt with.

Since last one year, the Council has been witness to many improvements in the economy such as the increased formalization of the economy and widening of the tax base, as highlighted by the Economic Survey 2017-18.

Comparison of trends in Revenue in 2017-18 and 2018-19;

[Source: Ministry of Finance, PIB Press release dated 01 March 2019]

A unique experiment in public policy, this body epitomizes the federal setup envisaged by the Constitution. In its attempt to preserve and provide for differing opinions of different States, the Council has evolved a unique style of functioning of allowing detailed and threadbare discussion on every agenda point but finally deciding the issue by consensus. Though it is a political body, the discussions have been based on technical merits of an issue. There is remarkable eloquence and camaraderie in the Council meetings.

The way of the Council:

Conduct of the meetings:

Though the Constitution mandates that the Council should meet at least once in every quarter of a financial year, it has been meeting much more frequently, on an average once every 45 days. A tradition of holding some meetings outside Delhi to promote greater integration has been adopted. To respond to pressing issues, the Council also started meeting virtually through Video Conference.

Principle of unanimity:

For the first time in India’s history, an important subject such as the power of taxation is shared between the States and the Centre. Given the diversity of the needs and resource bases of the States, it is only natural that there would be difference of opinion among the States. However, propounded by the honourable Chairman of the Council, the Council has always adhered to the principle of unanimity. In a situation where such concurrence was not possible, the Council devised the following methods to achieve the objective.

The GST Council is India’s first experience at cooperative-federalism based decision-making authority. We cannot afford to risk a failure and, therefore, it’s functioning has to arouse confidence amongst all States. – Arun Jaitley, Hon’ble Finance Minister

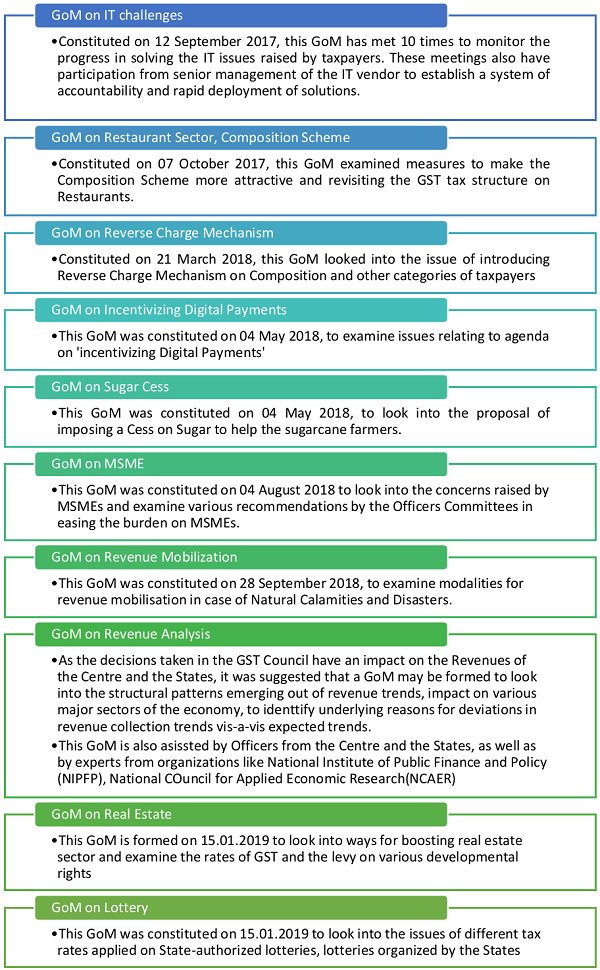

Groups of Ministers(GoMs):

Whenever concurrence of the members of the Council was hard to achieve, or when an issue required in-depth discussion or wider consultation, the Council formed sub-groups of Ministers similar to Parliamentary Committees, to look into the issues and build consensus. Till now, 10 such Groups of Ministers have been formed to consider specific issues:

Recommendations of some of the Groups of Ministers like the GoM on Restaurant Sector, GoM on Reverse Charge Mechanism have been accepted by the Council. GoM on IT challenges is a standing GoM which is monitoring and guiding the IT implementation aspect of GST. Other GOMs are at various stages of deliberation. The GoMs have helped to find common ground with respect to the issues referred to them. These GoMs afford an element of nimbleness to the proceedings of the Council by meeting as frequently as situations demand.

