A. E-invoice – Basics:

Q. 1. What is ‘e-invoicing’?

As per Rule 48(4) of CGST Rules, notified class of registered persons have to prepare invoice by uploading specified particulars of invoice (in FORM GST INV-01) on Invoice Registration Portal (IRP) and obtain an Invoice Reference Number (IRN).

After following above ‘e-invoicing’ process, the invoice copy containing inter alia, the IRN (with QR Code) issued by the notified supplier to buyer is commonly referred to as ‘e-invoice’ in GST.

Because of the standard e-invoice schema (INV-01), ‘e-invoicing’ facilitates exchange of the invoice document (structured invoice data) between a supplier and a buyer in an integrated electronic format.

Please note that ‘e-invoice’ in ‘e-invoicing’ doesn’t mean generation of invoice by a Government portal.

Q. 2. How is ‘e-invoicing’ different from present system?

There is no much difference indeed.

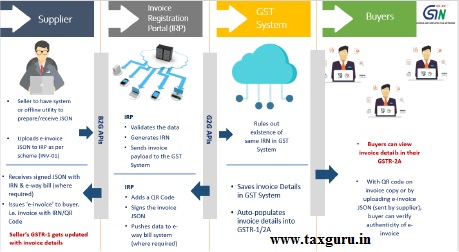

Registered persons will continue to create their GST invoices on their own Accounting/Billing/ERP Systems. These invoices will now be reported to ‘Invoice Registration Portal (IRP)’. On reporting, IRP returns the e-invoice with a unique ‘Invoice Reference Number (IRN)’ after digitally signing the e-invoice and adding a QR Code. Then, the invoice can be issued to the receiver (along with QR Code).

A GST invoice will be valid only with a valid IRN.

For more detailed process, please go through ‘e-invoice – Detailed Overview’

Q. 3. For which businesses, e-invoicing is mandatory?

For Registered persons whose aggregate turnover (based on PAN) in any preceding financial year from 2017-18 onwards, is more than prescribed limit (as per relevant notification), e-invoicing is mandatory.

Q. 4. What are the legal provisions governing e -invoice?

Below notifications were issued on e-invoice:

| Notification No. (Central Tax) |

Key Contents | |

| 68/2019 Dt. 13-12-2019 | Key Contents

(4) The invoice shall be prepared by such class of registered persons as may be notified by the Government, on the recommendations of the Council, by including such particulars contained in FORM GS T IN V-01 after obtaining (5) Every invoice issued by a person to whom sub-rule (4) applies in any manner other than the manner specified in the said sub-rule shall not be treated as an invoice. (6) The provisions of sub-rules (1) and (2) shall not apply to an invoice prepared in the manner specified in sub-rule (4). Notified 10 Common Goods and Services Tax Electronic Portals for the purpose of preparation of invoice in terms of rule 48 (4) |

|

| 69/2019 Dt. 13-12-2019 | ||

| 70/2019 Dt. 13-12-2019 | Notified registered person, whose aggregate turnover in a financial year exceeds one hundred crore rupees, as a class of registered person who shall prepare invoice in terms of sub-rule (4) of rule 48 of the said rules in respect of supply of goods or services or both to a registered person; notification to come into force from the 1st day of April, 2020

(This notification superseded by 13 of 2020 Dt. 21-3-2020) |

|

| 2 of 2020 Dt. 1-1-2020

13 of 2020 Dt. 21-3-2020 (in supersession of 70/2019 Dt. 13-12-2019) |

Substituted Form GST INV-1 as e-invoice schema

(Schema further amended vide Notification 60/2020 Dt. 30-7-2020)

(Further amended by 61/2020 Dt. 30-7-2020)

|

|

|

|

||

| 61/2020 Dt. 30-7-2020 |

|

|

Q. 5. What are the advantages of e-invoice for businesses?

e-invoice has many advantages for businesses such as Auto-reporting of invoices into GST return, auto-generation of e-way bill (where required).

e-invoicing will also facilitate standardisation and inter-operability leading to reduction of disputes among transacting parties, improve payment cycles, reduction of processing costs and thereby greatly improving overall business efficiency.

Q. 6. What businesses need to do, to be e -invoice ready?

Businesses will continue to issue invoices as they are doing now. Necessary changes on account of e-invoicing requirement (i.e. to enable reporting of invoices to IRP and obtain IRN), will be made by ERP/Ac counting and Billing Software providers in their respective software. They need to get the updated version having this facility.

