- A. FAQs on GST Registration by Casual Taxable Person

- Q.1 I want to take a Registration as a Casual Taxable Person but I can’t find the option.

- Q.2 Can a Casual Taxable Person opt for Composition?

- Q.3 When should I apply for a Registration as a Casual Taxable Person?

- Q.4 How long is the Registration as a Casual Taxable Person valid?

- Q.5 Can I extend my Registration as a Casual Taxable Person?

- Q.6 I have already extended my initial registration once and cannot extend it a second time as per prevailing laws. What do I do if my extension is about to expire and my business has not concluded?

- Q.7 The moment I select Registration as a Casual Taxable Person option, the New Registration Application prompts me to fill a GST Challan. Why?

- Q.8 Is there a fixed amount I must deposit with the GST authorities before taking a Registration as a Casual Taxable Person?

- Q.9 Can a Casual Taxable Person take multiple registrations in a State?

- Q.10 I have deposited advance tax but do not want to continue the business. How shall I get my money back?

- B. Manual on filing of GST Registration Application by Normal Taxpayer/ Composition/ Casual Taxable Person/ Input Service Distributor (ISD)/ SEZ Developer/ SEZ Unit

A. FAQs on GST Registration by Casual Taxable Person

Q.1 I want to take a Registration as a Casual Taxable Person but I can’t find the option.

Ans: The option to register is in the New Registration Application for a normal taxpayer.

In PART A of the New Registration Application, select Taxpayer (Reference screenshot (highlighted in red)):

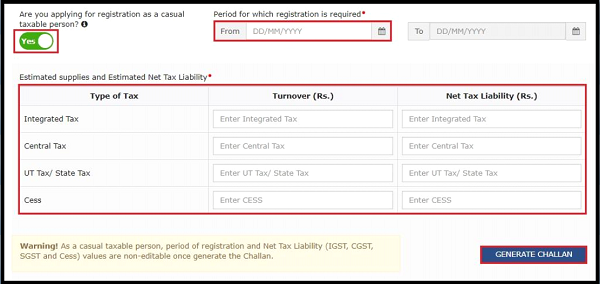

2. In PART B of the New Registration Application in the Business Details section, select Yes under ‘Are you applying for registration as a casual taxable person?’ as shown in the screenshot below:

3. Enter the estimated values of supplies and estimated net tax liability as CGST + SGST / IGST and cess for the period for which registration is applied and click the GENERATE CHALLAN button. This option is also available after all tabs of Part B of the Registration application is filled up.

4. Make the advance tax payment using the payment modes available on the GST Portal and then complete Part B of the registration application and submit it.

5. Your registration will be granted after due processing by the concerned Tax Official.

Q.2 Can a Casual Taxable Person opt for Composition?

Ans: Casual Taxable Person cannot opt for composition.

Q.3 When should I apply for a Registration as a Casual Taxable Person?

Ans: You should apply for Registration as a Casual Taxable Person at least 5 days prior to the commencement of business.

Q.4 How long is the Registration as a Casual Taxable Person valid?

Ans: The certificate of registration issued to a casual taxable person shall be valid for the period specified in the application for Registration or ninety days from the effective date of registration, whichever is earlier.

Q.5 Can I extend my Registration as a Casual Taxable Person?

Ans: Yes, you can extend your Registration as a Casual Taxable Person once for an additional period of 90 days, if you apply for extension of registration before the expiry of the initial period for which registration was granted.

Q.6 I have already extended my initial registration once and cannot extend it a second time as per prevailing laws. What do I do if my extension is about to expire and my business has not concluded?

Ans: In such a case, you are required to obtain registration as a normal taxpayer in the concerned state.

Q.7 The moment I select Registration as a Casual Taxable Person option, the New Registration Application prompts me to fill a GST Challan. Why?

Ans: In case of Registration as a Casual Taxable Person, you are required by law to deposit the tax in advance equivalent to the estimated tax liability based on the estimated turnover for the period for which the casual registration has been obtained. A provisional GSTIN will also be generated and prefilled in the challan. The status of this GSTIN will be provisional until your application is approved by the tax authority and the casual registration is officially granted.

Q.8 Is there a fixed amount I must deposit with the GST authorities before taking a Registration as a Casual Taxable Person?

Ans: No, you are required by law to deposit the tax in advance equivalent to the estimated tax liability based on the estimated turnover for the period for which the casual registration is being obtained by you.

Q.9 Can a Casual Taxable Person take multiple registrations in a State?

Ans: In case a Casual taxable person has multiple business verticals within one state, the Casual taxable person can apply for multiple registrations within the state.

Q.10 I have deposited advance tax but do not want to continue the business. How shall I get my money back?

Ans: You can apply for refund of advance tax deposited at the time of filing of application for surrender of registration.

B. Manual on filing of GST Registration Application by Normal Taxpayer/ Composition/ Casual Taxable Person/ Input Service Distributor (ISD)/ SEZ Developer/ SEZ Unit

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

I have applied for casual tax payer registration for Exhibition conduct in punjab. I have paid estimated tax amount Rs. 10000/- ( CGST & SGST). But My registration rejected. If it possible for GST Refund applied for estimate tax paid amount. How do apply ?

How to apply GST Advance tax paid amount for Casual Registration?? Even though the Casual registration was not approved by GST officer..Hence not able to add bank details..Please suggest..

Sir.

Can we ( expired casual taxable person gst no) gst return file or not ? After expiring the gdt no…

I instead got permanent GST Registration done as my frequency availing Casual GST was very high in Bangalore.

I booked it from InstaSpaces.in through their virtual office service with proper documents. I paid 1000/month for this solution

Sir…

If casual dealer takes registration for 30days after completion of its term…

Is it mandatory to surrender or apply for cancellation of GSTN or it will automatically gets surrendered.

At Portal it is showing inactive….

Kindly let me know….

Thanks & Regards

Priya Maheshwari

Dear Mohnish ji. I am just starting my business and have registered under GST in Mumbai. Am participating in an exhibition in Delhi and will issue invoices with Mumbai Address with full taxable amount as IGST. Yhe organizer insists on temporary Delhi GST.

As this is 1 day ehbition can I not issue invoices with my Mumbai address and charge full IGST. Have raised eway bill too. Warm Regards Vimal

I am registered under GST Act in Punjab. I want to hold exhibition cum sale in another city of Punjab. Do I need to register under Casual Dealer?

Hello,

Do we have to continue to file returns once our Casual Taxable period is completed ?

We have paid tax and filed all our returns for the period for which our casual taxable period was active.

Now the period has expired and our work is over. The status of our registration on website has become Inactive.

In that case do we have to still file GST Returns ?

Kindly let me know

Thanks and Regards

Aparna Bhatia

what if tax liability is nil then??

I want to do exhibitions but i dont expect my turnober to be more than 50000..do i need to apply for temporary gst no? And what if my sales are even lesser than what i have paid in advance?

Im too small a player. Kindly guide

we have applied for casual tax payer , paid advance but our application was rejected . how can we geet that advance money back as we dont have login id and password . also it is not showing refund column to file FRD01 A

i have to register for an exhibition what if my actual GST liability exceeds the amount I have paid as advance

You can fill up the same in GSTR-1 and GSTR-2 subsequently.

Sir,

We have not mentioned the nil rated & non gst

inword supplies in the gstr-3b . what can I do sir.

Awaiting your favourable reply