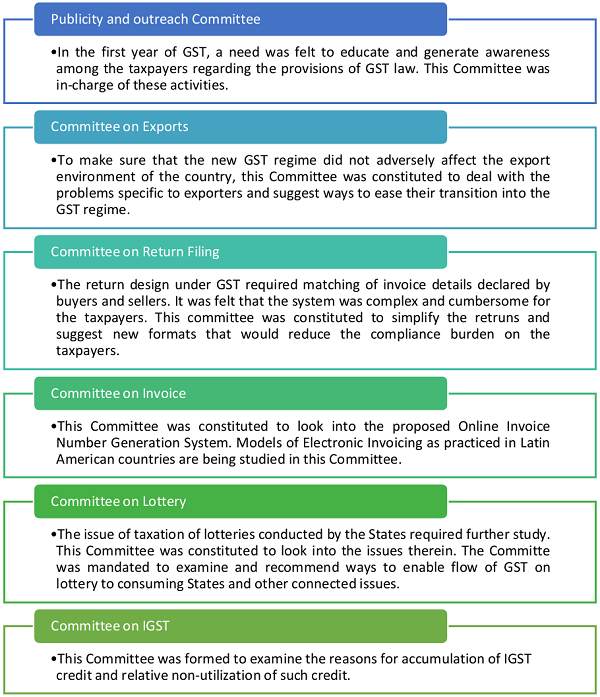

Officer Committees:

Time and again, in the debates of the Council, few issues emerged which needed further technical examination. To consider these, the Council formed the following 19 committees with officers from the States and the Centre.

Major initiatives:

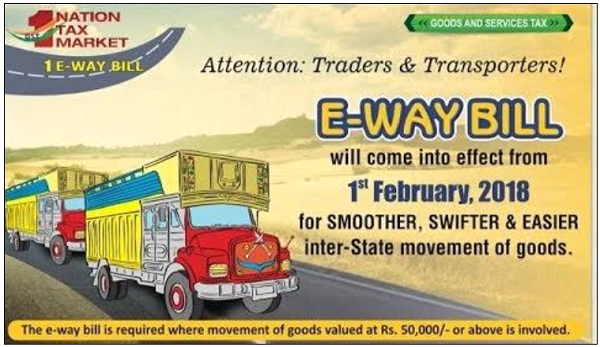

E-waybill mechanism:

To bring the entire supply chain into books, the GST Council recommended the rollout of E-waybill mechanism from 01.04.2018. To facilitate the smooth transition, the E-waybill mechanism was first introduced for inter-State movement of goods and later for intra-State movement in a staggered manner. A total of around 34 Crore E-waybills were issued till November 2018.

Simplification of Legal provisions:

During the first year of operation of GST, many representations were received from different stakeholders. These representations were examined by various officers Committees and also some Groups of Ministers. As many of them required amendments in GST Law, a new Committee called Law Review Committee was formed with members from State and Central governments to suggest possible amendments. The proposed amendments were then placed in public domain for comments, after which the Amendment Act was passed by the Parliament. The States are also in the process of amending their respective GST Acts.

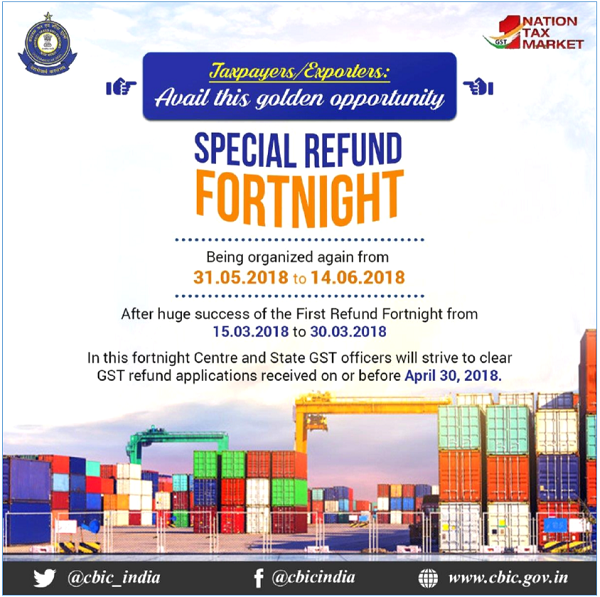

Boost to Exporters:

To ease the burden on exporter who were facing working capital shortages, the GST Council in its meeting on 10 March 2018, directed all the authorities to proactively clear refund claims. To this end, two special refund fortnights were conducted, one from 15.03.2018 to 29.03.2018 another from 31.05.2018 to 16.06.2018. The Council also formed a Committee of officers to look into various measures like e-wallet scheme to ease the burden on exporters.

