Job Work under CGST Act, 2017

Introduction:-

In the age of outsourcing, it is common to get certain operations done from another person. This latter person may carry out either a part of the process allowing its completion by another person or by the person sending the goods or May himself complete the goods. Such operations are called Job Work operations.

The person sending the goods is known as “Principal” and that carrying out the operation is known as ‘Job worker’.

The GST Law makes special Provisions with regard to the removal of Goods for Job Work and receiving back the goods after processing from the Job-worker without the Payment of GST. The benefit of these provisions shall be available both to the Principal and the Job Worker.

Definition:-

Section 2(68) of the CGST Act, 2017 defines job work to mean as ‘any treatment or process undertaken by a person on goods belonging to another registered person’. Thus, the job worker is expected to work on the goods sent by the principal and whether the activity is covered within the scope of job work or not would have to be determined on the basis of facts and circumstances of each case.

Ownership of the goods does not transfer to the job worker, but it rests with the Principal.

The job worker, in addition to the goods received from the principal, can use his own goods for providing the services of job work. As held in Prestige Engineering (India) Limited v Commissioner of Central Excise, Meerut [1994 (73) ELT 497 (SC), addition or application of minor items by the job worker would not detract from the nature and character of his work.

Supply of Job Work Services:-

Job worker as a supplier of Service, is liable to pay GST if he is liable to be registered. He shall issue an invoice at the Time of Supply of the Service as determined under Section 13 read with section 31 of the CGST Act.

Value of services would be determined in terms of Sec.15 of CGST Act and would include not only service charges but also the value of any Goods or services used by him for supplying the Job work services, if recovered from the Principal.

Question arises as to whether the value of Moulds, Jigs, dies and fixtures or tools which have been provided by the Principal to the Job worker and have been used by the latter for providing Job work services would be included in the value of Job work services?

Ans:- Sec.15(2)(b) of the CGST Act stipulates that any amount that the supplier is liable to pay in relation to the supply but which has been incurred by the recipient will form part of the Valuation for that particular Supply, provided it has not been included in the price for such supply.

Accordingly it is clarified that the value of such moulds, dies, jigs and fixtures or tools may not be included in the value of job work services provided its value has been factored in the price for the supply of such services by the Job worker.

Provisions relating to the Job work are covered in the sections 19 & 143 of CGST Act, 2017.

Job Work Procedure:-

It is to note that the provisions of said section are applicable to a registered person. Thus a Principal, who can send the goods for Job work under the said provisions must be a Registered Person.

Provisions of Sec.143 are as follows:-

Principal can send Goods to Job Worker without payment of Tax:-

- A registered person (Principal) is allowed to send Inputs/Capital Goods without payment of Tax to a Job worker and from there to another Job worker and after completion of job-work bring back such goods without payment of tax. Such goods need to be removed under intimation and subject to certain conditions.

- Principal is not required to reverse the ITC availed on Inputs/Capital Goods dispatched to Job worker.

- Principal can also send Inputs/Capital goods to the Job worker without bringing them to his premises and can still avail the credit of tax paid on such Inputs/Capital goods.

- After processing of goods, the Job worker may clear the goods to:-

1. Another Job worker for further processing, or

2. Dispatch the goods to any of the place of business of the principal without payment of Tax.

Supply of Goods directly from Job worker’s place of Business/Premises:-

- After processing of goods, the principal also has the option to clear the goods, directly from job-workers premises, on payment of tax within India or without payment of tax for export outside India on fulfillment of conditions.

- The facility of supply of goods by principal to third party directly from the premises of job-worker, on payment of tax in India likewise with or without payment of tax for export, may be availed by principal on declaring premise of the job-worker as his Additional Place of Business in registration. However, such declaration is not required by principal where:

♦ Job worker is registered under section 25 or

♦ Principal is engaged in supply of notified goods.

