Dr. Sanjiv Agarwal

GST Models

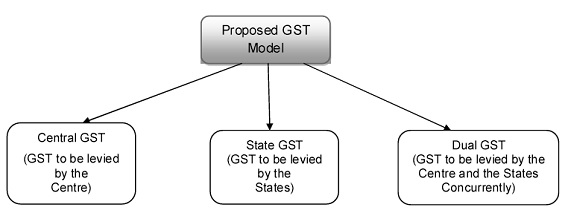

There are three prime models of GST:

- GST at Central (Union) Government level only

- GST at State Government level only

- GST at both, Union and State Government Levels

Canada has GST at Union level extending to all goods and services covering all stages of value addition. In addition, there is tax at province (State) level in different forms which include VAT, Retail Sales tax and so on. European Union (EU) Nations (each one is independent Nation but, part of a Union and have agreed to adopt common principles for taxation of goods and services) have adopted “classic” VAT.

In the Indian context, Constitution of India specifically reserves the power to impose tax on specific activities to specific level of Government, e.g., tax on import of goods can be imposed by Union Government only whereas tax on sale of goods involving movement of goods within the State can be imposed by State Governments only.

Get Knowledge about Reverse charge under GST

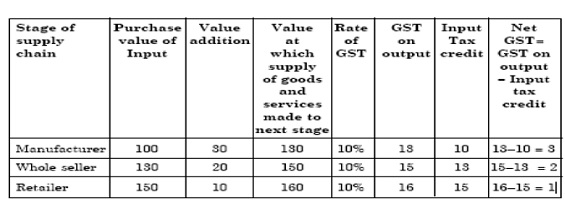

Illustration of GST

Central GST (CGST)

Under this option, the two levels of Government would combine their levies in the form of a single National GST, with appropriate revenue sharing arrangements among them. The tax could be controlled and administered by the Central Government. There are several models for such a tax. Australia is the most recent example of a National GST, where it is levied and collected by the Centre, but the proceeds are allocated entirely to the States.

In the case of a Central GST (where all goods and services are taxed by the Central government only), the Centre will collect most of the country’s total tax revenue, leaving very little for the sub-national Governments. As against this, the present proposal is to have a dual GST.

A single national VAT has great appeal from the perspective of establishment and promotion of a common market in India. However, the States may worry about the loss of control over the tax design and rates. Indeed, some control over tax rates is a critical issue in achieving accountable sub-national governance and hard budget constraints. The States may also be apprehensive that the revenue sharing arrangements would over time become subject to social and political considerations, deviating from the benchmark distribution based on the place of final consumption. The Bagchi Report also did not favour this option for the fear that it would lead to too much centralization of taxation powers.

The key concerns about this option would thus be political. Notwithstanding the economic merits of a National GST, it might have a damaging impact on the vitality of Indian federalism.

Salient Feature of CGST

- CGST on both , goods and services

- To be levied, controlled and administered by Union.

- Levied by the Centre through a separate statute on all transactions of goods and services made for a consideration.

- Exceptions would be exempted goods and services, goods kept out of GST and transactions below prescribed threshold limits.

- CGST would be levied across the value chain.

- Rates for CGST would be prescribed appropriately reflecting revenue considerations and acceptability.

- Two Governments will combine their various levies into single GST.

- Proceeds to be shared between Centre and States .

Advantages

- If levied on a comprehensive base at a single rate, it would clear the system of virtually all economic distortions and classification disputes.

- Replacing 36 taxing Statutes (of the Centre and 35 States and Union Territories) with only one would lead to a substantial reduction in compliance costs and free up resources for other more productive pursuits.

- It would make common market for India a reality. Goods and services would move freely within India with no check-posts, internal-tax frontiers or other barriers to trade.

Disadvantages

- Near impossibility of achieving the structure – It will require drastic modification to the Constitution of India.

- It might upset the present concept of fiscal federalism, which is the cornerstone of Indian polity.

- Entire infrastructure developed for taxation at both levels will have to undergo huge change.

- States may not agree to give up the power of taxation and depend on the Union for resources.

Read Other Articles from Dr. Sanjiv Agarwal

Author Bio