Q. 7. Is an invoice/CDN/DBN (required to be reported to IRP by notified person), valid without IRN?

As per Rule 48(4), notified person has to prepare invoice by uploading specified particulars in FORM GST INV-01 on Invoice Registration Portal and after obtaining Invoice Reference Number (IRN).

As per Rule 48(5), any invoice issued by a notified person in any manner other than the manner specified in Rule 48(4), the same shall not be treated as an invoice.

So, the document issued by notified person becomes legally valid only with an IRN.

However, in the initial period of operation, Government has given a relaxation that invoices raised by notified taxpayers during October, 2020 without following e -invoice procedure (i.e. uploading invoice details on e-invoice portal (IRP), obtaining IRN and issuing invoice with QR Code) will be deemed to be valid and no penalty will be there if the IRN for such invoices is obtained within 30 days of date of invoice.

It was also specified that no such relaxation would be available for the invoices issued from 1st November 2020.

B.E-invoice – Applicability:

Q. 8. What documents are presently covered under e-invoicing?

i. Invoices

ii. Credit Notes

iii. Debit Notes,

when issued by notified class of taxpayers (to registered persons (B2B) or for the purpose of Exports) are currently covered under e-invoice.

Though different documents are covered, for ease of reference and understanding, the system is referred as ‘e-invoicing’.

Q. 9. What supplies are presently covered under e-invoice?

Supplies to registered persons (B2B), Supplies to SEZs (with/without payment), Exports (with/without payment), Deemed Exports, by notified class of taxpayers are currently covered under e-invoicing.

Q. 10. B2C (Business to Consumer) supplies can also be reported by notified persons?

No. Reporting B2C invoices by notified persons is not applicable/allowed currently. However, they will be brought under e-invoice in the next phase.

Q. 11. Is e -invoicing applicable for NIL-rated or wholly-exempt supplies?

No. In those cases, a bill of supply is issued and not a tax invoice.

Q. 12. Whether the financial/commercial credit notes also need to be reported to IRP?

No, only the credit and debit notes issued under Section 34 of CGST/SGST Act have to be reported.

Q. 13. Whether e-invoicing is applicable for supplies by notified persons to Government Departments?

e-invoicing by notified persons is mandated for supply of goods or services or both to a registered person.

Thus, where the Government Department doesn’t have any registration under GST (i.e. not a ‘registered person’), e-invoicing doesn’t arise.

However, where the Govt. department is having a GSTIN (as entity supplying goods/services/ deducting TDS), the same has to be mentioned as recipient GSTIN in the e-invoice.

Q. 14. Whether e-invoicing is applicable for invoices between two different GSTINs under same PAN?

Yes. e-invoicing by notified persons is mandated for supply of goods or services or both to a registered person.

As per Section 25(4) of CGST/SGST Act, “A person who has obtained or is required to obtain more than one registration, whether in one State or Union territory or more than one State or Union territory shall, in respect of each such registration, be treated as distinct persons for the purposes of this Act.”

Q. 15. For high sea sales and bonded warehouse sales, whether e -invoicing is applicable?

No. These activities/transactions are neither supply of goods nor a supply of services, as per Schedule III of CGST/SGST Act.

Q. 16. What is the applicability of e-invoice for import transactions?

e-invoicing is not applicable for import Bills of Entry.

17. Which entities/sectors are exempt from the e-invoicing mandate?

a. Special Economic Zone Units

b. insurer or a banking company or a financial institution, including a non-banking financial company

c. goods transport agency supplying services in relation to transportation of goods by road in a goods carriage

d. Suppliers of passenger transportation service

e. Suppliers of services by way of admission to exhibition of cinematograph films in multiplex screens

Q. 18. The exemption from e -invoicing is w.r.t the nature of supply/transaction or w.r.t the entity?

It is for the entity.

Q. 19. Do SEZ Developers need to issue e-invoices?

Yes, if they have the specified turnover and fulfilling other conditions of the notification.

In terms of Notification (Central Tax) 61/2020 dt. 30-7-2020, only SEZ Units are exempted from issuing e-invoices.