Rate rationalization:

Indirect taxes, in general, are considered regressive as they do not differentiate between the richer and poorer sections of the society. However, an element of progressivity has been added in GST through multiple rate slabs with higher incidence on the products consumed by the affluent section of the society and lower rate of tax on mass consumption items. During the one year of implementation of GST, rates have been revised on the lower side multiple times, to lower the burden on taxpayers. The number of items on which 28% GST rate is applicable was reduced from initial 228 to 28.

Graduated transition to the ‘ideal’ GST regime resulted in the Indian economy bypassing some of the anticipated shocks in the form of increase in inflation or a reduction in growth rate.

– National Institute of Public Finance and Policy, Working Paper 255

Amendment of GST Acts:

To enable the implementation of many trade-friendly decisions taken by the GST Council since the launch of the new tax regime, the Goods and Services Acts of all the States and the Centre required few amendments. It was important that these Amendment Acts were passed in time to ensure uniform implementation of tax policies across the Country. The GST Council Secretariat coordinated with the States and Union Territories with Legislature to ensure that the Amendment Acts were passed in the respective legislatures.

| Sl. No |

Name of State | Dates on which SGST Amendment Act had been published in the Gazette or promulgated |

| 1 | Andhra Pradesh | 23rd October 2018 |

| 2 | Arunachal Pradesh | 03rd December 2018 |

| 3 | Assam | 24th October 2018 |

| 4 | Bihar | 5th October 2018 |

| 5 | Chattisgarh | 5th October 2018 |

| 6 | Delhi | 15th January 2019 |

| 7 | Goa | 23rd November 2018 |

| 8 | Gujarat | 8th October 2018 |

| 9 | Haryana | 28th September 2018 |

| 10 | Himachal Pradesh | 05th November 2018 |

| 11 | Jammu & Kashmir | 13th November 2018 |

| 12 | Jharkhand | 15th October 2018 |

| 13 | Karnataka | 29th September 2018 |

| 14 | Kerala | 15th October 2018 |

| 15 | Madhya Pradesh | 26th November 2018 |

| 16 | Maharashtra | 13th October 2018 |

| 17 | Manipur | 15th October 2018 |

| 18 | Meghalaya | 7th January 2019 |

| 19 | Mizoram | 29th October 2018 |

| 20 | Nagaland | 29th September 2018 |

| 21 | Odisha | 23rd October 2018 |

| 22 | Puducherry | 18th December 2018 |

| 23 | Punjab | 23rd October 2018 |

| 24 | Rajasthan | 01st October 2018 |

| 25 | Sikkim | 29th September 2018 |

| 26 | Tamil Nadu | 14th November 2018 |

| 27 | Telangana | 15th January 2019 |

| 28 | Tripura | 12th October 2018 |

| 29 | Uttar Pradesh | 14th October 2018 |

| 30 | Uttarakhand | 16th October 2018 |

| 31 | West Bengal | 28th November 2018 |

MSMEs, Composition Scheme:

The Council took special note of the issues related to the Medium, Small and Micro Enterprises. To ease their burden of compliance as well as burden of taxation on them, the Council has announced the following measures:

| Higher exemption threshold limit for supplier of goods: | Registration threshold increased to Rs. 40 lakh in most States |

| Composition scheme for services and mixed suppliers: | A composition scheme is made available for suppliers of services (or mixed suppliers) with a tax rate of 6% (3% CGST + 3% SGST) having an annual turnover in preceding financial year upto Rs 50 lakhs. |

| Increase in turnover limit for the existing composition scheme: |

The limit of annual turnover in the preceding financial year for availing composition scheme for goods increased to Rs 1.5 crore |

In total, the GST Council met 33 times, took more than 920 decisions, which have already been implemented through 349 Central notifications. Almost equal number of notifications have been issued by each State.

“GST is now on the track and is in process of fast settling down. The thrust of the Government is to lower the tax rate and widen the tax base and keep the revenue collections moving-up. “

– Shri Arun Jaitley, Union Minister of Finance, Chairman, GST Council

PIB Press release dated 05 March 2019

The potential areas of future work:

Widening of GST ambit:

To facilitate free flow of credits, various stakeholders requested the inclusion of Petroleum and other products which are presently outside the ambit of GST. Article 279A(5) gives the Council the power to decide the date on which GST may be made applicable on Petroleum products.

