The 52nd GST Council meeting was characterized by significant changes being made to the tax landscape in India. The Council, upholding the spirit of cooperative federalism, decided to cede the right to tax ENA for use in alcohol for human consumption to the States. Moreover, the GST on molasses has been reduced from 28% to 5%, benefiting sugarcane farmers and lowering cattle feed costs. A favorable shift has occurred in the tax rates for millet flour, which will give a fillip to millet consumption in the country as unpackaged millet flour with at least 70% millet content will now enjoy a zero percent tax rate, while packaged and labeled millet flour will be subject to a five percent tax rate. This is particularly significant as we celebrate the year 2023 as the International Year of Millets.

The Council has recommended to issue clarifications to clear ambiguity on taxability of personal guarantee offered by directors to the bank against the credit limits/loans being sanctioned to the company, corporate guarantee provided for related persons including corporate guarantee provided by holding company to its subsidiary company and on various issues related to place of supply.

The Central Government has notified comprehensive rules for Goods and Services Tax Appellate Tribunal (Appointment and Conditions of Service of President and Members) Rules, 2023. They encompass various provisions related to the appointment and removal of the President and Members, their salaries and allowances, as well as delineating their respective powers, including asset declarations and post-office restrictions. Notably, advocates with a minimum of 10 years of litigation experience in indirect tax law across various forums are also now eligible to become Judicial Members of the GSTAT. The various recommendations of the Council such as amnesty scheme for filing of appeals against demand orders in cases where appeal could not be filed within the allowable time period , admissibility of export remittances received in Special INR Vostro account as permitted by RBI for the purpose of consideration of supply of services to qualify as export of services under the IGST Act , conditional IGST exemption to foreign flag foreign going vessel when it converts to coastal run subject to its reconversion to foreign going vessel in six months, etc. herald a facilitative tax regime which promotes ease of doing business.

Pankaj Kumar Singh,

Additional Secretary

52nd GST Council Meeting

Recommendations of 52nd GST Council Meeting

The 52nd GST Council met under the Chairpersonship of Hon’ble Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman in New Delhi on 07.10.2023. The meeting was also attended by Hon’ble Union Minister of State for Finance Shri Pankaj Chaudhary, Hon’ble Chief Ministers of Goa and Meghalaya holding finance portfolio, besides Finance Ministers of States & UTs (with legislature) and senior officers of the Ministry of Finance & States/ UTs.

The GST Council inter-alia made the following recommendations relating to changes in GST tax rates, measures for facilitation of trade and measures for streamlining compliances in GST.

A. Recommendations relating to GST rates on goods and services

I. Changes in GST rates of goods

1. GST rates on “Food preparation of millet flour in powder form, containing at least 70% millets by weight”, falling under HS 1901, with effect from date of notification, have been prescribed as:

a. 0% if sold in other than pre-packaged and labelled form

b. 5% if sold in pre-packaged and labelled form

2. To clarify that imitation zari thread or yarn made out of metallised polyester film /plastic film, falling under HS 5605, are covered by the entry for imitation zari thread or yarn attracting 5% GST rate. However, no refund will be allowed on polyester film (metallised) /plastic film on account of inversion.

3. Foreign going vessels are liable to pay 5% IGST on the value of the vessel if it converts to coastal run. GST Council recommends conditional IGST exemption to foreign flag foreign going vessel when it converts to coastal run subject to its reconversion to foreign going vessel in six months.

II. Other changes relating to Goods

1. GST Council recommended to keep Extra Neutral Alcohol (ENA) used for manufacture of alcoholic liquor for human consumption outside GST. Law Committee will examine suitable amendment in law to exclude ENA for use in manufacture of alcoholic liquors for human consumption from ambit of GST.

2. To reduce GST on molasses from 28% to 5%. This step will increase liquidity with mills and enable faster clearance of cane dues to sugarcane farmers. This will also lead to reduction in cost for manufacture of cattle feed as molasses is also an ingredient in its manufacture.

3. A separate tariff HS code has been created at 8 digit level in the Customs Tariff Act to cover rectified spirit for industrial use. The GST rate notification will be amended to create an entry for ENA for industrial use attracting 18% GST.

III. Changes in GST rates of services

1. Entries at Sl. No. 3 and 3A of notification No. 12/2017-CTR dated 28.06.2017 exempts pure and composite services provided to Central/State/UT governments and local authorities in relation to any function entrusted to Panchayat/ Municipality under Article 243G and 243W of the Constitution of India. The GST Council has recommended to retain the existing exemption entries with no change.

