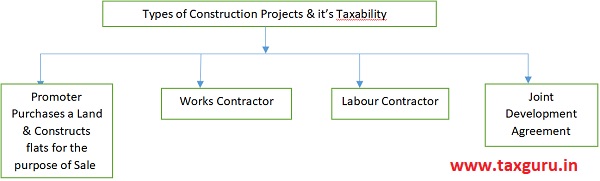

Article explains Implications of GST on Real Estate Sector. It explains GST when Builder Purchases a Land and Constructs flats for the purpose of Sale, Joint Development Agreemen, Supply of Constructed Flats by Promoter to Land Owner, Supply of constructed Flat by Promoter to Outsiders, Amendments in GST in Real Estate Sector (w.e.f. 01-04-2019), Reverse Charge Mechanism on Real Estate sector (w.e.f. 01-04-2019, Example On Joint Development Agreement, Supply of land by land Owner to Promoter, Joint Development Agreement.

Real Estate Sector

Page Contents

- Builder Purchases a Land and Constructs flats for the purpose of Sale:-

- Joint Development Agreement:-

- Supply of land by land Owner to Promoter:-

- Supply of Constructed Flats by Promoter to Land Owner:-

- Supply of constructed Flat by Promoter to Outsiders:-

- Amendments in GST in Real Estate Sector (w.e.f. 01-04-2019):-

- Reverse Charge Mechanism on Real Estate sector (w.e.f. 01-04-2019):-

- Example On Joint Development Agreement:-

Builder Purchases a Land and Constructs flats for the purpose of Sale:-

a. Sale After Completion of Construction:-

No GST Liability, as the aforesaid service is covered under Schedule-III Negative List of Services

b. Sale Before Completion of Construction:-

GST Liability Exists:-

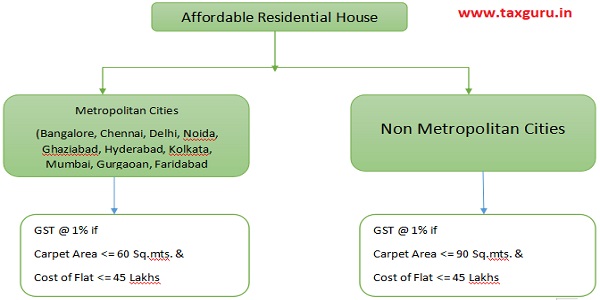

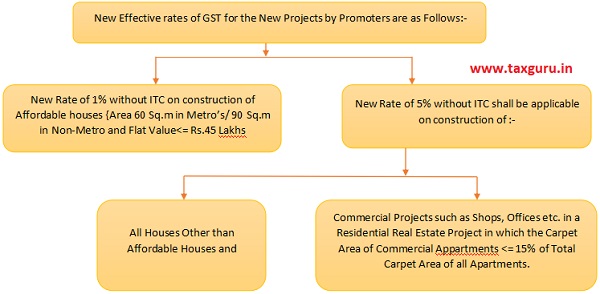

1. Taxable @1%:-

Applicable to Affordable Residential Houses

No Input Tax Credit is available in this case.

2. Taxable @5%:-

Applicable to Non Affordable Residential Houses and Commercial House but which is a part of Residential Real Estate Project (i.e where Commercial Carpet area <= 15% of Total Carpet Area)

No Input Tax Credit is available in this case.

In both the above cases (1) & (2) Rule 42 of CGST Rules (i.e Methodology of Apportionment of credit on Inputs and Input Services and reversal of Ineligible credit) has to be applied.

3. Taxable @12%:-

Applicable to Commercial Complex.

Input Tax Credit is available in these cases.

Note:- The above said Tax Rates 1%/5%/12% are excluding land value which is 1/3rd of the Total Value as said in Notification No.11/2017.

Works Contractor:-

- Means a person who provides construction services without purchase of Land.

- In these cases Material and Labour cost is incurred by the contractor himself and he adds a reasonable profit to the cost incurred by him which will be the value of taxable supply.

GST Liability Exists:-

a. Taxable @12%:-

Applicable to Affordable Residential Houses

b. Taxable @18%:-

Applicable to Non Affordable Residential Houses

In both the above cases ( a ) & (b) Input Tax credit is available.