Q. 20. Are Free Trade & Warehousing Zones (FTWZ) exempt from e-invoicing?

Yes. As per Foreign Trade Policy, Free Trade & Warehousing Zones (FTWZ) are only a special category of Special Economic Zones, with a focus on trading and warehousing.

Q. 21. Is e-invoicing applicable for supplies by notified persons to SEZs?

Yes, e-invoicing is applicable for supplies by notified persons to SEZs.

In terms of Notification (Central Tax) 61/2020 dt. 30-7-2020, only SEZ Units are exempt from issuing e-invoices.

Q. 22. There is an SEZ unit and a regular DTA unit under same legal entity (i.e. having same PAN). The aggregate total turnover of the legal entity is more than Rs. 500 Crores (considering both the GSTINs). However, the turnover of DTA unit is below Rs. 100 crores for FY 19-20.

In this scenario, as SEZ unit is exempt from e -invoicing, whether e -invoicing will be applicable to DTA Unit?

Yes, because the aggregate turnover of the legal entity in this case is > Rs. 500 Crores. The eligibility is based on aggregate annual turnover on the common PAN.

Q. 23. Is e-invoicing applicable to invoices issued by Input Service Distributor (ISD)?

No

Q. 24. Whether e-invoicing is applicable for supplies involving Reverse Charge?

If the invoice issued by notified person is in respect of supplies made by him but attracting reverse charge under Section 9(3), e-invoicing is applicable.

For example, a taxpayer (say, a Firm of Advocates having aggregate turnover in a FY is more than Rs. 500 Cr.) is supplying services to a company (who will be discharging tax liability as recipient under RCM), such invoices have to be reported by the notified person to IRP.

On the other hand, where supplies are received by notified person from (i) an unregistered person (attracting reverse charge under Section 9(4)) or (ii) through import of services, e-invoicing doesn’t arise / not applicable.

Q. 25. How to know a particular supplier is supposed to issue e -invoice (i.e. invoice along with IRN/QR Code)?

On fulfilment of prescribed conditions, the obligation to issue e-invoice in terms of Rule 48(4) (i.e. reporting invoice details to IRP, obtaining IRN and issuing invoice with QR Code) lies with concerned taxpayer.

However, as a facilitation measure, all the taxpayers who had crossed the prescribed turnover in a financial year from 2017-18 onwards have been enabled to report invoices to IRP.

One can search the status of enablement of a GSTIN on e-invoice portal: https://einvoice1.gst.gov.in/ > Search > e-invoice status of taxpayer

This listing of GSTINs is solely based on the turnover of GSTR-3B as reported to GST System. It may contain exempt entities or those for whom e-invoicing is not applicable for some other reason. So, it may be noted that enablement status on e-invoice portal doesn’t mean that the taxpayer is supposed to do e-invoicing If e-invoicing is not applicable to a taxpayer, they need not be concerned about the enablement status and may ignore it.

Further, the turnover slab of taxpayer can also be ascertained through “Search Taxpayer” / “Know Your Supplier” Sections on GST portal also.

In case any registered person, is required to prepare invoice in terms of Rule 48(4) but not enabled on the portal, he/she may request for enablement on portal: ‘Registration – > e-Invoice Enablement’.

C. E-invoice – Reporting to IRP:

Q. 26. What is an Invoice Registration Portal (IRP)?

Invoice Registration Portal (IRP) is the website for uploading/reporting of invoices by the notified persons.

Vide notification no. 69/2019-Central Tax dated 13.12.2019, ten portals were notified for the purpose of preparation of the invoice in terms of Rule 48(4).

The first Invoice Registration Portal (IRP) is active and can be accessed at: https://einvoice1.gst.gov.in/

Other portals will be made available in due course.

Q. 27. Is e-invoicing voluntary, i.e. can entities with aggregate turnover below the prescribed limit also report invoices to IRP, if they wish to do so?

No, presently, only the notified class of persons will be allowed/enabled to report invoices to IRP.

Q. 28. Is there any time window within which I need to report an invoice to IRP, i.e. is there any validation to the effect that the ‘document date’ (in the payload to IRP) has to be within a specified time window, for reporting to IRP/generation of IRN?

No such validation is kept on the portal.

Q. 29. Is the signature (DSC) of supplier mandatory while reporting e-invoice to IRP?

No

Q. 30. Can e-commerce operators generate e-invoices on behalf of the sellers on their platforms?

Yes, if such suppliers, selling through e-Commerce entity are otherwise notified persons and supposed to report invoices under Rule 48(4).

