The GST Council at its 24th meeting held on 16th December’2017 on an urgent meeting through video conferencing to discuss implementation of e-way bill system under the Goods and Services Tax (GST) regime approved Mandatory Compliance of e-Way Bill.

After review of the status of the hardware and software framework required for implementation of the e-way bill system and in consultation with the states, GST council recommended following :

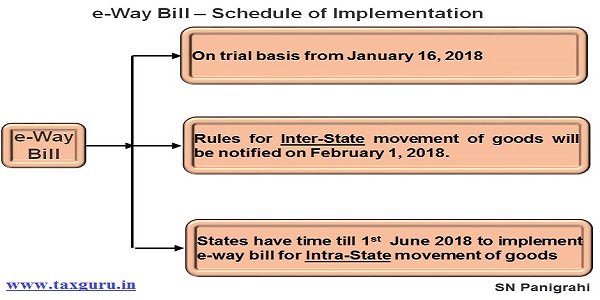

- Nationwide e-way bill system will be available on trial basis from January 16, 2018 for traders and transporters to use voluntarily.

- The Rules governing the compulsory implementation of the e-way bill system across India for Inter-State movement of goods will be notified on February 1, 2018.

- States have time till 1 June to implement the national e-way bill system for Intra-State goods movement.

- Mandatory Compliance of e-way bill for intra-state movement of goods from 1 June 2018. While the system for both inter-state and intra-state e-way Bill generation will be ready by January 16, the states may choose their own timings for implementation of e-way Bill for intra-state movement of goods on any date before June 1, 2018

What is E-Way Bill

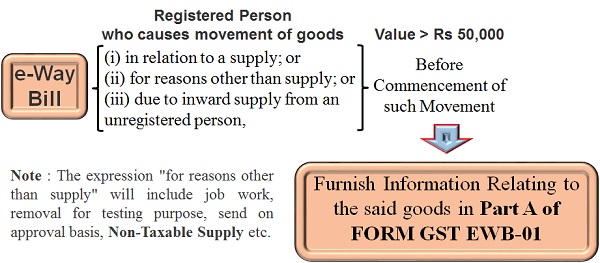

Under the GST regime, Electronic Way Bills (E-way Bills) will be the primary document for transportation of the goods. e-way bill is a document required to be carried by a person in charge of the conveyance carrying any consignment of goods of value exceeding fifty thousand rupees as mandated by the Government in terms of Section 68 of the Goods and Services Tax Act read with Rule 138 of the rules framed thereunder. It is generated from the GST Common Portal by the registered persons or transporters who causes movement of goods of consignment before commencement of such movement. An e-way bill is required for movement of goods worth more than Rs 50,000.

Why E- Way Bill

E-Way Bill will be meant to bring uniformity across states for seamless inter-state movement of goods.

Implementation of this system could lead to significant supply chain de-bottlenecking to reduce transaction time and other compliance related issues.

The mechanism will help the tax authorities monitor inter-state and intra-state movement of goods

22 states have abolished border commercial tax check posts. Many states have also issued advisories to field to not stop trucks. This move will allow seamless movement of goods across the border, ending waiting hours for commercial vehicles. Seamless transport is expected to cut transport costs which will help make goods cheaper. E-Way Bill provides authenticity of movement of goods.

The e-way bill mechanism has been introduced in the GST regime to plug tax evasion loopholes. Tax evasion was one of the reasons cited by the government for the fall in revenue collection in October.

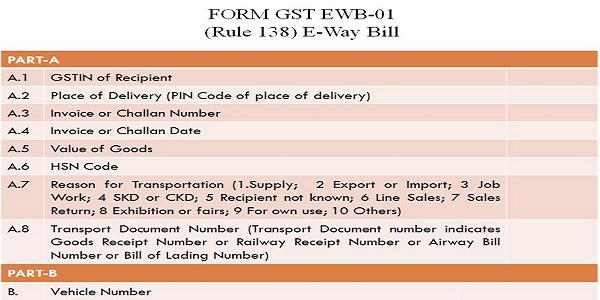

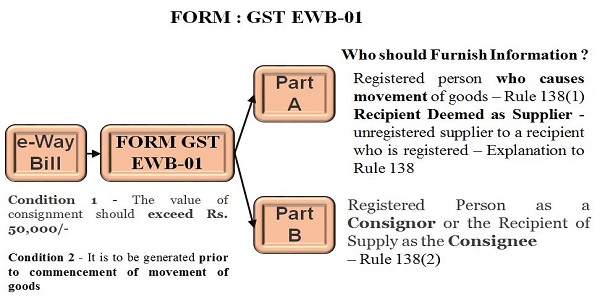

E- Way Bill Has Two Parts:

