APPLICABILITY OF GST ON RENT

♦ The basic definition of outward supply includes rental income in the ambit of supply. Renting of immovable property is specifically considered as a supply of services in the GST regime.

♦ As per the GST Act, the following types of rents are covered under GST:

any lease, tenancy, easement, license to occupy Land any lease or letting out of the building including commercial or residential property for business or commerce (wholly or partly).

This type of renting is considered as a supply of services, and hence, GST would be attracted.

Vide Central Tax Rate notification 12/2017 ,rent received from renting of residential dwelling unit for residential purpose is exempt from GST. However Government has withdrawal this exemption by Central Tax Rate notification no.05/2022 with effect from 18th July 2022.Government also inserted same service in RCM by amending notification no.13/2017.

So, from 18th July 2022 RCM is applicable on renting of residential dwelling from Any person to registered person.

SIMPLIFICATION OF GST ON RENT

- To Simplify GST on Rent we are dividing it in Three categories

1) Any Property to be used for Commercial purpose(Forward Charge)

2) Any property to be used for Residential Purpose (Reverse Charge)

3) Specified Exempt Rent Income

So , We will check Taxability one by one category

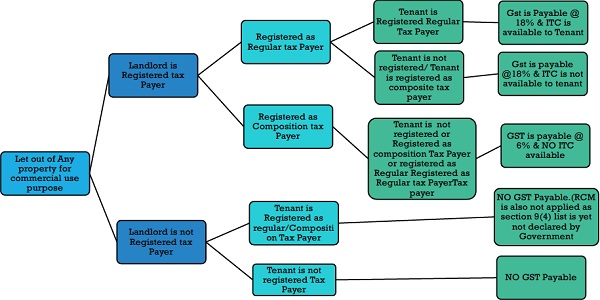

1) Any Property to be used for Commercial purpose (Forward Charge)

Any Registered person let out any property for Business purpose will be treated as Taxable supply and Rent received for such let out by Registered Person will be taxable and he has to pay tax on forward charge basis.

If registered person is registered as Regular Tax payer than GST rate will be 18%.(ITC is available to Tenant if he is also registered Tax Person)

If Registered person is Composition Tax payer than GST rate will be 6%(GST here treated as composition leavy, Threshold limit is 50,00,000/- rupees for service provider )(ITC is not available to Tenant if he is also registered Tax person)

Chart in next Page will brief you all transactions related to this category.;

Any Property Let Out for commercial purpose

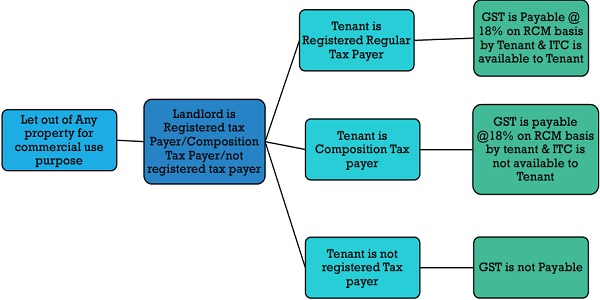

2) Any Property to be used for Residential purpose (Reverse Charge)

Any Registered person take property on Rent for Residential purpose from any person have to pay GST on RCM basis as per Central GST Rate notification 05/2022

If registered person is registered as Regular Tax payer than RCM GST rate will be 18%.(ITC is available paid as RCM)

If Registered person is Composition Tax payer than RCM GST rate will be 18%(GST here treated as composition leavy, Threshold limit is 50,00,000/- rupees for service provider )(ITC is not available paid as RCM)

Chart in next Page will brief you all transactions related to this category.;

Any Property Let Out for Residential purpose

3) Specified Exempt Rent Income

Vide Central Tax Rate notification 12/2017 Rent received by the registered charitable trust or a religious trust exempt from GST where:

- Rent on rooms is Rs 1,000 or less per day.

- Rent on shops, business units, community halls of such charitable trust are Rs 10,000 or less per day.

- Rent on community halls or open area charged Rs. Ten thousand or less per day.

Rent on shops, business units, community halls of such charitable trust are Rs 10,000 or less per day.

It is Rs.10000/= per month not Per day. Please revisit Notification No.12/2017 CT (R) dated 28.06.2017

whether rent from shops of rs. 10000/- per month is per shop or all the shops put together

Hello, If any NGO provide it’s building on rental to Postal Department of India, so is it taxable under GST??

My partnership firm is registered as composition dealer and owner of my rented shop is unregistered person. I pay 70000 rent per month. Is gst on this rent applicable?