2. Further, the GST Council has also recommended to exempt services of water supply, public health, sanitation conservancy, solid waste management and slum improvement and upgradation supplied to Governmental Authorities.

IV. Other changes relating to Services

1. To clarify that job work services for processing of barley into malt attracts GST @ 5% as applicable to “job work in relation to food and food products” and not 18%.

2. With effect from 1st January 2022, liability to pay GST on bus transportation services supplied through Electronic Commerce Operators (ECOs) has been placed on the ECO under section 9(5) of CGST Act, 2017. This trade facilitation measure was taken on the representation of industry association that most of the bus operators supplying service through ECO owned one or two buses and were not in a position to take registration and meet GST compliances. To arrive at a balance between the need of small operators for ease of doing business and the need of large organized players to take ITC, GST Council has recommended that bus operators organised as companies may be excluded from the purview of section 9(5) of CGST Act, 2017. This would enable them to pay GST on their supplies using their ITC.

3. To clarify that District Mineral Foundations Trusts (DMFT) set up by the State Governments across the country in mineral mining areas are Governmental Authorities and thus eligible for the same exemptions from GST as available to any other Governmental Authority.

4. Supply of all goods and services by Indian Railways shall be taxed under Forward Charge Mechanism to enable them to avail ITC. This will reduce the cost for Indian Railways.

B. Measures for facilitation of trade:

i) Amnesty Scheme for filing of appeals against demand orders in cases where appeal could not be filed within the allowable time period: The Council has recommended providing an amnesty scheme through a special procedure under section 148 of CGST Act, 2017 for taxable persons, who could not file an appeal under section 107 of the said Act, against the demand order under section 73 or 74 of CGST Act, 2017 passed on or before the 31st day of March, 2023, or whose appeal against the said order was rejected solely on the grounds that the said appeal was not filed within the time period specified in sub-section (1) of section 107. In all such cases, filing of appeal by the taxpayers will be allowed against such orders upto 31st January 2024, subject to the condition of payment of an amount of pre-deposit of 12.5% of the tax under dispute, out of which at least 20% (i.e. 2.5% of the tax under dispute) should be debited from Electronic Cash Ledger. This will facilitate a large number of taxpayers, who could not file appeal in the past within the specified time period.

(ii) Clarifications regarding taxability of personal guarantee offered by directors to the bank against the credit limits/loans being sanctioned to the company and regarding taxability of corporate guarantee provided for related persons including corporate guarantee provided by holding company to its subsidiary company: The Council has inter alia recommended to:

(a) issue a circular clarifying that when no consideration is paid by the company to the director in any form, directly or indirectly, for providing personal guarantee to the bank/ financial institutes on their behalf, the open market value of the said transaction/ supply may be treated as zero and hence, no tax to be payable in respect of such supply of services.

(b) to insert sub-rule (2) in Rule 28 of CGST Rules, 2017, to provide for taxable value of supply of corporate guarantee provided between related parties as one per cent of the amount of such guarantee offered, or the actual consideration, whichever is higher.

(c) to clarify through the circular that after the insertion of the said sub-rule, the value of such supply of services of corporate guarantee provided between related parties would be governed by the proposed sub-rule (2) of rule 28 of CGST Rules, 2017, irrespective of whether full ITC is available to the recipient of services or not.

(iii) Provision for automatic restoration of provisionally attached property after completion of one year:

The Council has recommended an amendment in sub-rule (2) of Rule 159 of CGST Rules, 2017 and FORM GST DRC-22 to provide that the order for provisional attachment in FORM GST DRC-22 shall not be valid after expiry of one year from the date of the said order. This will facilitate release of provisionally attached properties after expiry of period of one year, without need for separate specific written order from the Commissioner.

(iv) Clarification on various issues related to Place of Supply: The Council has recommended to issue a Circular to clarify the place of supply in respect of the following supply of services:

(i) Supply of service of transportation of goods, including by mail or courier, in cases where the location of supplier or the location of recipient of services is outside India;

(ii) Supply of advertising services;

(iii) Supply of the co-location services.

(v) Issuance of clarification relating to export of services-:

The Council has recommended to issue a circular to clarify the admissibility of export remittances received in Special INR Vostro account, as permitted by RBI, for the purpose of consideration of supply of services to qualify as export of services in terms of the provisions of sub-clause (iv) of clause (6) of section 2 of the IGST Act, 2017.