Labour Contractor:-

- Means a contract which involves a pure supply of Man power.

Taxability:-

a. For Single residential Unit:-

This service is purely Exempt [Notification No.12/2017].

b. In any other Case:-

Is liable to tax @ 18%

Common Notes:-

- Meaning of Affordable Residential House:-

Joint Development Agreement:-

Joint Development Agreement is a case where the Promoter enters into agreement with the Land Owner, where the Land Owner supplies his land to the Promoter while in return the Land owner gets some Constructed Flats on his land along with cash consideration (if any).

In these cases generally 3 supplies are involved:-

1. Supply of land by land Owner to Promoter.

2. Supply of Constructed Flats by Promoter to Land Owner.

3. Supply of constructed Flat by Promoter to Outsiders.

Supply of land by land Owner to Promoter:-

- Transfer of Development right shall be regarded as Supply (i.e Assignment of Right to Use of Land by Land Owner to Promoter), but this supply is Exempt supply (Entry No. 41 A/B; Notification No.04/2019)-Notification given below.

Supply of Constructed Flats by Promoter to Land Owner:-

- This is a Supply of service by Promoter to Land Owner.

- Value Of Supply of Service = Stamp Duty Value (SDV) of flats constructed by Promoter to Landowner.

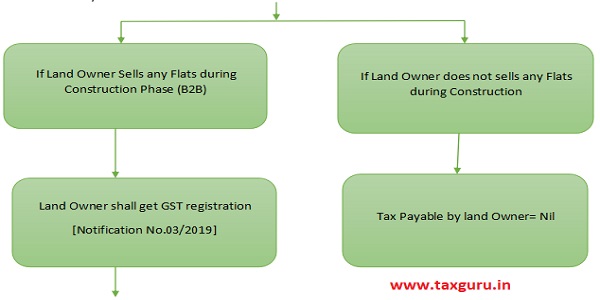

- GST Liability on Flats given by Promoter to Land Owner has to be paid irrespective of sale of Flats by land Owner to his Customers.

Tax Payable by Land Owner:-

Sale Consideration* 1%/5%/12%

(-) ITC on Tax paid by Promoter

Net Payable

Supply of constructed Flat by Promoter to Outsiders:-

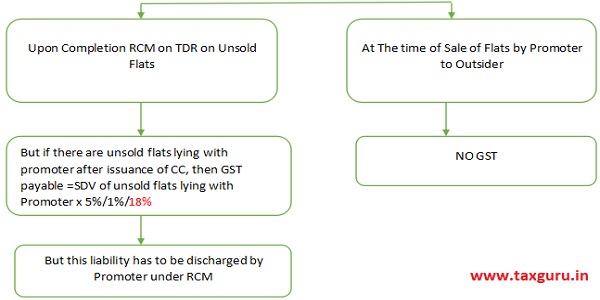

1. During Construction Phase:-

Sale of Flats by Promoter to Outsiders is liable to GST (@1%/5%/12%)

2. On Completion of Construction:-

Note:-

a. In short GST has to be payable on all Flats Constructed by Promoter on the Land belonging to Land Owner on which JDA has been entered into. (Refer Example Below)

b. For Commercial Project GST is applicable @12% (i.e 2/3rd of 18%), but in the FAQ’s released by MOF dated 07-05-2019 (F.No. 354/32/2019-TRU) it is said that TDR on Commercial Projects flats which remained unsold on the date of Completion of project, GST on such TDR has to be paid @18% instead of 12%.

Amendments in GST in Real Estate Sector (w.e.f. 01-04-2019):-

Earlier, the effective rate of GST on real estate sector was 8%/12% with ITC. With effect from 01.04.2019, the effective rates of GST for the new projects have been brought down to a large extent.

However, the promoters/builders have been given a one-time option to continue to pay tax at the old rates on ongoing projects (buildings where construction and actual booking both have started before 01.04.2019) which have not been completed by 31.03.2019.

Conditions for Applicability of above said Tax Rates:-

1. Input Tax Credit shall not be Available.

2. 80% of inputs and input services used in supplying the service shall be purchased from registered Persons. In case of shortfall, RCM u/s 9(4) @ 18%. However on cement @ 28%.

