The taxation of corporate and personal guarantees under the Goods and Services Tax (GST) framework has long been a subject of debate and uncertainty. Companies often issue guarantees for loans obtained by their subsidiaries to safeguard investments. Additionally, directors of companies sometimes provide guarantees for loans in their personal capacity as part of their routine business operations. A recent ruling by the Supreme Court brought some clarity to this issue. In this article, we will explore the taxability of these guarantees under GST and delve into the Supreme Court’s decision and GST Council recommendations.

Detailed Analysis

Supreme Court Ruling: In a recent decision, the Supreme Court clarified that the issuance of a corporate guarantee to a subsidiary company would not attract service tax if provided without consideration. However, the landscape changed with the introduction of GST. Under Schedule I of the Central Goods and Services Tax (CGST) Act, 2017, the supply of goods or services among related entities, in the course of business and without consideration, qualifies as a supply, thereby subject to GST.

CGST Act Provisions: Section 15(5) of the CGST Act empowers the government to determine the value of certain supplies. This provision plays a crucial role in determining the taxability of corporate and personal guarantees.

GST Council Recommendations

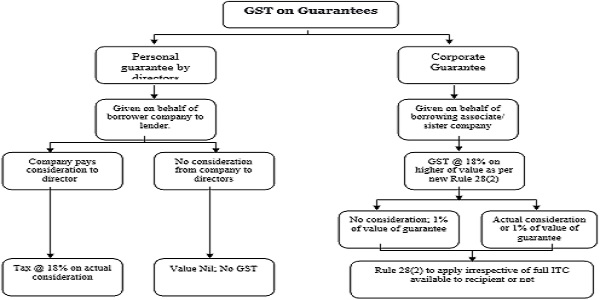

- GST Council in its 52nd Council meeting held on 7th October, 2023 clarified / recommended on taxation of guarantees given by corporates and directors in their individual capacity.

- Personal guarantees given by directors to banks / financial institutions for corporate borrowings on behalf of company

- Where company pays consideration to director in any form – directly or indirectly – to be taxed at open market value.

- Where no consideration is involved – value to be considered as zero and no tax payable

- Corporate guarantee on behalf of related parties / subsidiaries

- To be taxed on taxable value as per new Rule 28(2) in CGST Rules, 2017 @ equal to one percent of value of guarantee on actual consideration, whichever is higher, irrespective of whether full ITC is available to the recipient or net.

- To be taxed @18@GST

- Prospective in operation

In view of GST Council’s recommendation, corporate guarantees given in favour of related parties will be liable for 18 percent goods and service tax (GST) on 1 percent of the amount guaranteed or on the actual consideration, whichever is higher. However, personal guarantees offered by the promoters or directors of the company shall not attract tax. The move on implementation is expected to resolve conflicts on levying GST on personal and corporate guarantees between related parties.

Conclusion

The recent clarification by the Supreme Court and the subsequent recommendations by the GST Council provide much-needed clarity on the taxation of personal and corporate guarantees under the GST regime. Personal guarantees offered by company directors for corporate borrowings are subject to tax if any consideration is paid by the company. Corporate guarantees for related parties are taxable, with the tax amount being one percent of the guaranteed value or the actual consideration, whichever is higher. These recommendations are expected to resolve ambiguities and disputes related to the taxation of guarantees between related parties and will have a prospective implementation. Understanding these regulations is crucial for businesses to ensure compliance with GST laws and to avoid potential tax liabilities.

Author Bio

Now that corporate guarantee would be a taxable service @ 18% on a deemed valuation of 1% of value of guarantee or actual consideration, whichever is higher, tax liability would be decided on the basis of place of supply. Since supply to SEZ would be considered as a zero rated, tax liability would be subject to provisions of export of services.

Will GST be applicable for corporate guarantee provided by holding company to its JV which has principle place of business in SEZ?

If the JV has presence in both DTA as well as SEZ, the corporate guarantee will be taxable to the extent of value belonging to the DTA GST registration of the JV.