TRANSITIONAL PROVISIONS

1. INTRODUCTION

1.1 This Chapter deals with the transitional provisions contained in CGST Act, 2017, to facilitate the taxpayers to take Input Tax Credit (ITC) on the CENVAT credit balance or CENVAT credit on goods in stock, etc. at the time of migration from the erstwhile Central Excise and Service Tax regime to GST regime. Presently the relevance of these transitional provisions is only academic, so as to deal with litigation, if any in this regard. The provisions of CGST Act, 2017 and CGST Rules, 2017, relevant to this Chapter are as under –

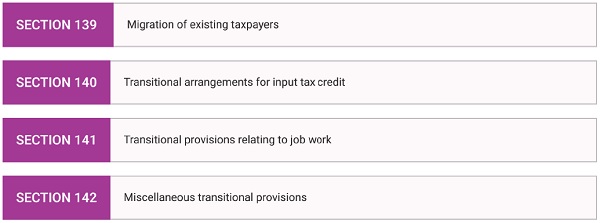

| Sr. No. | Section/Rules | Provisions pertaining to |

| 1 | Section 139 | Migration of existing taxpayers |

| 2 | Section 140 | Transitional arrangements for input tax credit |

| 3 | Section 141 | Transitional provisions relating to job work |

| 4 | Section 142 | Miscellaneous transitional provisions |

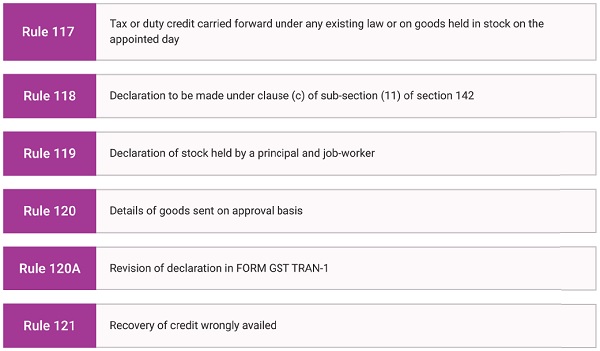

| 5 | Rule 117 | Tax or duty credit carried forward under any existing law or on goods held in stock on the appointed day |

| 6 | Rule 118 | Declaration to be made under clause (c) of sub-section (11) of section 142 |

| 7 | Rule 119 | Declaration of stock held by a principal and job worker |

| 8 | Rule 120 | Details of goods sent on approval basis |

| 9 | Rule 120A | Revision of declaration in FORM GST TRAN-1 |

| 10 | Rule 121 | Recovery of credit wrongly availed |

1.2 Prior to introduction of the Goods and Services Tax (GST), the Central Government, State Government and the Local Bodies like Municipal Corporations, etc. levied different types of indirect taxes, viz. Central Excise Duty, Service Tax, Sales Tax, Value Added Tax (VAT), Commercial Tax/Octroi, etc. The GST replaced multiple taxes levied and collected by the Centre and States by subsuming such different types of taxes into a single levy.

1.3 Availability of Input Tax Credit (ITC) of taxes paid on inputs, input services and capital goods for set off against the output tax liability is one of the key features of GST. This avoids cascading effect of taxes and ensures uninterrupted flow of credit from the seller to buyer. To ensure a seamless flow of input tax from the existing laws, viz. the Cenvat Credit Rules, 2004, Sales Tax/VAT law, into the GST regime, ‘Transitional arrangements for input tax credit’ were included in the CGST Act, 2017s to provide for the entitlement and manner of claiming input tax in respect of appropriate taxes or duties paid under the existing laws.

1.4 Transitional provisions are incorporated under GST to enable existing taxpayers to migrate to GST in a transparent and exact manner. It means that besides migrating from the Central Excise or Service Tax Registration to GST Registration, the amount of Cenvat Credit claimed on inputs, capital goods and input services carried forward in the last return filed for Central Excise and Service Tax immediately before the appointed day i.e. 01.07.2017, shall be transferred to the Electronic Credit Ledger of the taxpayer concerned, provided the amount of credit is admissible under the GST law. The transition provisions were more pertinent during the initial implementation of GST.

1.5 The concept of GST was completely new and many of the taxpayers were unaware of the provisions prevalent under GST for transition from old to new regime, which resulted in numerous litigation. A major concern for persons registered under GST is to make sure they don’t lose out on the tax benefits and input credits of the old regime.

1.6 These taxes may have been paid while purchasing, inputs, raw materials, semi-finished goods, finished goods, or on materials sent to job worker. For most taxpayers, these taxes were available as input credit till 30th June 2017, and moving the balance taxes to GST regime was important to take benefit of them by utilizing such credit towards discharge of GST on the supplies made during the GST regime. To help businesses transition smoothly and carry forward their input tax credit, the CBIC had released transition forms namely TRAN-1 and TRAN-2.

1.7 During the current scenario, transition provisions are significant only for the matters pending in litigation in different stages at Courts.