(vi) Allowing supplies to SEZ units/ developer for authorised operations for IGST refund route by amendment in Notification 01/2023-Integrated Tax dated 31.07.2023:

The Council has recommended to amend Notification 01/2023-Integrated Tax dated 31.07.2023 w.e.f. 01.10.2023 so as to allow the suppliers to a Special Economic Zone developer or a Special Economic Zone unit for authorised operations to make supply of goods or services (except the commodities like pan masala, tobacco, gutkha, etc. mentioned in the Notification 01/2023-Integrated Tax dated 31.07.2023) to the Special Economic Zone developer or the Special Economic Zone unit for authorised operations on payment of integrated tax and claim the refund of tax so paid.

C. Other measures pertaining to law and procedures:

i) Alignment of provisions of the CGST Act, 2017 with the provisions of the Tribunal Reforms Act, 2021 in respect of Appointment of President and Member of the proposed GST Appellate Tribunals: The Council has recommended amendments in section 110 of the CGST Act, 2017 to provide that:

- an advocate for ten years with substantial experience in litigation under indirect tax laws in the Appellate Tribunal, Central Excise and Service Tax Tribunal, State VAT Tribunals, by whatever name called, High Court or Supreme Court to be eligible for the appointment as judicial member;

- The minimum age for eligibility for appointment as President and Member to be 50 years;

- President and Members shall have tenure up to a maximum age of 70 years and 67 years respectively.

ii) Law amendment with respect to ISD as recommended by the GST Council in its 50th meeting: GST Council in its 50th meeting had recommended that ISD (Input Service Distributor) procedure as laid down in Section 20 of the CGST Act, 2017 may be made mandatory prospectively for distribution of ITC in respect of input services procured by Head Office (HO) from a third party but attributable to both HO and Branch Office (BO) or exclusively to one or more BOs. The Council has now recommended amendments in Section 2(61) and section 20 of CGST Act, 2017 as well amendment in rule 39 of CGST Rules, 2017 in respect of the same.

Source: PIB Press Release dated 07.10.2023

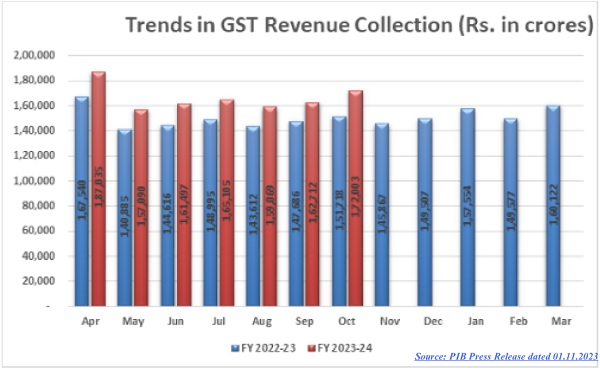

GST Revenue Collection

GST revenue collection for October 2023 is second highest ever, next only to April 2023, at ₹1.72 lakh crore; records increase of 13% Y-o-Y

The gross GST revenue collected in the month of October, 2023 is ₹ 1,72,003 crore out of which ₹ 30,062 crore is CGST, ₹ 38,171 crore is SGST, ₹ 91,315 crore (including ₹ 42,127 crore collected on import of goods) is IGST and ₹ 12,456 crore (including ₹ 1,294 crore collected on import of goods) is cess.

The government has settled ₹ 42,873 crore to CGST and ₹ 36,614 crore to SGST from IGST. The total revenue of Centre and the States in the month of October, 2023 after regular settlement is ₹72,934 crore for CGST and ₹ 74,785 crore for SGST.

The gross GST revenue for the month of October, 2023 is 13% higher than that in the same month last year. During the month, revenue from domestic transactions (including import of services) is also 13% higher than the revenues from these sources during the same month last year. The average gross monthly GST collection in the FY 2023-24 now stands at Rs. 1.66 lakh crore and is 11% per cent more than that in the same period in the previous financial year.

The chart below shows trends in monthly gross GST revenues during the current year:

Notifications

Notification No. 12/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend Notification No 11/2017- Central Tax (Rate) dated 28.06.2017

The Central Government vide the said Notification has amended the entry no. 8 and 10 related to passenger transport services and rental services of transport vehicles with operators respectively in Notification No 11/2017- Central Tax (Rate) dated 28.06.2017 to provide that if the supplier of an input service charges central tax at a rate higher than 2.5%, the credit of input tax charged on the input service in the same line of business in excess of the tax paid or payable at the rate of 2.5% will not be allowed.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 15/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 12/2023- Union Territory Tax (Rate) dated 19.10.2023 respectively.

