“Explore the impact of GST on healthcare services. Currently exempt, healthcare providers face increased costs without input tax credit. Learn about GST rates on medical equipment, the classification of healthcare services, and exemptions. Discover the potential benefits of allowing input credits and proposing a lower GST rate, fostering healthcare infrastructure development and reducing the burden on patients. Stay informed about recent changes and clarifications, ensuring compliance with GST regulations in the healthcare sector.

Health care is the most crucial part of human lives. Health is the second largest reason for pushing people below the poverty line. According to official estimates, 25-30 percent of people do not seek health services because of their inability to afford it. More than 40 per cent of hospitalized people take loans or sell assets to pay for treatment. As high as 80 per cent people pay out-of-pocket for healthcare. A study based on household surveys in rural locations of Maharashtra, Bihar and Tamil Nadu revealed that almost 90 per cent of those in need of tertiary treatment die a slow and painful death because they cannot afford surgical treatment. The remaining 10 per cent, who can afford it, end up spending a better part of their life’s savings for treatment. Health care cost is the commonest reason for rural indebtedness. One sick person in the family can bring them down below- poverty-line perpetually.

At present Healthcare services are exempt from GST. As it is Exempted Services health care service providers are not eligible to avail credit on the input taxes paid by it, which ultimately becomes a cost for the service provider. In this way GST increase the day to day operating cost of healthcare unit. For example, hospitals are paying 12% tax on a dialysis machine, tubing’s, dialysis needles, Catheter, plasma filter, dialysis fluid which was earlier in the tax slab of 5% tax rate. It increased the dialysis cost for kidney patients. This is just an example, there are so many other medical equipment which cost went up like the lead valve of a pacemaker are imposed by 18% tax and CRT-ICD are taxed at 12% which is costing 15,000-20,00 extra on pacemaker and 40,000 extra on CRT-ICD.

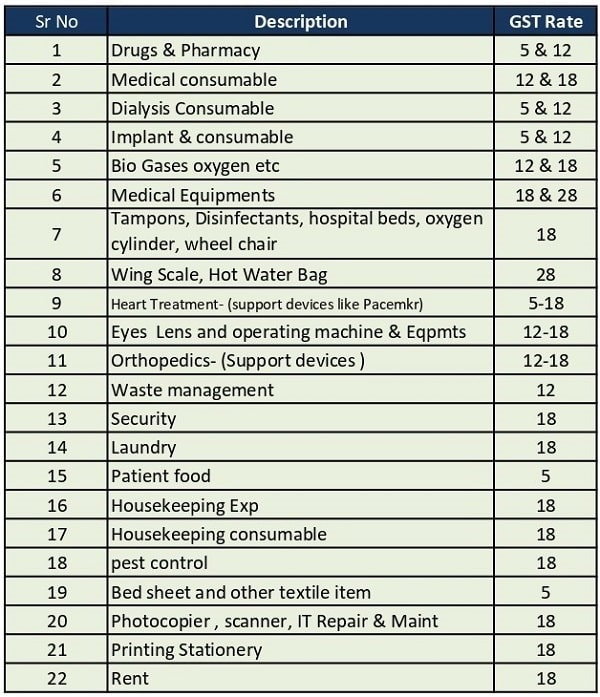

If we go through the GST Rate charged on various Input services required for day to day operation of a healthcare unit, we can understand how much GST input a healthcare service providers has to forgo resultant it increase the cost of Healthcare Operation :-

If healthcare industry is allowed to take input, it will lower the cost while purchasing life-saving medicines. And overall cost of healthcare services will actually come down benefitting larger section of the people. In case GST council believes that zero-rating benefit is not sustainable, Government may consider the option to treat the health care services as taxable supply of services at a lower rate of 5%. It will also boost Health care Infrastructure, Health service providers would be able to avail loans at lower rates and be able to invest more on infrastructural developments and bridge the resource gap, adopt IoT & Digital technologies, invest in R&D and up skill the workforce

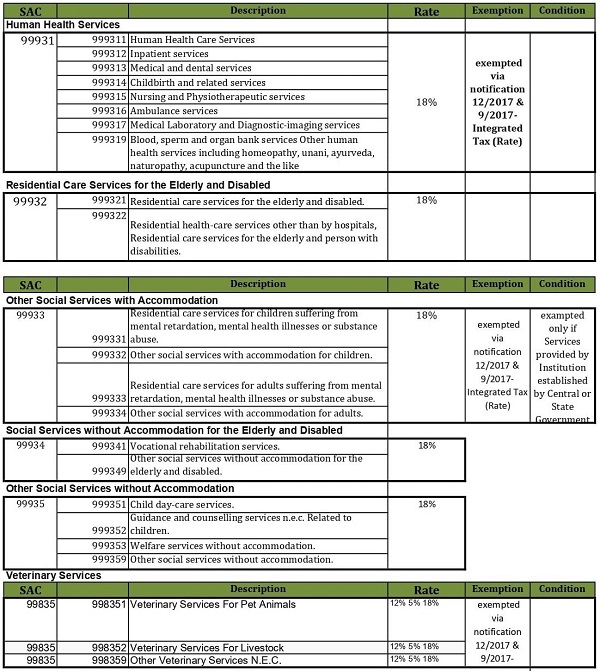

Classification of Healthcare Services under GST

SAC code for hospital, doctor and medical services fall under two categories of the SAC headings. Majority of the hospital and doctor services by a clinical establishment, an authorized medical practitioner or Para-medics fall under human health and social care services. On the other hand, veterinary services by a veterinary clinic in relation to health care of animals or birds fall under other professionals, technical and business services.

