Introduction

The term “Classification” is defined as systematic arrangement in groups or categories according to established criteria. Under the given concept, the arrangement of varied items is into mutually exclusive but related classes.

Under the Indirect Tax regimes prevalent across the Globe including India, the classification of various items which are the subject matter of tax, be it goods or services, is an essential and integral part of the whole levy and collection mechanism. It is important both from the taxpayer’s perspective and tax collector’s perspective to have a definite class or group under which subject matters of tax can be divided.

Importance

1. Leviability of tax

2. Goods vs services

3. Exemptions

4. Rate of tax

5. Standardization

Steps

1. Definition of ‘Goods’ and ‘Services’.

2. Activities listed in Schedule-II.

3. Activities listed in Schedule-III.

4. Identification of Composite Supplies or Mixed Supplies.

5. Identification of HSN Code from the rate notification.

6. Applicability of Principles of Interpretation applicable on Customs Tariff Act 1975 now made applicable vide Notification No 01/2017-CT (Rate) dated 28.06.2017.

7. Understanding the Service Code (Tariff) applicable on services in accordance with Annexure to Notification No 11/2017-CT (Rate) dated 28.06.2017.

Goods and Services

(52) “goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply;

(102) “services” means anything other than goods, money and securities but includes activities relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged;

Schedule II

1. Any transfer of title in Goods

2. Any transfer of title in goods under an agreement which stipulates that property in goods shall pass at a future date upon payment of full consideration as agreed

3. Goods forming part of the assets of a business transferred or disposed of by or under the directions of the person carrying on the business so as no longer to form part of those assets, whether or not for a consideration.

4. When any person ceases to be a taxable person, any goods forming part of the assets of any business carried on by him shall be deemed to be supplied by him in the course or furtherance of his business immediately before he ceases to be a taxable person, unless: (a) the business is transferred as a going concern to another person; or (b) the business is carried on by a personal representative who is deemed to be taxable

5. Supply of goods by any unincorporated association or body of persons to a member thereof for cash, deferred payment or other valuable consideration.

Schedule III

1. Services by an employee to the employer in the course of or in relation to his employment.

2. Services by any court or Tribunal established under any law for the time being in force.

3. The functions performed by the Members of Parliament, Members of State Legislature, Members of Panchayats, Members of Municipalities and Members of other local authorities.

4. The duties performed by any person who holds any post in pursuance of the provisions of the Constitution in that capacity

5. The duties performed by any person as a Chairperson or a Member or a Director in a body established by the Central Government or a State Government or local authority and who is not deemed as an employee before the commencement of this clause.

6. Services of funeral, burial, crematorium or mortuary including transportation of the deceased.

7. Sale of land and sale of building (completed).

8. Actionable claims, other than lottery, betting and gambling.

Mixed Vs Composite Supply

(30) “composite supply” means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply;

(90) “principal supply” means the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary;

(74) “mixed supply” means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply.

“8. Tax liability on composite and mixed supplies. — The tax liability on a composite or a mixed supply shall be determined in the following manner, namely:—

(a) a composite supply comprising two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply; and

(b) a mixed supply comprising two or more supplies shall be treated as a supply of that particular supply which attracts the highest rate of tax.

Independent Supply

Interestingly, in many cases when two or more supplies are made together, then there can be a possibility that such supplies are neither composite nor mixed but are two independent supplies which happen at the same time or same occasion. It is important not to feel compelled, when more than one supplies are made at the same time or same occasion, to forcible fit them into composite-mixed supply. In such cases, the classification of such supplies shall be determined based on their individual characteristics.

Taxable vs Exempt Supply

According to Section 2(108) of the CGST Act, 2017, the term taxable supply is defined as “a supply of goods or services or both which is leviable to tax under this Act”;

Further the term ‘exempt supply’ is defined under Section 2(47) of the Act thus: (47) “exempt supply” means supply of any goods or services or both which attracts nil rate of tax or which may be wholly exempt from tax under section 11, or under section 6 of the Integrated Goods and Services Tax Act, and includes non-taxable supply.

