Writ petition filed before Hon’ble Gujarat High Court challenging vires of of The Section 17(2) and 17(3) of the Central Goods and Services Tax Act, 2017 & The Gujarat (State) Goods and Services Tax Act, 2017 vis-à-vis Article 14, 19, 21 & 265 of the Constitution of India to be declared as void and unconstitutional.

The petition filed by Advocate Nipun Singhvi, challenged the provisions being violative as it restricts the credit of the input tax credit on goods / services or both used by Advocates for effecting taxable legal services and exempt legal services.

Counsel for the petitioner Advocate Vishal J. Dave submitted “That the tax to be paid by the litigant on taxable legal services in the absence of provision for availment of input tax credit by advocates is leading to the effect of cascading of taxes since the tax component in the form of taxes on goods and services or both used by advocates including petitioner for providing the said taxable legal services becomes part of the cost of the advocates, which is passed on to the clients by way of professional fee on which again GST is chargeable.”

The petitioner prayed for introducing mechanism for availing input tax credit on the expenses done with respect to goods and services availed by the advocates.

The petitioner who is qualified Chartered Accountant and a financial activist has been actively filing public interest litigation/writs significant among them are Demonetisation, Tribunals under Finance Act, 2017; GST provisions relating to AAR/AAAR and Appointment of Technical Member in NCLT.

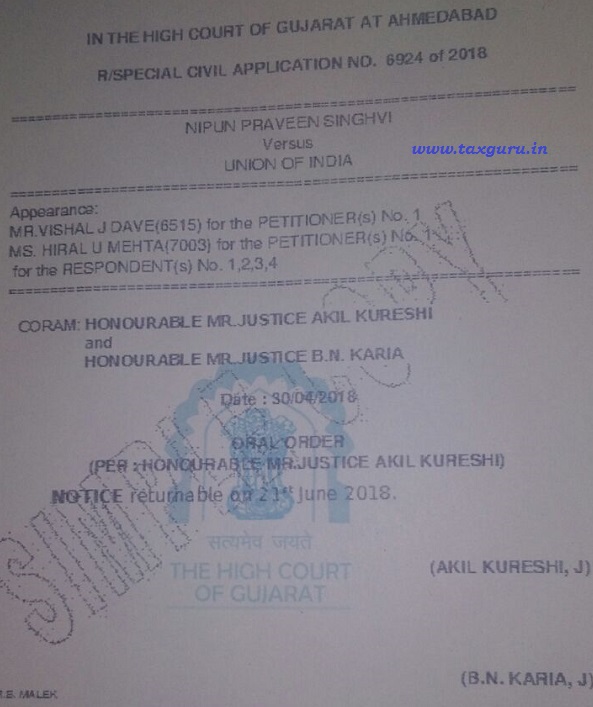

Gujarat High Court issued notices to Centre, State and GST Council on Monday. Next date of hearing is fixed on 21.06.2018.

Advocates want to take itc even when they are not paying anything The client who pays under RCM gets the credit The client below 20 lakh neeed not pay tax under rcm

Where is the problem They are wasting court time for publicity

ok, Mr & Mrs. Advocates… In GST if goods or service is taxable in the hands of provider, will eligible to take GST Credit, your service not taxable under GST, but need to pay by receiver…

Dept will allow you all to take credit but your outward will be taxed……… is this acceptable from advocate….

It is a fair rule and goes in favour of principle of natural justice, if taxes are not borne by supplier on outward supply of goods/services/both then input credit should also not be allowed to enjoy. The ultimate consumer of advocate services bears the cost on which GST is already paid. RCM is not in force so no question of double taxation/cascading effect.

Adv prathap pillai ,kerala.

since advocates are not required to register even if their aggregate turnover crosses the 20 lakh threshold is saving them from taxing their unregistered clients or in other words clients are relieved from GST burden. Therefore their is no or illegality or lack of fairness in passing the costs to clients

An Advocate or any other Professionals require lot of inputs of different types to enable him/them to render Professional services.In all cases Inputs and Outputs need not necessarily be of same nature.

rightly done as ITC should not be blocked just because RCM is applicable on output supply and serivices..because it doesn’t make any sense that as per sec. 17(2) and 17(3) block ITC on part of services on which RCM payable..its harsh

But what are the legal services which are taxable at hands of Advocates ??