Exemption to Health Care Services

Exemption are provided to Health Care Services vide Notification No. 12/2017-Central Tax (Rate) dated 28-06-2017 and Notification No.9/2017 – Integrated Tax (Rate) dated 28-06-2017.

Exemption to Health Care Services

The GST Rate for services has a catch-all clause which mentions that if a service is not exempt from GST explicitly or the GST rate for the service is not provided for explicitly, then an 18% GST rate would be applicable. Hence, some of the above services not rendered by a clinical establishment or an authorized medical practitioner or para-medics could be subject to GST. In case a person supplying services is taxable under GST, then GST Registration must be obtained, and GST returns must be filed.

Besides Notification No. 12/2017-Central Tax (Rate) dated 28-06-2017 and Notification No.9/2017 – Integrated Tax (Rate) dated 28-06-2017, it is also important to refer some of the relevant circulars clarifying the GST taxability/ exemption under GST of various services involved in the healthcare sector. In Circular no. 27/01/2018-GST dated 04th January 2018 at Serial No 4, it has been clarified that Service of renting of rooms in hospitals to in-patients is exempt. However vide notification No. 03/2022 dated 13 July 22, GST Council decided to levy 5% GST on hospital rooms (non-ICU) having daily room rent exceeding Rs. 5,000 without GST Input. In this notification GST Dept also withdrawn exemption of Biomedical waste treatment & disposal services provided to clinical establishment which was exempt vide earlier notification 12/2017 and 09/2017 and levy GST @12%.

Clarification Regarding Health care Services

In Circular No. 32/06/2018 TRU dated 12-02-2018 at serial no 5 it has been clarified regarding Healthcare services as follows:

| 5 | Is GST leviable in following cases:(1) Hospitals hire senior doctors/ consultants/ technicians independently, without any contract of such persons with the patient; and pay them consultancy charges, without there being any employer-employee relationship. Will such consultancy charges be exempt from GST? Will revenue take a stand that they are providing services to hospitals and not to patients and hence must pay GST?

(2) Retention money: Hospitals charge the patients, say, Rs.10000/- and pay to the consultants/ technicians only Rs. 7500/- and keep the balance for providing ancillary services which include nursing care, infrastructure facilities, paramedic care, emergency services, checking of temperature, weight, blood pressure etc. Will GST be applicable on such money retained by the hospitals? (3) Food supplied to the patients: Health care services provided by the clinical establishments will include food supplied to the patients; but such food may be prepared by the canteens run by the hospitals or may be outsourced by the Hospitals from outdoor caterers. When outsourced, there should be no ambiguity that the suppliers shall charge tax as applicable and hospital will get no ITC. If hospitals have their own canteens and prepare their own food; then no ITC will be available on inputs including capital goods and in turn if they supply food to the doctors and their staff; such supplies, even when not charged, may be subjected to GST. |

Health care services provided by a clinical establishment, an authorised medical practitioner or para-medics are exempt. [Sl. No. 74 of notification No. 12/2017-CT(Rate) dated 28.06.2017 as amended refers].

(1) Services provided by senior doctors/ consultants/ technicians hired by the hospitals, whether employees or not, are healthcare services which are exempt. (2) Healthcare services have been defined to mean any service by way of diagnosis or treatment or care for illness, injury, deformity, abnormality or pregnancy in any recognised system of medicines in India[para 2(zg) of notification No. 12/2017-CT(Rate)]. Therefore, hospitals also provide healthcare services. The entire amount charged by them from the patients including the retention money and the fee/payments made to the doctors etc., is towards the healthcare services provided by the hospitals to the patients and is exempt. (3) Food supplied to the in-patients as advised by the doctor/nutritionists is a part of composite supply of healthcare and not separately taxable. Other supplies of food by a hospital to patients (not admitted) or their attendants or visitors are taxable. |

Taxability of Medicine

“Supply of service” which is not covered as per the above explained exemption, would be taxable under GST. As far as taxability of Medicine is concerned, some of the medicine supply is exempt while the rest of the supply of medicine is taxable under GST. Most of the medicines are taxed @ 5%, @ 12% and 18% ranges and depending upon the HSN of the medicines. Similarly, consumables / injectables and implants are taxed as per applicable rate importantly, notification 1/2017- Central Tax (Rate) dated 28th June 2017 covers the taxable GST rates applicable on the supply of medicines. Whereas, notification 2/2017- Central Tax (Rate) dated 28th June 2017 covers the exemption.

Conclusion

GST has significantly impacted the way the healthcare sector structures the costs of its services. Where citizens are being encouraged to have health insurance premium, Health insurance premium is getting costlier year by year and moreover GST has levied 18% on it resulting it becoming more expansive. The Healthcare Federation of India (NATHEALTH), in December2019, urged the government to bring a zero rating of Goods and Services for all healthcare services and health insurance premiums. The Federation raised the point that the net impact of GST on inputs consumed by hospitals has increased since healthcare service providers are ineligible to avail Input Tax Credit, healthcare services being non-taxable. This ultimately increases the cost of healthcare services on patients and defeats the objectives of GST that includes reducing the overall costs of goods and services for the end users. The CII also recommended a flat 5% rate of GST on healthcare service deliveries PAN-India. In the 47th meeting, the GST Council decided to levy 5% GST on hospital rooms (non-ICU) having daily room rent exceeding Rs. 5,000 but without input. The GST council should levy 5% GST on all billing but should allow GST Input on material and services a healthcare unit procures for day to day operation. It will also boost Health care Infrastructure and encourage investing more on infrastructural developments and bridging the resource gap.

Author Bio