Notification No. 13/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend notification No. 12/2017-CTR dated 28.06.2017

The Central Government vide the said Notification has inserted a new serial number 3B in notification No. 12/2017-CTR dated 28.06.2017, specifying services provided to Governmental Authorities i.e. water supply, public health, sanitation conservancy, solid waste management, and slum improvement and upgradation which have been exempted from GST. It also amends the entries at serial no. 6, 7, 8 and 9 to insert “and the Ministry of Railways (Indian Railways)” after the words “Department of Posts”. It shall come into force with effect from 20.10.2023.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 16/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 13/2023- Union Territory Tax (Rate) dated 19.10.2023 respectively.

Notification No. 14/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend Notification No 13/2017- Central Tax (Rate) dated 28.06.2017

The Central Government vide the said Notification has amended Notification No 13/2017- Central Tax (Rate) dated 28.06.2017 the entry at serial no. 5 and 5A so that supply of goods and services by Indian Railways shall be taxed under the Forward Charge Mechanism (FCM) and not Reverse Charge Mechanism to enable Indian Railways to avail ITC which would reduce the cost of Indian Railways. It shall come into force with effect from 20.10.2023.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 17/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 14/2023- Union Territory Tax (Rate) dated 19.10.2023 respectively.

Notification No. 15/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend Notification No 15/2017- Central Tax (Rate) dated 28.06.2017

The Central Government vide the said Notification has amended Notification No 15/2017- Central Tax (Rate) dated 28.06.2017 to specifically state that it pertains to the ‘construction of a complex, building, or a part thereof, intended for sale to a buyer.’ The change clarifies that no refund of unutilised input tax credit shall be allowed under sub-section (3) of section 54 of the CGST Act to such construction projects where the amount charged includes the value of land or an undivided share of land, except where the entire consideration is received after the issuance of a completion certificate or after the first occupation, whichever is earlier.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 18/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 15/2023- Union Territory Tax (Rate) dated 19.10.2023 respectively.

Notification No. 16/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend Notification No 17/2017- Central Tax (Rate) dated 28.06.2017

The Central Government vide the said Notification has amended Notification No 17/2017- Central Tax (Rate) dated 28.06.2017 to exclude bus operators organised as companies from the purview of section 9(5) of the CGST Act, 2017. It shall come into force with effect from 20.10.2023.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 19/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 16/2023- Union Territory Tax (Rate) dated 19.10.2023 respectively.

Notification No. 17/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend Notification No 1/2017- Central Tax (Rate) dated 28.06.2017

The Central Government vide the said Notification has amended Notification No 1/2017- Central Tax (Rate) dated 28.06.2017 to effect the following changes. GST rate on molasses has been reduced from 28% to 5% vide insertion of Sl. No. 92A in Schedule I of the said Notification and omission Sl. No. 1 of Schedule IV of the said Notification. Vide insertion of Sl. No. 25A and related entries in Schedule III in the said Notification spirit for industrial use will be taxed at 18%,

The GST rate on Food preparation of millet flour in powder form, containing at least 70% millets by weight, falling under HS 1901 if sold in pre-packaged and labelled form shall be now taxed at 5%. Sl. No. 96A has been inserted in Schedule I of the said Notification and Sl. No. 13 of Schedule III of the said Notification has been suitably amended to give effect to the same. It shall come into force with effect from 20.10.2023.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 20/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 17/2023 – Central Tax (Rate) dated 19.10.2023 respectively.

Notification No. 18/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend Notification No 2/2017- Central Tax (Rate) dated 28.06.2017

The Central Government vide the said Notification has amended Notification No 2/2017- Central Tax (Rate) dated 28.06.2017to insert Sl. No. 94A of the said Notification to tax “Food preparation of millet flour in powder form, containing at least 70% millets by weight”, falling under HS 1901, at 0% if sold in other than pre-packaged and labelled form. It shall come into force with effect from 20.10.2023.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 21/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 18/2023- Union Territory Tax (Rate) dated 19.10.2023 respectively.

Notification No. 19/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend Notification No 4/2017- Central Tax (Rate) dated 28.06.2017

The Central Government vide the said Notification has amended Notification No 4/2017- Central Tax (Rate) dated 28.06.2017 so that supply of goods and services by Indian Railways shall be taxed under the Forward Charge Mechanism (FCM) to enable Indian Railways to avail ITC which would reduce the cost of Indian Railways. It shall come into force with effect from 20.10.2023.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 22/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 19/2023- Union Territory Tax (Rate) dated 19.10.2023 respectively.

