GST Insights- Further Relief Measures- COVID-19

–Updated Compliance Chart for GSTR-3B and GSTR-1

-Reduction in Late fee in filing GSTR-3B

-Change in calculation of Interest amount if filed after relief dates

-Relief provided in filing GSTR-3B for May 2020 to August 2020

-Reduced rate of Interest @9% if GSTR-3B filed by Sept. 20

-One-time chance to file revocation application against cancellation

-Filing of GSTR-1 and GSTR-3B by EVC in case of C

Various Notifications have been issued to amend the existing relief provided by the Government amid COVID-19 in terms of waiver of late fees, interest and reduced rate of Interest @9% p.a. for the period of February, March and April 2020 and similar relief has been provided for the period May, June & July 2020 and extension of due date for August 2020. The relief measures and other updates are summarized below:

Page Contents

- A. Waiver of late fees – GSTR-1

- B. Relief in GSTR-3B (February 2020 to August 2020)

- C. Change in calculation of Interest amount in case of failure to file GSTR-3B by relief dates

- D. One-time Reduction in Late fee – GSTR-3B (July 2017 to January 2020)

- E. Further extension of compliances under N/N 35/2020 to 31stAugust 2020

- F. One-time opportunity to file revocation application against cancellation of GST registration- ROD Order dated 25thJune 2020

- G. Filing of GSTR-3B and GSTR-1 by EVC- Further extension

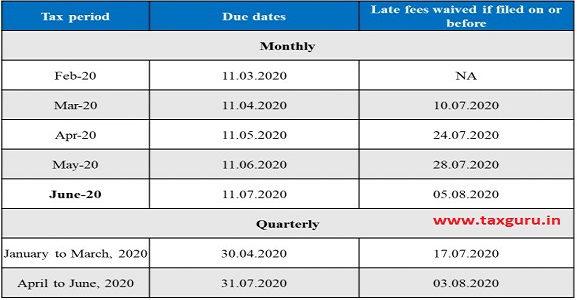

A. Waiver of late fees – GSTR-1

B. Relief in GSTR-3B (February 2020 to August 2020)

(1) Aggregate turnover of more than Rs. 5 crores

(2) Aggregate turnover upto Rs. 5 crores- State List-1

Applicable States: Taxpayers with principal place of business in the States of Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshadweep

(3) Aggregate turnover of upto Rs. 1.5 crores- State List-2

** Taxpayer with principal place of business in the States of Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi,

Comments:

Please note that there has been no change in due date to file GSTR-3B except for May and August 2020. Hence, if the GSTR-3B for a particular month say March 2020 is not filed on or before relief dates provided, then late fee shall be levied from existing due dates i.e. from 20th/22nd /24th April 2020.

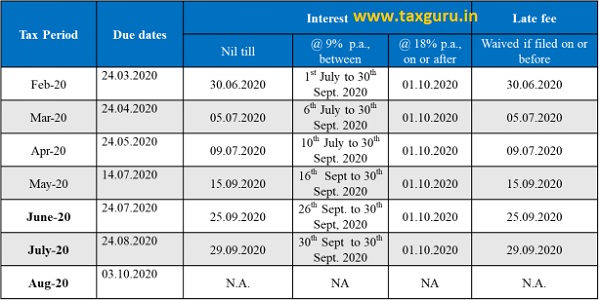

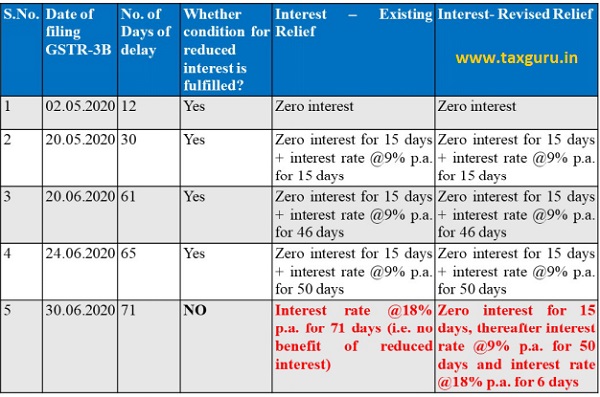

C. Change in calculation of Interest amount in case of failure to file GSTR-3B by relief dates

One of the major relaxations which has been given now is change in manner of calculation of Interest amount where GSTR-3B for the period February 2020 to April 2020 are not filed by the prescribed relief dates. Earlier, Interest @18% p.a. would be charged from the existing due date if the GSTR-3B is not filed within prescribed relief dates.