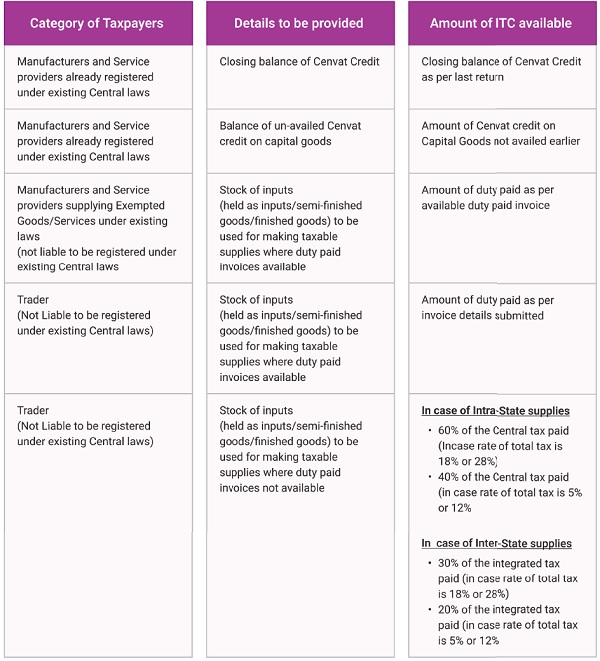

2. CATEGORY OF TAXPAYERS

The transitional provisions allow the following category of taxpayers to carry forward the Cenvat credit while migrating into the new regime.

3. TRANSITIONAL PROVISIONS FOR AVAILMENT OF INPUT TAX CREDIT

3.1 Closing balance of the credit in the last returns: The closing balance of the CENVAT credit /VAT in the last returns filed for the period ending 30.06.2017 under the existing law can be taken as credit in Electronic Credit Ledger. Such credit would be available only when the returns for the previous last six months have been filed under the existing law. In order to claim this credit, declaration in FORM GST TRAN-1 is required to be furnished on the common portal within ninety days from the appointed day i.e. 1st July, 2017 or within such extended time.

3.2 Unavailed credit on capital goods: The balance installment of unavailed Cenvat credit on capital goods can also be taken by filing the requisite declaration in the GST TRAN-1.

3.3 Credit on duty paid stock: A registered taxable person, other than manufacturer or service provider, may have duty paid goods in his stock on 1st July, 2017. GST would be payable on all supplies of goods or services made after the appointed day. The Government cannot collect tax twice on the same goods. Hence, in such cases, it has been provided that the credit of the duty/tax paid earlier would be admissible as credit. Such credit can be taken as under:

(i) Credit shall be taken on the basis of invoice evidencing payment of duty of Central Excise or VAT.

(ii) Such invoices should be less than one-year old.

(iii) Declare the stock of duty paid goods within prescribed time on the common portal.

3.4 Credit on duty paid stock when registered person does not possess the document evidencing payment of Central Excise duty/VAT: For such traders who do not have Central Excise or VAT Invoice, there was a scheme to allow credit to them on the duty paid stock. The features of this scheme are as under:

(i) The scheme was operative only for six months from 1st July, 2017. It was not available to manufacturer or supplier of service. It was available to traders only.

(ii) Credit @ 60% on such goods which attract Central Tax @ 9% or more and @ 40% for other goods of GST paid on such stock cleared after 1st July, 2017 was allowed. However, such goods should not be unconditionally exempted goods or taxed at ‘Nil’ rate under the GST law. It has also been provided that where Integrated Tax is paid on such goods, the amount of credit shall be allowed at @ 30% and 20%, respectively of the said tax.

(iii) Credit would be allowed after the GST is paid on such goods subject to the condition that the benefit of such credit is passed on to the customer by way of reduced prices.

(iv) A statement of supply of such goods in each of such tax period has to be submitted.

(v) Stocks stored should be easily identifiable.

3.5 Credit relating to exempted goods under the existing law but now taxable: Input Tax Credit of CENVAT / VAT in respect of input, semi-finished and finished goods in stock attributable to such exempted goods or services, which are now taxable can also be taken in the same manner.

3.6 Input/input services in transit: There might be a scenario where input or input services are received on or after the appointed day but the duty or tax on the same was paid by the supplier under the existing law. Registered person may take credit of eligible duties and taxes, provided the invoice has been recorded in the books within 30 days from 1st July, 2017. The period can be extended by the Commissioner of GST by another 30 days. A statement of such invoices have to be furnished. Input Service Distributor can also distribute such credit.

3.7 Tax paid under existing law under composition scheme: The taxpayers paying tax under the normal scheme of the earlier law has opted to pay tax under the Composition Scheme of the CGST Act, 2017, then the amount of CENVAT credit carried forward in a return will not be allowed to be carried forward if the person is paying tax under Composition Scheme. Even the unavailed amount of CENVAT credit on capital goods shall not be allowed to be carried forward under the CGST Act, 2017. In case, the taxpayer is switching over from the Composition Scheme to the normal scheme under the CGST Act, 2017, then he can take credit of eligible duties and taxes in respect of inputs held in stock, inputs held in semi-finished or finished goods, subject to the following conditions:-

(i) Such Input stock is used for taxable supply under this Act.

