In this article we are going to discuss about Intermediary Services under GST

Generally, a common person thinks that if a transaction is carried out with the Entity/Customer outside India then it is ‘Export of Services’ and it does not attract GST. However, GST liability may arise if a transaction is categorized as ‘Intermediary’ Services.

Hence, it is important to understand the concept of Export of services and Intermediary service and thereafter analyze a particular transaction.

Let us first discuss about what is Export of Services –

In common parlance, export of services means when the supplier of service is located in India and the place of supply of service is outside India.

However, as per Section 2(6) of the IGST Act, 2017, supply of service qualifies to be an export of services if it fulfills the following conditions:

> The service is supplied from India to a recipient located outside India,

> The place of supply of service is outside India,

> The consideration for the service is received in freely convertible foreign exchange or in Indian rupees wherever permitted by the Reserve Bank of India, and

> The transaction is between separate entities, i.e. not merely between two establishments of an entity.

Export of services are treated as Zero rated supply i.e. the goods and services exported outside India shall be relieved of GST levied upon them – either at the input stage or at the final product stage. Therefore, exporter of services is not liable to pay tax under GST.

Let us now discuss Intermediary services –

Definition u/s 2(13) of the IGST Act, 2017 – “Intermediary means a broker, an agent or any other person, by whatever name called, who arranges or facilitates the supply of goods or services or both, or securities, between two or more persons, but does not include a person who supplies such goods or services or both or securities on his own account.”

Circular No. 159/15/2021-GST dated September 20, 2021, lays down primary requirements for intermediary services:

1. Minimum of Three Parties: An intermediary essentially “arranges or facilitates” another supply between two or more other persons and, does not himself provide the main supply. The arrangement requires a minimum of three parties, two of them transacting in the supply of goods or services or securities and one arranging or facilitating the said main supply. An activity between only two parties can, therefore, NOT be considered as an intermediary service.

2. Two distinct supplies: Two distinct supplies involved in ‘intermediary’ is Main supply and Ancillary supply.

-

- Main supply – Supply between the two principals, which can be a supply of goods or services or securities.

- Ancillary supply – Supply which is the service of facilitating or arranging the main supply between the two principals. It is supply of intermediary service and is clearly identifiable and distinguished from the main supply.

3. Intermediary service provider to have the character of an agent, broker or any other similar person: Definition of “intermediary” itself stipulates intermediary as a broker, agent or any other person facilitating or arranging the services. The word ‘means’ in the definition is not inclusive and does not expand the definition to include any other person. The phrase “arranges or facilitates” specifies that intermediary services are only supportive services.

4. Does not include a person who supplies such goods or services or both or securities on his own account: It excludes a person who supplies such goods or services, or both or securities on his own account. If the person supplies the main supply, either fully or partly, on principal to principal basis, then the said supply cannot be covered under the scope of “intermediary”.

5. Sub-contracting for a service is not an intermediary service: Sub-contracting means delegating certain responsibilities to specialized service providers or entities to leverage their expertise and resources in order to achieve business goals effectively. The main supplier of goods or services or both can outsource the main service, fully or partly, to sub-contractor. Such sub-contractors provides the main supply, either fully or part thereof, and does not merely arrange or facilitate the main supply between the principal supplier and his customers, and therefore, clearly is not an intermediary.

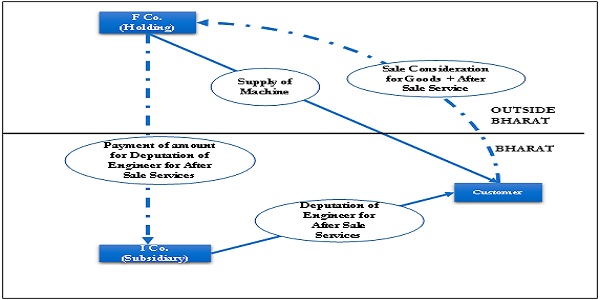

Let us understand with the help of an example:

F Co. (Holding Company) is supplying a machine to a customer in India.

> I Co. (Subsidiary Company of F Co.) deputes engineers to provide after sales services to the customer.

> The customer pays the consideration for supply of machine & after sale services to F Co.,

> F Co. then remits the amount to I Co. towards the services for deputation of Engineer for providing After Sale Services.

ANALYSIS:

1. There are 3 parties involved in the transaction.

2. Need to understand whether the service provided by I Co. is

i. Ancillary supply;

ii. Sub-contracting, or

iii. As principal to principal supply.

> Considering that I Co. is facilitating supply i.e. facilitating after sales services, it will get covered under ‘Intermediary Services’.

> Further, following other points will needs to be analysed:-

> whether I Co. is performing as an agent or principal,

> whether I Co. is bearing any risk associated with default in after sale services (it will have to be understood).

> If ‘sub-contracting’ or ‘principal to principal’ is triggered then it may come out of ‘intermediary’ service

> Further, agreement between F Co. & I Co. needs to be seen or drafted accordingly

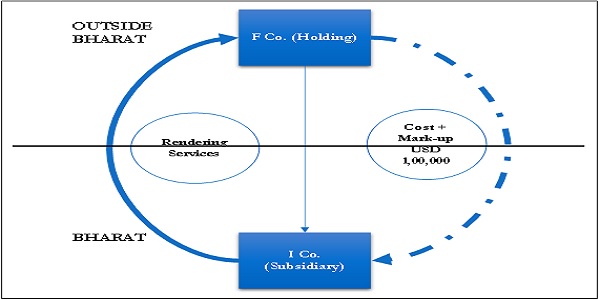

- I Co. (Subsidiary Company) provides services of software development to F Co. (Holding Company). F Co. pays I Co. $ 1,00,000 for the service rendered on cost + profit basis.

- The transaction is between separate entities, i.e. F Co. and I Co. are different and are two separate legal entities.

- Service is supplied from India to a recipient located outside India, the place of supply of service is outside India as per section 11 of IGST Act and the consideration for the service is received freely convertible foreign exchange.

ANALYSIS:

- The transactions to be termed as Intermediary Services should have minimum three parties, two distinct supply , intermediary should have the characteristics of agent, broker, the supply should not be on principal to principal basis & it should not be a sub contract.

- Given the aforementioned details, the transaction between F Co. & I Co. shall be termed as Export of services not as Intermediary Services as it does not satisfies the requirement of Intermediary services

Pauser:

1. If directors of I Co. are residing in United States and controlling entire operation of I Co. from US then, can it be considered that F Co. has its own establishment in India & I Co. is not a separate legal entity.

2. Linking Intermediary services with Permanent Establishment or Business Connection under Income Tax.

If GST officer determines a transaction as ‘Intermediary Services’ or lets say client has taken conservative position of considering transaction as ‘intermediary’ service and decided to pay GST of 18%. Then, whether such position will be detrimental from perspective of Income Tax i.e. with respect to having fixed places in India Or business connection in India.

******

I thank Mr Sujal Shrivastav (CA Final Student) for preparing this article.

Compiled by:

Mr. Sujal Shrivastav

January 3, 2024

Source: IGST Act, Circular No. 159/15/2021-GST

For further information, contact us on +91 9833 88 44 64 or utkarsh.m@cauma.in / sujal.s@cauma.in.

Disclaimer: The information contained herein is of a general nature and does not contain any expert view or opinion. Please refer source documents for detailed information. Although we try to provide accurate information, there can be no guarantee that such information is accurate as of the time it is received or in the future. We request readers to seek professional advice before arriving at any decision / conclusion after reading of this document. We are not responsible for any loss arising to anyone after referring and relying on this document.