Notifications Number 01/2017-CT (Rate) dated 28.06.2017

This Notification is divided into 6 Schedules, as follows:

- 5% (Schedule I);

- 6% (Schedule II);

- 9% (Schedule III);

- 14% (Schedule IV);

- 5% (Schedule V); and

- 125% (Schedule VI)

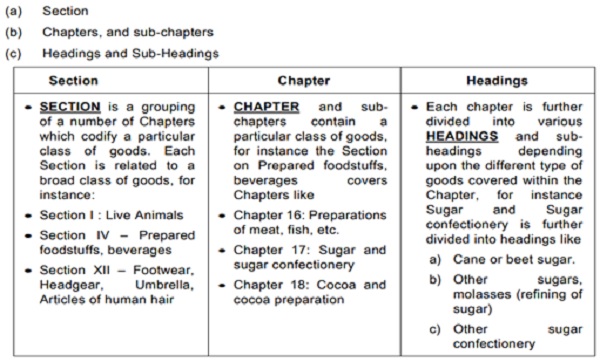

Harmonized System of Nomenclature (“HSN”)

(a) Adopted by 137 countries to ensure uniformity in classification of products;

(b) Contains about 5,000 commodity groups – each identified by a 6-digit code (it is pertinent to note that both the Tariff in India follow an 8 digit code system for further clarity in trade volumes and a more specific classification of indigenous products);

(c) Amended over regular intervals of 4/6 years, taking into consideration the technological advancements in any field – last amendment approved by the WCO in 2009, and brought into force with effect from 1-1-2012;

(d) For ensuring uniformity, WCO has published the Explanatory Notes to various headings/ sub- headings;

(e) The Customs Tariff in India was aligned to the HSN w.e.f. 28.02.1986 (whereas the Excise tariff was aligned w.e.f. 1-3-1986).

Searching HSN Code on CBIC website

Search facility is available on website. The search can be on basis of technical description as well as description through trade or commercial description. It is available at pre-login and post-login. Go to Home> Services> User Services > Search HSN Code. The search is based on Artificial Intelligence and Machine language linked with e-invoice declaration data base – https://www.gst.gov.in dated 6-1-2022.

Overview of HSN

- Animal Products (Section I – Chapters 1 to 6)

- Vegetable Products (Section II – Chapters 6 to 14)

- Animal or vegetable fats and oils (Section III – Chapter 15)

- Prepared foodstuffs, beverages (Section IV – Chapters 16 to 24)

- Mineral Products (Section V – Chapters 25 to 27)

- Products of Chemicals and allied industries (Section VI – Chapters 28 to 38)

- Plastics and Rubber and their articles (Section VII – Chapters 39 and 40)

- Raw hides and Skins, Leather and articles (Section VIII – Chapters 41 to 43)

- Wood, cork, straw and their articles (Section IX – Chapters 44 and 46)

- Pulp of wood, Paper, Paper-board and articles (Section X – Chapters 47 to 49)

- Textile and Textile Products (Section XI – Chapters 50 to 63)

- Footwear, Headgear, Umbrellas, Articles of human hair (Section XII – Chapters 64 to67).

- Articles of stone, plaster, ceramic, mica, glass (Section XIII – Chapters 68 to 70)

- Pearls, precious metals (Section XIV – Chapter 71)

- Base metals and articles of base metal (Iron, Steel, Copper, Nickel, Zinc, Tin etc.).

(Section XV – Chapters 72 to 83)

- Machinery and mechanical appliances, electrical equipments, television etc. (Section XVI

- – Chapters 84 and 85)

- Vehicles, Aircrafts, vessels and associated transport equipment (Section XVII – Chapters86 to 89)

- Optical, photographic, medical, surgical instruments, clocks, musical instruments

- (Section XVIII – Chapters 90 to 92)

- Arms and Ammunition (Section XIX – Chapter 93)

- Manufactured articles like Furniture, toys etc. (Section XX – Chapters 94 to 96)

- Works of Art, collectors’ pieces and antiques (Section XXI – Chapters 97 to 98).