For more details, please see this detailed document.

Q. 31. What do I need to generate an e-invoice?

A system/utility to report e-invoice details in JSON format to IRP and to receive signed e-invoice in JSON format from the Portal.

Q. 32. Whether any tool is provided to report invoices to IRP?

Yes. For entities not having their own ERP/Software solutions, they can use the free offline utility (‘bulk generation tool’) downloadable from the e-invoice portal. Through this, invoice data can be easily reported to IRP and obtain IRN/signed e-invoice.

Q. 33. What are various modes for generation of e-invoice?

Multiple modes are available so that taxpayer can use the best mode based on his/her need:

a. API based (integration with Taxpayer’s System directly)

b. API based (integration with Taxpayer’s System through GSP/ASP)

c. Free Offline Utility (‘Bulk Generation Tool’, downloadable from IRP)

Web-based / mobile app-based modes will also be provided in future.

Q. 34. Will it be possible for bulk uploading of invoices to IRP?

Yes. It is possible. The offline utility (‘bulk generation tool’) serves this purpose.

Further, the ERP or accounting systems used by large taxpayers can be designed in such a way that they can report invoices in bulk to IRP.

However, reporting to IRP and generation of IRN will be one after another (which will not be visible for user). For the user, it will appear like bulk upload and bulk receipt.

Q. 35. As many businesses will be reporting invoices, will there be any delay in generation of IRN by IRP? Can the portal take that much load?

IRP is only a pass through validation portal. Certain key fields will be validated on IRP. So, IRN will be generated in sub-200 millisecond duration.

The server capacity is robust enough to handle simultaneous uploads. Further, multiple IRPs will be made available to distribute the load of invoice registration.

The IRPs are dedicated portals other than the regular GST common portal (used for filing registration applications, filing returns, making payments etc.)

Q. 36. Will IRP store/archive e -invoices?

No. IRP will only be a pass-through portal which performs prescribed validations on

invoice data and generates IRN. It will not store or archive e-invoice data.

Q. 37. Will I need to enter invoice details on a government website and obtain IRN?

- In e-invoice scenario, what is primarily envisaged is ‘machine-to-machine’ exchange of invoice data (mainly between taxpayer’s system & IRP).

- If the business doesn’t have ERP/Accounting/Billing Software or have very few invoices to report, they can download and use the free Offline Tool to enter data and create JSON file, for uploading on IRP.

- Web-based and mobile app-based interfaces will also be made available in future.

Q. 38. In case of breakdown of internet connectivity in certain areas, will there be any relaxation in the requirement to obtain IRN?

A localised mechanism to provide relaxation in such contingent situations is prescribed as per proviso to Rule 48(4) of CGST Rules. It reads as: “…Commissioner may, on the recommendations of the Council, by notification, exempt a person or a class of registered persons from issuance of invoice under this sub-rule for a specified period, subject to such conditions and restrictions as may be specified in the said notification.”

D. E-invoice – Schema / Contents:

Q. 39. What is e-invoice schema?

‘Schema’ simply means a structured template or format. ‘e-invoice’ schema is the standard format for electronic invoice. It is notified as ‘Form GST INV-1’.

Q. 40. Why is an e-invoice standard/schema required?

- Presently, businesses are preparing/generating invoices in their respective ERPs/Accounting/Billing Software. All these software have their own format of storing the data of invoice. Thus, the e-invoice generated by one system is not understood by the other, thereby necessitating data entry efforts and consequent errors and reconciliation problems.

- ‘Schema’ acts as uniform standard for ERP/ Billing/Accounting software providers to build utility in their solution/package to prepare e-invoice in notified standard thereby ensuring e-invoice generated by any ERP/Accounting and Billing Software is correctly understood by another ERP/Accounting software. This is also required for ensuring uniformity in reporting to IRP.

- Schema ensures e-invoice is ‘machine-readable’ and ‘inter-operable’, i.e. the invoice/format can be readily ‘picked up’, ‘read’, ‘understood’ and further processed by different systems like Oracle, Tally, SAP etc.

Q. 41. What is the basis of e-invoice schema?

e-invoice Schema is based on PEPPOL/Universal Business Language (UBL) with certain customizations to cater to Indian business practices and legal requirements.