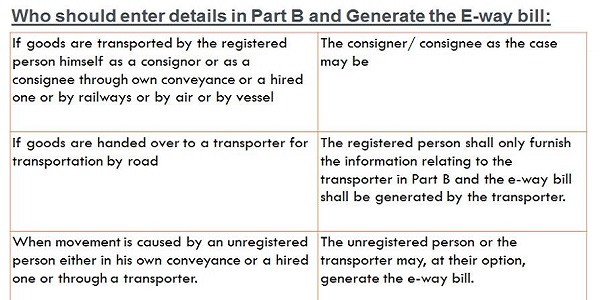

Who Should Furnish E-Way Bill

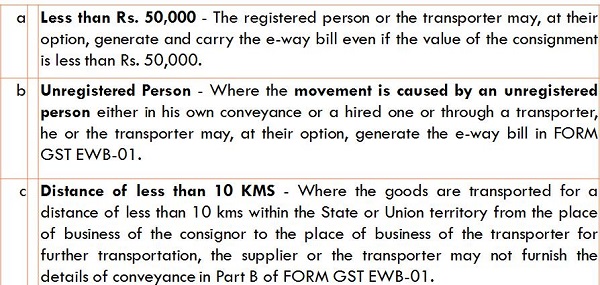

Optional E-Way Bill

In following transactions, the generation of e-way bill is optional:

When E-Way Bill not Required:

Rule 138(14)

Notwithstanding anything contained in this rule, no e-way bill is required to be generated—

(a) where the goods being transported are specified in Annexure;

(b) where the goods are being transported by a non-motorised Conveyance;

(c) where the goods are being transported from the port, airport, air cargo complex and land customs station to an inland container depot or a container freight station for clearance by Customs; and

(d) in respect of movement of goods within such areas as are notified under clause (d) of sub-rule (14) of rule 138 of the Goods and Services Tax Rules of the concerned State.

Rule 138(7) -Transporter May Generate FORM GST EWB-01

Where the consignor or the consignee has not generated FORM GST EWB-01 in accordance with the provisions of sub-rule (1) and the value of goods carried in the conveyance is more than fifty thousand rupees, the transporter shall generate FORM GST EWB-01 on the basis of invoice or bill of supply or delivery challan, as the case may be, and may also generate a consolidated e-way bill in FORM GST EWB-02 on the common portal prior to the movement of goods.

Rule 138(8) – Information Available on Portal

The information furnished in Part A of FORM GST EWB-01 shall be made available to the registered supplier on the common portal who may utilize the same for furnishing details in FORM GSTR-1

If goods not Transported as per e-Way Bill Generated

Rule 138(9)

Where an e-way bill has been generated under this rule, but goods are either not transported or are not transported as per the details furnished in the e-way bill, the e-way bill may be cancelled electronically on the common portal, either directly or through a Facilitation Centre notified by the Commissioner, within 24 hours of generation of the eway bill:

Provided that an e-way bill cannot be cancelled if it has been verified in transit in accordance with the provisions of rule 138B.

Validity of e-way bill

Rule 138(10) An e-way bill or a consolidated e-way bill generated under this rule shall be valid for the period as mentioned below :

i. Upto 100 Km – 1 day

ii. For every 100 km or part thereof thereafter – One additional day

The period of validity shall be counted from the time at which the e-way bill has been generated and each day shall be counted as twenty four hours.

EBN Number: Upon generation of e-way bill on the common portal, a unique e-way bill number (EBN) shall be made available to the supplier, the recipient and the transporter on the common portal – Rule 138(11)

Acceptance or rejection of e-way bill: The details of e-way bill generated shall be made available to the recipient, if registered who shall communicate his acceptance or rejection of the consignment. Where no communication is made within 72 hours, then it shall be deemed that he has accepted the said details – Rule 138(12)

The e-way bill generated under this rule or under rule 138 of the Goods and Services Tax Rules of any State shall be valid in every State and Union territory – Rule 138(13)

Rule 138(5) – Transferring goods in transit: If a transporter is transferring goods from one conveyance to another in the course of transit then he shall update the details of conveyance in the e-way bill before such transfer and further movement of goods. Rule 138(6) – Multiple consignments: If multiple consignments are intended to be transported in one conveyance, then the transporter may indicate the serial number of e-way bills of each consignment and a consolidated e-way bill may be generated by him prior to the movement of goods.

FORM GST EWB-02 : Consolidated E-Way Bill

Supply by unregistered person:

In case of supply by an unregistered person to a registered recipient, then the movement shall be said to be caused by registered recipient if such recipient is known at the time of commencement of the movement of goods.

Exceptional circumstances:

If goods cannot be transported within the validity period of the e-way bill due to circumstances of an exceptional nature, then the transporter may generate another e-way bill after updating the details in Part B.

Author Bio