GENERAL INTERPRETIVE RULES

- The titles of Sections and Chapters are provided for ease of reference only; for legal purposes, refer the heading and sub-heading. Read corresponding Section Notes and Chapter Notes (Rule 1 of GIR). If there is no ambiguity or confusion, the classification is final. You do not have to look to classification rules or trade practice or dictionary meaning. If classification is not possible, then only go to GIR. The rules are to be applied sequentially.

- If meaning of word is not clear, refer to trade practice. If trade understanding of a product cannot be established, find technical or dictionary meaning of the term used in the tariff. You may also refer to BIS or other standards, but trade parlance is most important.

- If goods are incomplete or unfinished, but classification of finished product is known, find if the unfinished item has essential characteristics of finished goods. If so, classify in same heading – Rule 2(a).

- If ambiguity persists, find out which heading is specific and which heading is more general. Prefer specific heading.- Rule 3(a).

- If problem is not resolved by Rule 3(a), find which material or component is giving ‘essential character’ to the goods in question – Rule 3(b).

- If both are equally specific, find which comes last in the Tariff and take it – Rule 3(c).

- If you are unable to find any entry which matches the goods in question, find goods which are most akin – Rule 4.

- In case of mixtures or sets too, the procedure is more or less same, except that each ingredient of the mixture or set has to be seen in above sequence. As per rule 2(b), any reference to a material or substance includes a reference to mixtures or combinations of that material or substance with other material or substance.

- Packing material is classified along with the goods except when the packing is for repetitive use – Rule 5.

Trade Parlance Theory

Since the primary objective of the Excise Act is to raise revenue, resort should not be had, for purpose of classification, to the scientific and technical meaning of the terms and expressions used therein, but to their popular meaning, that is to say, the meaning attached to that by those using the product.

The burden of proof that a product is classifiable under a particular tariff head is on the revenue and must be discharged by proving that it is so understood by the consumers of product in common parlance – CCE v. Vicco Laboratories 2005 (179) ELT 17 (SC 3 member bench

Broad Outline of Theory

Arrangement of Goods under the Tariff

It is important to first narrow down the search for the relevant classification by scaling it down to a particular Section or Chapter. It is interesting to note that the various commodities grouped under the Sections, Chapters, etc are arranged in increasing order of manufacturing process required on the said commodity – for instance, the Tariff begins with natural products, raw materials, goes on to semi- finished goods and concludes with fully manufactured goods. Reliance is not to be placed solely on the Section or Chapter Titles to classify the product therein.

–

–

Step 1: Identify the goods that require classification. –

Step 2: In the Tariff Schedule, commodities are arranged in increasing order of manufacturing process – Identify the broad Sections and Chapters, the said commodity would fall under –

Step 3: By way of application of General Rules of Interpretation, classify the product in terms of the 8-digit-classification –

Step 4: Find the relevant sub-heading, as per Step 3. The GST Rate Schedule (along with amending notifications) has specified various rates, grouped under 4-digit or 6- digit-classification. Further, a particular Heading may appear in several Schedules, for example, CTH 2106 [Food preparations not specified elsewhere] — Step 5: Find the relevant description of heading in GST Rate Schedule and corresponding Rate

11/2017-CT (Rate) dated 28.06.2017

Burden of classification on department

- Onus of establishing that an article falls in a particular tariff lay upon the revenue. -. -. – Even if evidence produced by assessee is rejected, the appeal of assessee has to be allowed (as Revenue has not discharged the onus of establishing a classification) –

- Hindustan Ferodo Ltd. v. CCE 1997(2) SCC 677 = 89 ELT 16 SC = 17 RLT 807 = 106 STC 214 (SC).

- Burden of proof of classification of goods is on department – Hewlatt Packard India Sales v. CC (Imports) (2023) 383 ELT 241 = 2 Centax 236 (SC).

- The burden of proof that a product is classifiable under a particular tariff head is on the revenue and must be discharged by proving that it is so understood by the consumers of product in common parlance – CCE v. Vicco Laboratories 2005 (179) ELT 17 (SC 3 member bench).

GST COURSE