Q. 42. Is there different invoice schema for different sectors/businesses, e.g. Traders, Manufacturers, Service Providers, Professionals etc.?

No. e-invoice schema is a single standard applicable to all businesses in the country. Many optional fields are available in the schema to cater to the requirements of specific businesses and practices followed by industry and trade in India.

Q. 43. What is the file format in which invoice has to be reported to IRP?

Invoice details in prescribed schema (INV-01) have to be reported to IRP in JSON format.

‘JSON’ stands for JavaScript Object Notation. It can be thought of as a common language for systems/machines to communicate between each other and exchange data.

As the ERP or Accounting software will generate it, taxpayer need not worry about it. This format is also used in GST system for reporting all data to GST System.

Q. 44. What are the various types of fields in e-invoice schema?

a. Data for fields marked as ‘Mandatory’ have to be provided compulsorily.

b. A mandatory field not having any value can be reported as NIL.

c. Fields marked as ‘Optional’ may or may not be filled up. Many of these are relevant for specific businesses (e.g. Batch No., Attributes etc.) and to cater to specific scenarios (e.g. export, e-way bill etc.).

d. Some sections in the schema are marked as ‘Optional’. But, if this section is selected, some of the fields may be mandatory. For example, the section ‘e-way Bill Details’ is marked as optional. But, if this section is chosen, the field, ‘Mode of Transportation’ is mandatory.

Q. 45. What is ‘cardinality’, as mentioned in schema?

In e-invoice schema, for each field, ‘Cardinality’ is marked as 0..1 / 1..1 / 1..n / 0..n. This is to denote whether a field is ‘mandatory’ and whether it is ‘repetitive’.

| Notation | Meaning |

| Starts with 0 | Optional field |

| Starts with 1 | Mandatory field |

| Ends with 1 | Data for the field can be entered only once |

| Ends with n | Data for the field can be entered multiple times |

Q. 46. Can the supplier place their entity logo on e -invoice? Is this part of schema?

Elements of invoice which are internal to business, such as company logo etc. are not part of e-invoice schema.

After reporting invoice details to IRP and receipt of IRN, at the time of issuing invoice to receiver (e.g. generating as PDF and printing as paper copy or forwarding via e-mail etc.), any further customisation, i.e. insertion of company logo, additional text etc., can be made by respective ERP/billing/accounting software providers.

Q. 47. What is the maximum number of line items which can be reported in an invoice?

The limit is kept at 1000 presently. It will be enhanced based on requirement in future.

Q. 48. In the e-invoice schema, the amount under ‘other charges (item level)’ is not part of taxable value. However, some charges to be shown in invoice are leviable to GST. How to mention them?

Such other charges (taxable), e.g. freight, insurance, packing & forwarding charges etc. may be added as one more line item in the invoice.

Q. 49. In e-invoice schema, there is no placeholder for mentioning TCS (Tax Collected at Source) collected by suppliers under Income Tax Act, 1961.

At present, there is no separate placeholder for this field in schema. Including it in schema will be examined in next round of revision.

However, as a work around, the field of “Other Charges (Invoice Level)” can be used to mention TCS where it doesn’t form part of taxable value.

It may further be noted that INV-01 schema is only to report specified invoice particulars to IRP. Once IRN is obtained from the portal, the business may add any other elements not relevant to GST, while issuing invoice finally to buyer.

Q. 50. In the current schema, there is no provision to report details of supplies not covered under GST, e.g. a hotel wants to give single invoice for a B2B supply where the supply includes food and beverages (leviable to GST) and Alcoholic beverages (outside GST).

For items outside GST levy, separate invoice may be given by such businesses.

Q. 51. The field “Differential Percentage” of tax rate is not available in schema, which is applicable on “Leasing of vehicles purchased and leased prior to July 1, 2017”.

This is not relevant/applicable after 30.06.2020

Q. 52. In case of Credit Note and Debit Note, is there any validation w.r.t referred invoice number?

No linkage with invoice is built, in view of the amended provisions of GST.

Q. 53. Some HSNs which are otherwise valid are not accepted by e -invoice portal.

HSN directory is being aligned with GST System, so that it is updated and uniform on all systems, viz. Customs (ICES), GST System, e-way bill system and e-invoice system.