- In such cases, the supply of goods will be regarded as supply by the Principal and not the job worker. Resultantly, it is clarified that the time value and place of supply would have to be determined in the hands of the principal irrespective of the location of the job workers place of business. Further, the invoice would have to be issued by the principal. It is also clarified that in case of exports directly from the job workers place of business, the LUT or bond as the case may be, shall be executed by the principal. These principles would apply mutatis mutandis in case of supply of waste and scrap generated during Job work. [Circular No.38/12/2018]

Procedure for sending goods to Job worker:-

- Before supply of goods to the job worker, the principal would be required to send intimation to the jurisdictional officer containing the details of the description of Inputs intended to be sent by the principal and the nature of processing to be carried out by the job worker. The said intimation shall also contain the details of the other job workers, if any.

- The Inputs/Capital goods shall be sent to the job worker under the cover of a challan issued by the Principal. The challan shall be issued even for the Inputs/Capital goods sent directly to the job worker.

Responsibility for keeping accounts for Inputs/Capital Goods:-

- Responsibility for keeping proper accounts of the Inputs/Capital Goods lies with the Principal.

Goods not received within the stipulated time Deemed as Supply:-

- In case the Inputs/Capital goods are not received back or not supplied from the Job worker’s premises, within specified time limit. It shall be deemed to be a supply from principal to the job worker from the day when it was sent for job work. Accordingly, the principal would be liable to tax along with Interest.

- Thus, goods sent for job work acquire the character of supply when the Inputs/Capital goods sent for job work are neither received back by the principal nor supplied further by the Principal from the place of business/premises of the job worker within 1/3 year/extended time period, of being sent out.

- It may be noted that the responsibility for sending goods to the job worker as well as bringing them back or supplying them has been cast on the Principal.

- In such cases where the Inputs/Capital goods are neither returned nor supplied from the job worker’s place of business/premises within the specified time period, the principal would issue an invoice for the same and declare such supplies in his return for that particular month in which the time period of 1/3 or extended time period has expired.

- Date of Supply: Date of supply shall be the date on which such Inputs/Capital goods were initially sent to the job worker. Further interest for the intervening period shall also be payable on the tax.

- If such goods are returned by the job worker after the stipulated time period, the same would be treated as supply by the job worker to the Principal and the job worker would be liable to pay GST if he is liable for registration in accordance with the provisions of the CGST Act and the rules made there under.

- The above provisions will not be applicable in case of moulds, Jigs, dies and fixtures etc.

Taking INPUT TAX CREDIT in respect of Inputs/Capital goods sent for Job Work (Sec.19):-

Sec.19 deals with ITC on Inputs/Capital Goods sent for Job work.

I. Credit on goods sent for Job work [sec.19(1), (2), (4) & (5)]:-

- A principal is entitled to take the credit of input tax paid on Inputs/Capital goods sent to the job worker for job work.

- Principal can also take ITC even when the Inputs/Capital goods have been directly sent to the Job worker without being brought into his premises. The principal need not wait till the Inputs/Capital goods are first bought to his place of business.

*Job worker is also eligible to avail ITC on inputs etc. used by him in supplying the job work services if he is registered [Circular No.38/12/2018].

II. Time limit for the return of goods sent for Job work or supply from job workers place of business:-

- Inputs and Capital goods sent for job work should either be returned to the Principal or must be supplied from the job workers premises within 1/3 years respectively from sending them to the Job worker.

- If the above time lines are not met, it is deemed that the Inputs/Capital goods were supplied by the principal to the Job worker on the day they were sent out to the job worker.

*The above said supply is required to be declared in GSTR-1 and the principal is liable to pay tax along with applicable Interest.

III. Special procedure for sending goods for Job work:-

Procedure for sending the goods for Job work, in accordance with rule.45 read with Circular No.38/12/2018:

a) Where goods are sent by Principal to only one Job worker:

- Principal has to send the Inputs/Capital goods to the job worker under the cover of a Delivery Challan issued by him (rule 55).

- Principal shall prepare in Triplicate, the challan in terms of rule 45 & 55, for sending the goods to a Job worker. The job worker should send one copy of the said challan along with goods, while returning them to the Principal.

- Further, the Principal would be required to send the intimation to the Jurisdictional Officer. Form GST ITC-04 will serve as the Intimation.

b) Where goods are sent from One job worker to another job worker:

- In such cases, the goods may move under the cover of a challan issued either by the Principal or the Job worker.