Notification No. 20/2023 – Central Tax (Rate) dated 19.10.2023 seeks to amend Notification No 5/2017- Central Tax (Rate) dated 28.06.2017

The Council has clarified that imitation zari thread or yarn made out of metallised polyester film /plastic film, falling under HS 5605, are covered by the entry for imitation zari thread or yarn attracting 5% GST rate. However, no refund will be allowed on polyester film (metallised) /plastic film on account of inversion. The Central Government vide the said Notification has amended Notification No 5/2017- Central Tax (Rate) dated 28.06.2017and inserted the S. No. 6AA after S. No. 6A in the said Notification to include imitation zari thread or yarn made out of Metallised polyester film /plastic film in the list of goods for which no refund shall be allowed on account of inversion. It shall come into force with effect from 20.10.2023.

Similar notifications have been passed under the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) and the Union Territory Goods and Services Tax Act, 2017 (“the UTGST Act”) under Notification No. 23/2023- Integrated Tax (Rate) dated 19.10.2023 and Notification No. 20/2023- Union Territory Tax (Rate) dated 19.10.2023 respectively.

Notification No. 52/2023 – Central Tax dated 26.10.2023 seeks to make amendments (Fourth Amendment, 2023) to the CGST Rules, 2017

The Central Government vide the said Notification has issued Central Goods and Services Tax (Fourth Amendment) Rules, 2023 to interalia amend aforesaid Rules and Forms:

i.Rule 28: It has re numbered Rule 28 as sub rule 1 and further inserted sub-rule (2) in Rule 28 of the Central Goods and Services Tax Rules, 2017 (“the CGST Rules”) to provide for taxable value of supply of corporate guarantee provided between related parties as one percent of the amount of such guarantee offered, or the actual consideration, whichever is higher notwithstanding anything contained in sub rule 1.

ii. Rule 142: In sub-rule (3), for the words “proper officer shall issue an order”, the words “proper officer shall issue an intimation” shall be substituted.

iii. Rule 159 and FORM GST DRC-22: In the said rules, in rule 159, in sub-rule (2), after the words “Commissioner to that effect”, the words “or on expiry of a period of one year from the date of issuance of order under sub-rule (1), whichever is earlier,” shall be inserted. FORM GST DRC 22 has also been suitably amended to provide that provisional attachment of property shall cease to have effect, on the date of issuance of order in FORM GST DRC 23 by the Commissioner, or on the expiry of a period of one year from the date of issuance of the order, whichever is earlier

iv. In FORM GST PCT-01 and FORM GST REG-08 certain amendments have been done. In FORM GST REG-01, the clause “(xiva) One Person Company” is inserted in PART-B, in serial number 2, after clause (xiv).

Notification No. 5/2023 – Integrated Tax dated 26.10.2023 seeks to notify supplies and class of registered person eligible for refund under IGST Route

The Central Government vide the said Notification has amended Notification No. 1/2023-Integrated Tax dated 31.07.2023 w.e.f. 01.10.2023 so as to allow the suppliers of Special Economic Zone developer or unit, for authorised operations to make supply of goods or services (except the commodities like pan masala, tobacco, gutkha, etc. mentioned in the Notification No. 1/2023-Integrated Tax dated 31.07.2023) to the Special Economic Zone Developer or Unit for authorised operations on payment of integrated tax and claim the refund of tax so paid.

Circulars

Circular No. 202/14/2023-GST dated 27.10.2023 regarding clarification relating to export of services – sub-clause (iv) of the Section 2 (6) of the IGST Act 2017

The Central Government vide the said Circular has clarified that when the Indian exporters, undertaking export of services, are paid the export proceeds in INR from the Special Rupee Vostro Accounts of correspondent bank(s) of the partner trading country, opened by AD banks, the same shall be considered to be fulfilling the conditions of sub-clause (iv) of clause (6) of section 2 of IGST Act, 2017, subject to the conditions/ restrictions mentioned in Foreign Trade Policy,2023 &extant RBI Circulars and without prejudice to the permissions / approvals, if any, required under any other law.

Circular No. 203/15/2023-GST dated 27.10.2023 regarding clarification regarding determination of place of supply in various cases

The Central Government vide the said Circular has clarified the following:

i. supply of service of transportation of goods, including through mail and courier: Sub-section (9) of section 13 of IGST Act has been omitted vide section 162 of Finance Act, 2023 which will come into effect from 01.10.2023. After the said amendment, certain doubts have been raised. It is clarified through the said Circular that after the said amendment comes into effect, the place of supply of services of transportation of goods, other than through mail and courier, in cases where location of supplier of services or location of recipient of services is outside India, will be determined by the default rule under section 13(2) of IGST Act and not as performance based services under sub-section (3) of section 13 of IGST Act. Accordingly, in cases where location of recipient of services is available, the place of supply of such services shall be the location of recipient of services and in cases where location of recipient of services is not available in the ordinary course of business, the place of supply shall be the location of supplier of services. It is also clarified that the place of supply in case of service of transportation of goods by mail or courier will continue to be determined by the default rule under section 13(2) of IGST Act as it was not covered under the provisions of sub-section (9) of section 13 before the said sub-section was amended/omitted.

ii. supply of services in respect of advertising sector:

It is clarified that the place of supply of service in a case wherein there is supply (sale) of space or supply (sale) of rights to use the space on the hoarding/ structure (immovable property) belonging to vendor to the client/advertising company for display of their advertisement on the said hoarding/ structure would be the location where such hoarding/ structure is located.