E. E-invoice – Generation of IRN:

Q. 54. Is Invoice number same as Invoice Reference Number (IRN)?

No. Invoice no. (e.g. ABC/1 /2019-2 0) is assigned by supplier and is internal to business. Its format can differ from business to business and also governed by relevant GST rules.

IRN, on other hand, is a unique reference number (hash) generated and returned by IRP, on successful registration of e-invoice.

Q. 55. How a typical IRN looks like?

IRN is a unique 64-character hash, e.g.

35054cc24d9 7033afc24f49ec4444dbab81f542c555f9d30359dc75794e06bbe

Q. 56. Can IRP reject a submitted invoice? On reporting invoice details to IRP, what validations will performed on the portal?

Yes. IRP can reject an invoice.

IRP will check whether the invoice was already reported and existing in the GST System. (This validation is based on the combination of Supplier’s GSTIN-Invoice Number-Type Of Document-Fin.Year, which is also used for generation of IRN). In case the same invoice (document) has already been reported earlier, it will be rejected by IRP.

Certain other key validations will also be performed on portal. In case of failure, registration of invoice won’t be successful, IRN won’t be generated and invoice will be rejected along with relevant error codes (which give idea about reasons for rejection.)

Q. 57. On reporting invoice details, what will be returned by IRP? Will it return signed JSON or PDF or both?

IRP will return only the signed JSON. No PDF will be returned. On receipt of signed JSON, it is for the respective ERP or Accounting & Billing software system to generate PDF, if needed.

Q. 58. What is the indication for the supplier that IRP has registered the reported invoice?

Upon successful registration of invoice on IRP, it will return a signed e-invoice JSON to the supplier with IRN and QR Code.

F. E-invoice – Printing of Invoice / IRN / QR Code

Q. 59. Can I print an e-invoice?

Yes. Once the IRP returns the signed JSON, your ERP/Accounting/Billing System it into PDF and printed, if required.

Businesses who don’t have their own ERP/Accounting Software, will be downloadingand using the free offline utility (‘bulk generation tool’) to upload invoice data on e-invoice portal and obtain signed invoice (in JSON). In this scenario also, there is a facilityon e-invoice portal to generate ‘human-readable’ PDF copy of invoice (for save/print/e-mail etc.).

Q. 60. Do I need to print IRN on the invoice?

No. It’s optional. IRN is anyway embedded in the QR Code which is one of the mandatory particulars on invoice.

Q. 61. How will the QR Code be received?

The QR code is part of signed JSON, returned by the IRP. It is a string (not image), which the ERP/accounting/billing software shall read and convert into QR Code image for placing on the invoice copy.

Q. 62. Do I need to print QR Code on the invoice? If so, what shall be its size and location on the invoice copy?

Yes. The QR code (containing, inter alia, the IRN) which comes as part of signed JSON from IRP, shall be extracted and printed on the invoice.This is one of the mandatory particulars of invoice under Rule 46 of CGST Rules.

However, printing of QR code on separate paper is not allowed.

While the printed QR code shall be clear enough to be readable by a QR Code reader, the size and its placing on invoice is upto the preference of the businesses.

Q. 63. Where e-invoicing is applicable for notified persons, when the invoice is generated/printed by the supplier (for issuance to buyer), what are the mandatory contents of such invoice issued/printed?

The particulars will be as per Rule 46 of CGST Rules, including QR code, with embedded Invoice Reference Number (IRN).

Q. 64. While returning IRN, the IRP is also adding its digital signature, “Acknowledgement No.” and “Date”. Whether these also need to be printed while issuing invoice?

No. There is no mandate to print these particulars on invoice copy.

Note that the “Acknowledgement No.” and “Date” given by IRP are only for reference. Being a 15-digit number, the acknowledgement number will also come handy for printing e-invoice or for generating e-way bill (instead of keying in the 64-character long IRN).

Q. 65. If e-invoice is applicable and issued, am I supposed to issue copies of invoice in triplicate/duplicate?

Where e-invoicing is applicable, there is no need of issuing invoice copies in triplicate/duplicate. This is clearly specified in Rule 48(6).

Q. 66. Will it be possible for invoices that are registered on IRP to be downloaded and saved on handheld devices?

It depends on the ERP/Accounting/Billing Software, providing you the service. The signed JSON can be stored on handheld devices also.