- Alternatively, the challan issued by the principal may be endorsed by the job worker sending the goods to another job worker, indicating therein the quantity and description of goods being sent.

- Same process may be repeated for subsequent movement.

c) Where the goods are returned to the Principal by the job worker:

- Job worker should send one copy of the challan (as received by him from the principal) while returning the goods to the principal after carrying out the job work.

d) Where the goods are sent directly by the supplier to the job worker:

- In this case, the goods may move from the place of business of the supplier to the place of business/premises of the job worker with a copy of invoice issued by the supplier in the name of the buyer (i.e. Principal). Job workers name and address should also be mentioned as the consignee in such invoice.

- Further the buyer shall issue the challan and send the same to the job worker directly.

- In case of Import of goods by the principal which are then supplied directly from the custom station of import, the goods may move from the customs station of import to the place of business/ premises of the job worker with a copy of the Bill of entry and the principal shall issue the challan under rule 45 and send the same to the job worker directly.

e) Where goods are returned in piecemeal by the Job worker:

- In case the goods after carrying out the job work, are sent in piecemeal quantities by a job worker to another job worker or to the principal, the challan issued originally by the principal cannot be endorsed and a fresh challan is required to be issued by the job worker.

f) Submission of Intimation:

- It is clarified that it is the responsibility of the Principal to include the details of all the challahs relating to goods sent by him to one or more job worker or from one job worker to another and its return therefrom during a quarter in form GST ITC-04 by the 25th day of the month succeeding the relevant quarter.

- For example, for Oct-Dec quarter, the due date is 25 Jan.

g) Requirement to generate E Way Bill:

- Shall be generated either by the principal or by the registered job worker irrespective of the value of the consignment, where goods are sent by a principal located in one State/UT to a job worker located in any other State/UT [Rule 138 of CGST rules].

- Further the E Way bill shall be generated by the principal, wherever required, in case the job worker is unregistered.

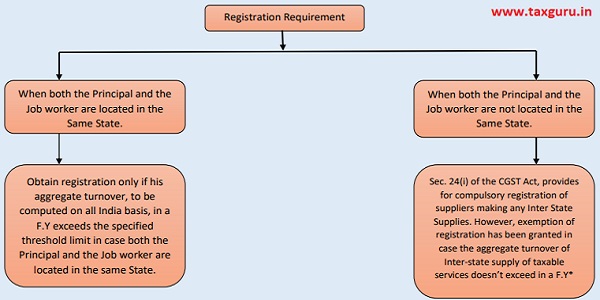

Registration requirements:-

*Therefore, it is clarified that a job worker, being a supplier of service, is required to obtain registration only in cases where his aggregate turnover, to be computed on all India basis, in a F.Y exceeds the threshold limit regardless of whether the principal and the job worker are located in the same state or different state.

Value of Goods, after completion of Job work, supplied directly from the premises of the registered job worker not to be included in its Aggregate Turnover:-

- As discussed earlier, principal can supply the goods directly from the premises of the job worker without bringing it back to his own premises. It is clarified that the supply of goods by the Principal from the Place of Business/Premises of the job worker will be regarded as Supply by the Principal and not by the job worker.

- Therefore, the value of such goods supplied will be included in the aggregate turnover of the Principal and not Job worker.

Transitional Provisions:-

1. This applies for items removed for job work before GST and returned on or after GST implementation.

2. No tax will be payable if the following conditions are satisfied:

- The goods are returned to the factory within 6 months from 1 July (i.e. by 31 Dec 2017) (extendable for a maximum period of 2 months).

- Goods held by job worker is declared in Form TRAN-1.

- The principal manufacturer can sell off the items under job work only after paying required taxes (Excise & VAT if before GST; if he sells after 1 July 2017, then GST applies). This rule does not apply to goods exported out of India within 6 months from the appointed date (extendable by not more than 2 months).

3. If the goods are not returned within the time period then ITC will be recovered from the principal manufacturer.

Author Bio