Bhawna Sadhwani

E-Invoice or electronic Invoice is a system in which B2B/ Credit Note/ Debit Note & Exports Invoices are authenticated electronically by GSTIN portal. Said Invoices are transmitted to GSTIN portal & an Identification Number will be issued against the Invoice which is known as ‘Invoice Reference Number’ or ‘IRN’ Number.

Applicability of E-Invoice :-

| Sr Num | Aggregate Turnover limit in any of the preceding | Applicable date |

| Financial Year | ||

| 1 | Turnover > 500 crore | 01.10.2020 |

| 2 | Turnover > 100 crore | 01.01.2021 |

| 3 | Turnover > 50 crore | 01.04.2021 |

| 4 | Turnover > 20 crore | 01.04.2022 |

Interpretation- Once E-Invoicing is applicable to a particular taxpayer, it will be applicable for lifetime. Example:- A registered person having following turnover in below FY

| Financial Year | Aggregate Turnover of Registered Person A |

| 2017-18 | 25 crore |

| 2018-19 | 18 crore |

| 2019-20 | 19 crore |

| 2020-21 | 15 crore |

| 2021-22 | 16 crore |

In above example as we can see that the Aggregate turnover of A in FY 2017-18 was above the prescribed limit of 20 crore & hence E-Invoice will be applicable to Registered Person “A” from 01.04.2022.

Now, Let us examine what is Aggregate Turnover?

As per section 2(6) of CGST Act, 2017 Aggregate Turnover =

- All Taxable Supplies;

- Exempt Supplies;

- Export of Goods or Service or both;

- Inter-state supplies of person having same PAN (i.e Entity with same PAN in different state)

On PAN India level and excluding Central tax, State tax, Union territory tax, Integrated tax and Cess.

Lets analyse above definition:- Suppose an Enterprises having registration in Gujarat and Rajasthan. The said Enterprises have its manufacturing unit in Gujarat & whatever Goods are manufactured are transferred to Rajasthan for further Supply to ultimate customers.

| Supply from | Amount |

| Gujarat to Rajasthan (Inter-company transfer) | 15 crore |

| Rajasthan to Ultimate Customer (Sales) | 20 crore |

Actual Turnover – 20 crore & Aggregate Turnover is 35 crore. E-Invoicing will be applicable to the said Enterprises. Exemption from E-Invoicing irrespective of Turnover Limit:-

As per Amended Notification 13/2020 dated 21.03.2020, E-Invoice is not applicable for below Registered Person:-

- SEZ Unit;

- Insurance or Banking company including NBFC;

- GTA;

- Passenger transport;

- Admission to exhibition of cinematograph films in multiplex screens;

- Government Department or Local Authority

Cancellation of E-Invoice:- Once E-Invoice is generated, it can be cancelled within 24 hours of its generation.

Manner of Issuing Invoice:- As per Rule 48(5), Any Registered Person (to whom E-Invoice is applicable) is issuing Invoice other than manner prescribed for E-Invoice, then such Invoice will not be treated as Invoice.

Credit Eligibility to Recipient:- A supplier, to whom E-Invoice is applicable issuing Tax Invoice rather than E-Invoice then the recipient will not be eligible to take credit on the said Tax Invoice issued by the Supplier. Rule 46 (Tax Invoice) is amended to insert clause ‘® prescribing the condition of having QR code on Invoice having embedded IRN Number.

Interpretation:- Only an E-Invoice can be considered as Valid document for availment of Input tax credit.

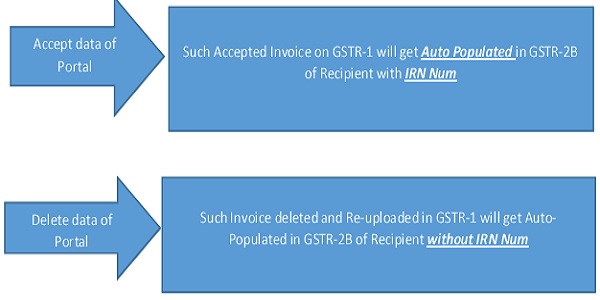

How Portal works with IRN?

When IRN is generated, that Invoice is reported to GST Common Portal through NIC. Below are the options for filing GSTR-1.