However, signed invoice JSON will not be available for download from IRP or GST System. Hence, it is advisable to properly store the signed e-invoice received from IRP.

Q. 67. What is the period of retention/storage/archival, in case of e -invoicing?

As per Rule 56(16) of CGST Rules, “Accounts maintained by the registered person together with all the invoices, bills of supply, credit and debit notes, and delivery challans relating to stocks, deliveries, inward supply and outward supply shall be preserved for the period as provided in section 36…”

The same applies to e-invoicing also.

Q. 68. Are there any penal provisions for not issuing invoice in accordance with GST Law/rules?

The penal provisions are provided in Section 122 of CGST/SGST Act read with CGST Rules.

G. E-invoice – Verification of IRN / QR Code:

Q. 69. How to verify an invoice is duly reported to IRP?

One can verify the authenticity or correctness of e -invoice by uploading the signed JSON file or Signed QR Code (string) on e-invoice portal: einvoice1.gst.gov.in > Search > ‘Verify Signed Invoice’

Alternatively, with “Verify QR Code” mobile app which may be downloaded from einvoice1.gst.gov.in > Help > Tools > Verify QR Code App

Q. 70. What data is embedded in QR Code?

The QR code will consist of the following key particulars of e-invoice:

a. GSTIN of Supplier

b. GSTIN of Recipient

c. Invoice number, as given by Supplier

d. Date of generation of invoice

e. Invoice value (taxable value and gross tax)

f. Number of line items

g. HSN Code of main item (line item having highest taxable value)

h. Unique IRN (Invoice Reference Number/hash)

i. IRN Generation Date

Q. 71. What is dynamic QR Code? Does it has any relevance for B2B e-invoicing?

Notification No. 14/2020-Central Tax dated 21st March, 2020 (as amended) mandates entities with aggregate turnover > Rs. 500 crores in any preceding financial year from 2017-18 onwards, to include a dynamic Quick Response Code (QR Code) on their B2C invoices. It is also specified that a Dynamic QR code made available to buyer through digital display (with payment cross-reference) shall be deemed to be having QR code.

The Dynamic QR Code has no relevance or applicability to ‘e-invoicing’, as envisaged under Rule 48(4). The said rule applies to B2B Supplies and exports by notified class of taxpayers.

Q. 72. Is it possible to have more than one QR code on an invoice?

Yes. Apart from the QR code relating to IRN, the supplier is free to place any other QR Code which is required as per business needs or otherwise mandated by any other statutory requirement.

In such cases, the QR Codes need to be marked clearly so that they can be distinguished easily.

H. E-invoice – Sending to Receiver:

Q. 73. On generation of IRN, will the IRP send or e-mail the e-invoice to the receiver?

No. IRP will not do this. Upon receiving signed JSON from the IRP, it is for the supplier to share the e-invoice (along with QR Code etc.) in agreed format to the receiver.

Q. 74. How will the supplier send the e-invoice to the receiver?

A suggested mechanism may be to exchange the PDF of the JSON received from IRP, (including QR code) as the best authenticated version of the e-invoice for business transactions.

Q. 75. However, a mechanism to enable system-to-system exchange of e-invoices through ecosystem partners will be made available in due course. After obtaining signed JSON (along with IRN/QR Code) from e-invoice portal and while issuing invoice copy to the recipient, whether supplier’s signature / digital signature is required on invoice?

The requirement is governed by the provisions of Rule 46 of CGST Rules, 2017.

Q. 76. Taxpayers (for whom e-invoicing is compulsory) will be making supplies to small businesses (for whom e-invoicing is not mandatory). How these small businesses will get the invoice from those big suppliers?

In the same way as it is being done now. For example, the large taxpayers can convert the signed e-invoice JSON into PDF and share the copy by e-mail or send printed copy by post, courier etc.

However, a mechanism to enable system-to-system exchange of e-invoices will be made available in due course.

Q. 77. Where e-invoicing is applicable, is carrying e-invoice print during transportation of goods mandatory?

No. As per Rule 138A(2) of CGST Rules, where e-invoicing is applicable, “the Quick Reference (QR) code having an embedded Invoice Reference Number (IRN) in it, may be produced electronically, for verification by the proper officer, in lieu of the physical copy of such tax invoice.”