Simplification of Returns:

With great attention given to the feedback from businesses and taxpayers, the GST Council decided to revamp the return forms with high premium on simplification and ease of filing. Accordingly, the Council approved the new return forms ‘Sahaj’ and ‘Sugam’ slated to be introduced soon. The new returns also make filing nil returns easier, through adoption of SMS based return filing mechanism.

Futuristic Returns (Returns 3.0):

Guided by the vision of the Revenue Secretary, frameworks of new GST Returns that can possibly automate the entire tax return process are being developed. This new model of returns draws the best from international practices, experiences in the field of tax management. The possibility of including new tools like invoice generation system, one-pager automated returns format are also being looked at.

Restructuring of GST Council Secretariat:

The Cabinet Note creating the GST Council Secretariat mandated it with assisting the Council in the conduct of its meetings, research in tax policy. As the GST regime continuously looks for innovation, feedback, the Council Secretariat is also being revamped to include a Research Centre in its premises. This Research Centre now hosts databases from International Monetary Fund, World Bank and European Union VAT Directives. Reflecting the true federal spirit of the GST Council, its Secretariat also has officers from Centre and the States working together to assist the Council. Apart from these new initiatives, the Council Secretariat also began hiring Research Assistants, Consultants to bring in diverse experiences, insights in tax policy design.

Pragmatic taxation:

New age taxation system requires the incorporation of new methodologies into policy design. The Council could, in future, look towards the following tools to enhance indirect tax policy.

1. Compliance Cost assessment:

The very nature of a regulation is that it imposes a requirement on the businesses to commit a portion of its resources in compliance. In today’s world of trade, where resources like time and money are valued more than ever before, it is desirable that any new regulation proposed by the government agencies is carefully crafted after considering its implications on the compliance requirements faced by the businesses. Compliance Cost assessments (CCAs) are the tools to measure these implications. They assist in creating a favourable business environment while also taking care of social and economic objectives of tax policy design.

2. Electronic tax administration:

To enhance objectivity, there is a need to eliminate the physical interface between the taxpayers and the tax officials. Some of the modules like registration are already automated. Full automation of business process of refund is the need of the hour.

3. Nudge Unit:

.Behavioural Economics is a newly emerging field of research which is the method of economic analysis that applies psychological insights into human behaviour to explain economic decision-making. Recently, the Central Board on Indirect Taxes and Customs (CBIC) has formed a nudge unit, comprised of Officers, academic experts, economists to study and improve the tax compliance through carefully designed behavioural interventions.

4. Data based policy design:

For the first time, entire indirect taxation system is unified in the form of GST. As quoted by the Economic Survey, GST brought for the first time, huge amounts of return data and transaction data which opens up a new window for understanding the Indian Economy. The data not only helps in the better understanding of the economy, but also assists in designing the tax policy that assures maximum social benefit. The potential of data-based design was realized in the understanding of the taxpayer segments and subsequent discussion led to the increasing of the turnover threshold for Composition Scheme and providing quarterly returns for small taxpayers. This sort of evidence-based policy or data-driven policy also provide the Government with immediate feedback, a degree of nimbleness which is difficult to achieve in traditional set-up. Data analytics is also playing a big role in catching tax evasion. Through network analysis, patterns of circular trade are identified and evaders are forced to bring their accounts to books.

[With GST,] a whole new world has indeed opened up to followers of the Indian Economy, and much exciting research lies ahead.

– Economic Survey, 2017-18

5. Efficient Tax Administration:

New methodologies like the World Bank’s PEFA (Public Expenditure and Financial Accountability), International Monetary Fund’s TADAT (Tax Administration Diagnostic Assessment Tool) are available now to measure the efficiency, effectiveness of the revenue administration. The Council is looking at such methodologies to benchmark the performance against similar administrations worldwide and improve the tax administration.

An example worth emulating:

It is the very first time in India that a truly federal, policy-making institution was successful in its mandate. This success is due to the accommodative approach that the Council adopted for itself realizing the different needs of the States. Having only one indirect tax policy making institution for the entire country, has made a responsive institution marked with a great degree of agility.

[An article in the Indian Express, calls for GST-type Council for agriculture]

Experts have been suggesting that similar cooperation among the States and the Centre is needed in multiple fields like agriculture, inter-State rivers, health etc., and that the GST Council has proved to be an example that is worth emulating.

Conclusion:

For any country to progress, it is imperative that its tax administration is efficient, its tax policies are transparent. The GST Council in its first year, succeeded in a significant manner in moving closer to these objectives. It has also paved the way for a robust economic growth in the country.

Source : Ministry of Finance, Government of India