In case where the advertising company wants to display its advertisement on hoardings/ bill boards at a specific location availing the services of a vendor and the responsibility of arranging the hoardings/ bill boards lies with the vendor who may himself own such structure or may be taking it on rent or rights to use basis from another person. The vendor is responsible for display of the advertisement of the advertisement company at the said location. During this entire time of display of the advertisement, the vendor is in possession of the hoarding/structure at the said location on which advertisement is displayed and the advertising company is not occupying the space or the structure. It is clarified that in such cases services provided by the Vendor to advertising company are purely in the nature of advertisement services in respect of which Place of Supply shall be determined in terms of Section 12(2) of IGST Act.

iii. Place of supply in case of supply of the “co-location services”:

It is clarified that the Co-location services are in the nature of “Hosting and information technology (IT) infrastructure provisioning services (S.No. 3 of Explanatory notes of SAC-998315). In such cases, supply of colocation services cannot be considered as the services of supply of renting of immovable property. Therefore, the place of supply of the colocation services shall not be determined by the provisions of clause (a) of sub-section (3) of Section 12 of the IGST Act but the same shall be determined by the default place of supply provision under sub-section (2) of Section 12 of the IGST Act i.e. location of recipient of co-location service.

Furthermore, it is clarified that in cases where the agreement between the supplier and the recipient is restricted to providing physical space on rent along with basic infrastructure, without component of Hosting and Information Technology (IT) Infrastructure Provisioning services and the further responsibility of upkeep, running, monitoring and surveillance, etc. of the servers and related hardware is of recipient of services only, then the said supply of services shall be considered as the supply of the service of renting of immovable property. Accordingly, the place of supply of these services shall be determined by the provisions of clause (a) of sub-section (3) of Section 12 of the IGST Act which is the location where the immovable property is located.

Circular No. 204/16/2023-GST dated 27.10.2023 regarding clarification on issues pertaining to taxability of personal guarantee and corporate guarantee in GST

The activity of providing personal guarantee by the director to the banks/ financial institutions for securing credit facilities for their companies is to be treated as a supply of service, even when made without consideration as the director and the company are to be treated as related persons as per Explanation (a) to section 15 of CGST Act. Rule 28 of Central Goods and Services Tax Rules, 2017 prescribes the method for determining the value of the supply of goods or services or both between related parties, other than where the supply is made through an agent. In terms of Rule 28 of CGST Rules, the taxable value of such supply of service shall be the open market value of such supply. The Central Government vide the said Circular has clarified that when no consideration by way of commission, brokerage fees or any other form, can be paid to its director by the company, directly or indirectly, in lieu of providing personal guarantee to the bank for borrowing credit limits as per RBI mandate, there is no question of such supply/transaction having any open market value. Accordingly, the open market value of the said transaction/ supply may be treated as zero and therefore, taxable value of such supply may be treated as zero. In such a scenario, no tax is payable on such supply of service by the director to the company.

It is also clarified that, however, there may be cases where the director, who had provided the guarantee, is no longer connected with the management but continuance of his guarantee is considered essential because the new management’s guarantee is either not available or is found inadequate, or there may be other exceptional cases where the promoters, existing directors, other managerial personnel, and shareholders of borrowing concerns are paid remuneration/ consideration in any manner, directly or indirectly. In all these cases, the taxable value of such supply of service shall be the remuneration/ consideration provided to such a person/ guarantor by the company, directly or indirectly.

It is also clarified that where the corporate guarantee is provided by a holding company, for its subsidiary company, those two entities also fall under the category of ‘related persons’. Hence the activity of providing corporate guarantee by a holding company to the bank/financial institutions for securing credit facilities for its subsidiary company, even when made without any consideration, is also to be treated as a supply of service. In respect of such supply of services by a person to another related person or by a holding company to a subsidiary company, in form of providing corporate guarantee on their behalf to a bank/ financial institution, the taxable value will be determined as per the newly inserted sub rule (2 ) of Rule 28 of CGST Rules.