For example, the due date to file GSTR-3B for March 2020 for taxpayers having aggregate turnover having more than 5 crs. is 20th April 2020. As per relief given, the GSTR-3B is required to be filed by 24th June 2020 to avail benefit of Nil interest for first 15 days and reduced interest rate of 9% p.a. thereafter. However, if GSTR-3B is filed after 24th June 2020, then Interest @18% p.a. would be charged from 21st April 2020.

Now after amendment in the mechanism of calculation of Interest, Interest @18% p.a. will be charged from 25th June 2020 instead of 21st April 2020. The comparative chart is reproduced below:

Comments:

This will have massive respite for businesses who are struggling to meet even the revised deadlines of the Government in filing GSTR-3B. This will reduce the interest burden if taxpayers fail to avail the benefit of relief dates announced.

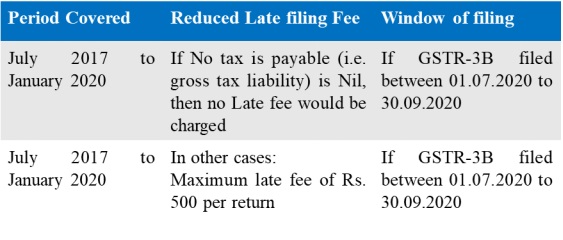

D. One-time Reduction in Late fee – GSTR-3B (July 2017 to January 2020)

The one-time relief in the form of substantial reduction in late fee has been given to encourage pending compliances as under:

E. Further extension of compliances under N/N 35/2020 to 31stAugust 2020

By way of the CGST Notification No. 35/2020 dated 03.04.2020, it has been notified that where any time limit for completion or compliance of any action, by any authority or by any person which falls during the period from the 20.03.2020 to 29.06.2020, then such time limit shall be extended to 30.06.2020

Now, CGST Notification No. 55/2020 has been issued to amend CGST Notification No. 35/2020 to further extend the period from 30.06.2020 to 31.08.2020.

F. One-time opportunity to file revocation application against cancellation of GST registration- ROD Order dated 25thJune 2020

Various taxpayers have faced cancellation of GST registration due to non-filing of GSTR-3B for the consecutive period of 6 months and CMP-08 for a consecutive period of 3 quarters and time to file revocation application within 30 days or time to file appeal within timelines under Section 107 has been elapsed and taxpayers could not file the application of.

As a one-time opportunity, Government has issued GST (Removal of Difficulties) Order, 2020 dated 25.06.2020 wherein they have provided that the time limit of 30 days to file revocation application as contained in Section 30(1) of the CGST, 2017 shall be counted from later of the following dates where cancellation order has been passed upto 12th June 2020 on account of non-filing of GST returns:

(a) Date of service of cancellation order

(b) 31.08.2020

Comments:

Few taxpayers have filed the returns and applied for revocation of cancellation of GST registration, however, the Revenue authorities are rejecting the requests even after full compliance of the requirements of GST law. It is noteworthy that similar relief may also be provided in such cases where Rejection Order for Revocation of cancellation of GST registration has been filed as route of filing of the Appeal under Section 107 of the Act is a long route and current need is to have immediate restoration of GST registration.

G. Filing of GSTR-3B and GSTR-1 by EVC- Further extension

CGST Rules, 2017 have been amended to provide that GSTR-1 and GSTR-3B can be filed by EVC by Companies instead of mandatory requirement to attached upto 30th September 2020 (CGST Notification No. 48/2020 dated 19.06.2020).

(CA Nikhil M. Jhanwar)

Disclaimer: The information in this document is for educational purposes only and nothing conveyed or provided should be considered as legal, accounting or tax advice.

Author Bio