Moreover, GST on capital goods shall be paid by the promoter on reverse charge basis, u/s 9(4) of the CGST Act at the applicable rates.

3. Promoter i.e, Builder is liable to pay GST on construction of houses w.r.t. Landlord share.

4. Upon completion of construction, TDR on unsold portion is liable to GST , but under RCM i.e., Tax to be paid by Promotor (Builder).

- Upon Completion of Construction Promoter has to Apply Rule 42 (i.e Methodology of Apportionment of credit on Inputs and Input Services and reversal of Ineligible credit) for each project separately.

- Exemptions in Notification 12/2017 (w.e.f. 01-04-2019):-

a. Service by way of transfer of development rights (herein refer TDR) or Floor Space Index (FSI) (including additional FSI) on or after 1st April, 2019 for construction of residential apartments by promoter in a project (Provided that the promoter shall be liable to pay tax at the applicable rate, on reverse charge basis {Notfn No.04/2019}).

b. Upfront amount (called as premium, salami, cost, price, development charges or by any other name) payable in respect of service by way of granting of long term lease of thirty years, or more, on or after 01.04.2019, for construction of residential apartments by a promoter in a project (Provided that the promoter shall be liable to pay tax at the applicable rate, on reverse charge basis)

Reverse Charge Mechanism on Real Estate sector (w.e.f. 01-04-2019):-

| Description Of Service | Tax Payable by |

| Services supplied by any person by way of transfer of development rights or Floor Space Index (FSI) (including additional FSI) for construction of a project by a promoter on unsold flats by Promoter (However RCM is to the extent of unsold portion) | Promoter |

| Long term lease of land (30 years or more) by any person against consideration in the form of upfront amount (called as premium, salami, cost, price, development charges or any other name) and/or periodic rent for construction of a project by a promoter on unsold flats by Promoter (However RCM is to the extent of unsold portion) | Promoter |

Example On Joint Development Agreement:-

M/s.Krishna Developers Ltd(herein after called Promoter) entered into Joint Development Agreement with Mr.Arjuna(herein after called land Owner) to construct 100 flats on the land owned by Mr.Arjuna and in return for the service provided by Mr.Arjuna, he is entitled to receive 40 flats from M/s.Krishna Developers Ltd .

Date on which JDA Agreement entered was: 30-06-2019

Date on which the Project is Completed was: 02-05-2021 (say)

GST Implications are as follows:-

On the 40 Flats provided by Promoter to Land Owner, promoter is liable to pay GST on Completion of Construction or Sale of flats by land owner whichever is earlier (as per Notfn No.06/2019) @ SDV of flats on the date when the agreement is entered into between Arjuna and M/s.Krishna Developers Ltd (i.e 30-06-2019).

Suppose out of 40 flats, 30 flats were sold under construction phase (06-05-2020), the GST liability on these 30 flats were to be discharged on the date when the land owner sold them to his Customers (06-05-2020) at the value of SDV as on 30-06-2019. In this case Mr.Arjuna has to get himself registered under GST and claim the ITC of tax paid by M/s.Krishna Developers Ltd on those 30 Flats (as per Notfn No.03/2019).

For remaining 10 flats M/s.Krishna Developers Ltd has to discharge his GST liability on Completion of Construction (i.e 02-05-2021) @ value of flats on 03-06-2019.

While coming to the flats retained by M/s.Krishna Developers Ltd (i.e 60 Flats):-

For Suppose out of those 60 flats, 45 flats were sold during the construction phase then the promoter has to discharge the tax liability on those 45 Flats @SDV on the date they are sold (i.e Forward Charge)

For Remaining 15 flats which remained unsold as on the date of Certificate of Completion is received they are covered under Schedule-III and are exempt from GST. But the promoter has to pay GST on TDR provided by Arjuna to M/s.Krishna Developers Ltd for these 15 flats @ SDV on the date on Completion of Project (02-05-2021) as per Notfn No.05/2019 & 04/2019 under Reverse Charge Mechanism (Sec.9(3)).

{Note:- Hence in JDA, GST is to be payable on ALL THE FLATS whether retained by the promoter himself or on those given to Land owner}.

Author Bio

Whether labour charges used in construction of real estate project, considered in 80% Inputs & input services or not. please clarify.

Most of construction expenses are incurred on labour.