Circular No. 205/17/2023-GST dated 31.10.2023 regarding clarification regarding GST rate on imitation zari thread or yarn based on the recommendation of the GST Council in its 52nd meeting held on 7th October, 2023

The Central Government vide the said Circular has clarified that imitation zari thread or yarn made from metallised polyester film/ plastic film falling under HS 5605 are covered by Sl. No. 218AA of Schedule I attracting 5% GST. The GST Council has also recommended that no refund will be permitted on polyester film (metallised)/plastic film on account of inversion of tax rate. Requisite changes have been made in Notification No. 5/2017-Central Tax (Rate) vide Notification No. 20/2023-Central Tax (Rate) dated 19.10.2023.

Circular No. 206/18/2023-GST dated 31.10.2023 regarding clarification regarding applicability of GST on certain services

i. Whether ‘same line of business’ in case of passenger transport service and renting of motor vehicles includes leasing of motor vehicles without operators:

It is clarified that input services in the same line of business include transport of passengers (SAC 9964) or renting of motor vehicle with operator (SAC 9966) and not leasing of motor vehicles without operator (SAC 9973) which attracts GST and/or compensation cess at the same rate as supply of motor vehicles by way of sale.

ii. Whether GST is applicable on reimbursement of electricity charges received by real estate companies, malls, airport operators etc. from their lessees/occupants:

It is clarified that whenever electricity is being supplied bundled with renting of immovable property and/or maintenance of premises, as the case may be, it forms a part of composite supply and shall be taxed accordingly. The principal supply is renting of immovable property and/or maintenance of premise, as the case may be, and the supply of electricity is an ancillary supply as the case may be. Even if electricity is billed separately, the supplies will constitute a composite supply and therefore, the rate of the principal supply i.e., GST rate on renting of immovable property and/or maintenance of premise, as the case may be, would be applicable.

It is further clarified that where the electricity is supplied by the Real Estate Owners, Resident Welfare Associations (RWAs), Real Estate Developers etc., as a pure agent, it will not form part of value of their supply. Further, where they charge for electricity on actual basis that is, they charge the same amount for electricity from their lessees or occupants as charged by the State Electricity Boards or DISCOMs from them, they will be deemed to be acting as pure agent for this supply.

iii. Whether job work for processing of “Barley” into “Malted Barley” attracts GST @ 5% as applicable to “job work in relation to food and food products” or 18% as applicable on “job work in relation to manufacture of alcoholic liquor for human consumption”:

It is clarified that job work services in relation to manufacture of malt are covered by the entry at Sl. No. 26 (i) (f) which covers “job work in relation to all food and food products falling under chapters 1 to 22 of the customs tariff” irrespective of the end use of that malt and attracts 5% GST.

iv. Whether District Mineral Foundations Trusts (DMFTs) set up by the State Governments are Governmental Authorities and thus eligible for the same exemptions from GST as available to any other Governmental Authority:

It is clarified that DMFT set up by the State Governments are Governmental Authorities and thus eligible for the same exemptions from GST as available to any other Governmental Authority.

v. Whether supply of pure services and composite supplies by way of horticulture/horticulture works(where the value of goods constitutes not more than 25 per cent of the total value of supply) made to CPWD are eligible for exemption from GST under Sr. No. 3 and 3A of Notification no 12/2017-CTR dated 28.06.2017:

It is clarified that supply of pure services and composite supplies by way of horticulture/horticulture works(where the value of goods constitutes not more than 25 per cent of the total value of supply) made to CPWD are eligible for exemption from GST under Sr. No. 3 and 3A of Notification no 12/2017-CTR dated 28.06.2017.

GST Portal Updates

Advisory: e-Invoice JSON download functionality Live on the GST e-Invoice Portal

The e-Invoice JSON download functionality is now live on the GST Portal. To help to navigate and make the most of this feature, some key steps are provided in the advisory (link below). Moreover, please note that this functionality is also accessible via GSP (GST Suvidha Providers) through G2B (Government-to-Business) APIs.

Portal update on 03.10.2023

Advisory: Facility for the e- commerce operators through whom unregistered suppliers of goods can supply goods

GSTN has provided APIs for ECOs (through whom unregistered persons can supply goods) to integrate with GSTN to obtain the details and facilitate the unregistered suppliers. The APIs are for validating the demographic details of the said suppliers and also for use in tracking and reporting supplies by such persons. The details of the APIs are provided in the link below.