I. E-invoice – Amendment / Cancellation:

Q. 78. Can I amend details of a reported invoice for which IRN has already been generated?

Amendments are not possible on IRP. Any changes in the invoice details reported to IRP can be carried out on GST portal (while filing GSTR-1). In case GSTR-1 has already been filed, then using the mechanism of amendment as provided under GST.

However, these changes will be flagged to proper officer for information.

Q. 79. Can an IRN/invoice reported to IRP be cancelled?

Yes. The cancellation request can be triggered through ‘Cancel API’ within 24 hours from the time of reporting invoice to IRP.

However, if the connected e-way bill is active or verified by officer during transit, cancellation of IRN will not be permitted.

In case of cancellation of IRN, GSTR-1 also will be updated with such ‘cancelled’ status.

Q. 80. Can an invoice number of a cancelled IRN be used again?

No. Once an IRN is cancelled, the concerned invoice number cannot be used again to generate another e-invoice/IRN (even within the permitted cancellation window). If it is used again, then the same will be rejected when it is uploaded on IRP.

This is because IRN is a unique string based on Supplier’s GSTIN, Document Number, Type of Document & Financial Year.

Q. 81. Can I partially cancel a reported invoice?

No. It has to be cancelled in toto. No partial cancellation of reported e-invoice allowed.

Cancellation of invoices is governed by Accounting Standards and other applicable rules/regulations.

J. E-invoice – Linkage with E-Way Bill / GST Return:

Q. 82. With the introduction of e-invoicing, is e-way bill still compulsory?

Yes. While transporting goods, wherever the e-way bill is needed, the requirement continues to be mandatory.

Q. 83. Will the e -invoice details be pushed to GST System? Will they populate the return?

Yes. On successful reporting of invoice details to IRP, the invoice data (payload) including IRN, will be saved in GST System. The GST system will auto-populate them into GSTR-1 of the supplier and GSTR-2A of respective receivers.

With source marked as ‘e-invoice’, IRN and IRN date will also be shown in GSTR-1 and GSTR-2A.

Q. 83. Whether the e-way bill get auto-generated?

In case both Part-A and Part-B of e-way bill are provided while reporting invoice details to IRP, they will be used to generate e-way bill.

In case Part-B details are not provided at the time of reporting invoice to IRP, the same will have to be provided by the user through ‘e-way bill’ tab in IRP log in or e-Way Bill Portal, so as to generate e-way bill.

K. E-invoice – Technology / Portal / APIs:

Q. 85. Where e-invoice API integration specifications be found?

They can be viewed at https://einv-apisandbox.nic.in/

Q. 86. Are there more FAQs on e-invoice from IRP/technology/developer’s angle?

FAQs relating to registration and log in on the e-invoice portal can be accessed at https://einvoice1.gst.gov.in/Others/Faqs

FAQs relating to APIs/Testing/Sandbox can be accessed at: https://einv-apisandbox.nic.in/FaqsonAPI.html

Q. 87. Who is an “Application Service Provider”? How can one become an ASP?

ASPs are software service providers who route GST data of their clients to GST System through GSPs (GST Suvidha Providers).

There is no empanelment for ASP. The software company needs to tie-up with a GSP to push data of its clients to GST System or download data of its clients from GST System.

As far as IRP is concerned, no separate category of GSP/ASP will be created for access to IRP.

Q. 88. Will NIC provide new APIs for e-way bill?

No. E-way bill system will continue to function as it is. No new APIs for e-way bill are required to be published.

L. e-Invoice – Resources, Help & Feedback

Q. 89. I want to know more about e-invoicing. Where can I find the material?

Please go through ‘e-invoice – Detailed Overview’

Q. 90. Are there any awareness videos available on e-invoicing?

Yes. Many awareness videos on e-invoice are available at ‘e-invoice’ play list on GSTN’s YouTube Channel

Q. 91. What are the channels of help and feedback for e-invoicing?

For any technical issue with APIs/Sandbox/e-invoice portal/Offline Utility etc., please raise a ticket with GST Self-Service Portal

Any other feedback & suggestions on e-invoice are welcome at e-invoice@gstn.org.in

*****

What if 1 invoice IRN is generated after 30 days.

If a supplier deals in both taxable and non taxable supplier then is it mandatory for him to generate irn for non taxable supply.

Please guide us