Portal update on 12.10.2023

Advisory: Facility of enrolment for supply of goods through e-commerce operators by GST un-registered suppliers

In terms of the recent amendments to the Act and the rules and Notification No. 34/2023 dated 31.07.2023, persons supplying goods through e-commerce operators shall be exempt from mandatory registration under the CGST Act even if they supply goods through e-commerce operators (ECO), if they satisfy certain specified conditions. GSTN has developed the necessary functionality for enrolment of unregistered persons and the same is available on the portal. Accordingly, unregistered person desirous of enrolling on the GST portal for making supplies of goods through ECOs in any one State/UT are advised to follow the path/procedure specified in the advisory as detailed in the link provided.

Portal update on 12.10.2023

Advisory: Person supplying of Online Money Gaming services or OIDAR or Both– Form GST REG-10 and Form GSTR-5A

In terms of the recent amendments made in the CGST/SGST Act, the IGST Act and the CGST/SGST Rules, any person located outside taxable territory making supply of online money gaming to a person in taxable territory, is liable to get registered in GST and is required to pay tax on such supply. In this context, every person located outside taxable territory making such supplies of online money gaming to a person in India is now mandated to take registration/amend his existing registration in accordance with the proposed Row (ii a) in FORM GST REG-10 and also required to furnish information regarding the supplies in the proposed Tables in FORM GSTR-5A. GSTN is in the process of developing the functionality of such new registrations or required amendment in existing registration, as the case may be. In the meantime, till the said functionality is made available on the portal, a workaround is suggested in the advisory as detailed in the link provided.

Portal update on 17.10.2023

Advisory related to changes in GSTR-5A

Notification 51/2023 dated 29.09.2023 has introduced Table 5B in GSTR 5A w. e. f 01.10.2023. In this notification, Table 5B has been introduced to report supplies made to Registered GSTINs (B2B supplies). This would be implemented shortly at GSTN and till such time, OIDARs are advised to file the return in the existing GSTR 5A itself.

Portal update on 27.10.2023

Best Practices Across India

First meeting of State Co-ordination Committee constituted for Haryana State by CGST Zone Panchkula and commencement of ‘Vigilance Awareness Week’ in CGST Panchkula Commissionerate

First meeting of State Co-ordination Committee constituted for Haryana State by CGST Zone Panchkula was held on 27.10.23. It was chaired by Sh. Upender Gupta, Chief Commr., Panchkula Zone & Sh. Ashok Meena, Commr., SGST, Haryana jointly and was attended by other senior officers.

Vigilance Awareness Week kickstarts in CGST Panchkula Commissionerate from 30.10.2023. Integrity Pledge was taken by the officers, under the guidance of Sh. Upender Gupta, IRS, Chief Commissioner, CGST Zone, Panchkula.

GST workshop was organised for travel agents, tour operators, hotel, homestay and restaurant owners at Kohima

An interactive GST workshop was organised for travel agents, tour operators, hotel, homestay and restaurant owners at Kohima to educate businesses in the tourism industry on how GST applies to their business as Nagaland gears up for the Hornbill Festival 2023. During these workshops, participants gain insights into GST regulations, compliance, and best practices, helping them navigate the complexities of taxation.

Legal Corner

Ratio decidendi

Ratio decidendi, a Latin term signifying “reason for deciding,” holds a central position within the legal realm. In the context of judicial decisions, it denotes the fundamental rationale or legal principle invoked by a court as the foundation for its verdict in a particular case. This rationale forms the bedrock for comprehending the court’s decision and provides a doctrinal framework to govern analogous cases in the future.

It is imperative to emphasize that the ratio decidendi does not constitute the law per se; rather, it encapsulates the underlying legal principle or logic that underpins a specific judgment. This distinction is of paramount significance, as it underscores that a court’s decision in a given case may not be universally applicable to all subsequent cases with akin legal issues. It is the ratio decidendi that mandates adherence in subsequent cases, not the broader or more general remarks or commentary made by the presiding judge.

In the event of disputes arising from the rationale articulated in a judgment, the crux of the matter pertains primarily to questions of law, as opposed to factual disputes. Given that the facts of distinct cases are unlikely to be carbon copies of one another, the particular factual findings arrived at by a judge in one case do not entail binding implications for other cases, even if analogous legal principles are invoked. Nevertheless, the legal reasoning, or ratio decidendi, that led to the verdict is obligatory and should be applied consistently in analogous cases.

In synthesis, ratio decidendi constitutes a pivotal doctrine within the precincts of legal precedent. It represents the legal rationale underpinning a court’s judgment and forms the benchmark to which other courts must adhere in comparable cases. While the specific factual elements of a case may diverge, the legal principles enshrined within the ratio decidendi serve as a guiding precedent for the uniform application of the law in subsequent cases.

Source of Newsletter – https://gstcouncil.gov.in/