(ii) Registered person is not covered under Section 10 (Composition Scheme) of this Act. (Section 10 of CGST Act, 2017)

(iii) Registered person is eligible for ITC under this Act.

(iv) Registered person is in possession of such Invoice or other duty payment documents.

(v) Such Invoices are not more than twelve months old on appointed day.

3.8 ITC in case of Centralized Registration under Service Tax: Person holding centralized registration can take credit of the amount of CENVAT credit carry forwarded in return furnished under the existing law, if the original / revised return under the existing law has been filed within three months. Such credit may be transferred to any of the registered persons having the same PAN for which the centralized registration was obtained.

3.9 Reclaim the reversed Input Service credit: CENVAT credit reversed on account of non-payment of consideration within a period of three months can be reclaimed if payment is made to the supplier of service within three months from 1st July, 2017.

3.10 Capital goods belonging to the principal lying at the premises of the agent: This provision is specific to SGST law. In such cases, agent shall be entitled to take credit subject to the following conditions:

(i) the agent is a registered taxable person

(ii) both the principal and the agent declare the details of stock

(iii) the invoices are not earlier than twelve months

(iv) the principal has either reversed or not availed of the input tax credit.

4. TRANSITIONAL PROVISIONS RELATING TO JOB WORK, GOODS RETURNED/SENT FOR APPROVAL ETC.:

4.1 Job work:- Inputs, semi-finished goods or finished goods were sent to the job worker or any other premises without payment of duty/VAT under the existing law. No GST is payable by the job worker when such goods are returned by him within six months from 1st July, 2017. The period, on sufficient cause being shown, can be extended by the Commissioner, GST for a further period not exceeding two months. If not returned within the prescribed period, then ITC shall be liable to be recovered from the principal according to section 142 (8) (a) as per second proviso to section 141(1) of the CGST Act, 2017. In addition, the job worker will have to pay the GST on such supplies. In case of semi-finished goods, the manufacturer may transfer the goods to premises of a registered person without payment of tax within the prescribed period. In case of finished goods, the manufacturer may transfer the goods on payment of tax or clear for export within the prescribed period. (Section 141(1) of CGST Act 2017)

4.2 Goods removed before 6 months of the appointed day i.e. 1st July, 2017 but returned within 6 months from 1st July, 2017: If such goods are returned by an unregistered person, then refund of the duty/VAT paid under existing law can be claimed. If returned by a registered person, then return of goods shall be treated as supply of goods. ITC can be claimed.

4.3 Goods sent on approval basis before 6 months of the appointed day i.e. 1st July, 2017 but returned within 6 months from 1st July, 2017: No tax is payable by the person returning the goods. Commissioner may extend for a further period not exceeding two months. If returned after that, tax is payable if the supply is taxable under GST by the recipient. If not returned, tax is payable by the person who sent the goods on approval basis.

4.4 TDS deducted in VAT: A supplier had made sale of goods and tax was required to be deducted under VAT Act and Invoice was issued before the appointed day, however, the payment was made on or after appointed day. In such cases no TDS under GST is to be deducted.

4.5 Price revision in respect of existing contracts: In case of upward price revision, a registered person will issue a supplementary invoice or debit notes within 30 days from the date of revision and such revision shall be treated as supply under GST and tax is payable under this Act. In case of downward revision, registered person may issue credit note within 30 days from such revision and credit note shall be deemed to have been issued in respect of outward supply made under this Act. A registered person will reduce his tax liability for such credit note subject to reversal of credit by the recipient.

4.6 Proceedings under the existing laws: GST law has become operational w.e.f. 1st July, 2017 and existing laws have been repealed. Elaborate provisions have been made to save the pending as well future claims relating to existing law made before, on or after the appointed day i.e. 1st July, 2017. Such proceedings may pertain to refund claims of CENVAT credit/VAT or export related rebate or service tax, such proceedings may either result in recovery of tax or refund. All such cases would be disposed of under the existing law. If any claim for refund of CENVAT credit is fully or partially rejected, the amount so rejected shall lapse. Refund of CENVAT credit shall be paid in cash. There will be no refund of CENVAT credit if already carry forwarded. If any amount becomes recoverable, the same shall be recovered as arrear of tax under CGST Act, 2017.

5. STATUTORY PROVISIONS

The Statutory provisions relating to transition are contained in Chapter XX from Section 139 to 142 of the CGST Act, 2017, and Rule 117 to 121 of the CGST Rules, 2017.

5.1 Section 139 of CGST Act, 2017 provides for migration of existing taxpayers. (Section 139, 140 of CGST Act,

2017)

5.2 Section 140 of the CGST Act, 2017 contains provisions for transitional arrangements for input tax credit.

5.3 Section 140(1) of the CGST Act, 2017 provides that a registered person can avail CENVAT credit of eligible duties carried forward in the return under the existing law relating to the period ending with the day immediately preceding the appointed day, provided such credit is admissible as ITC under the CGST Act, 2017, the credit does not relate to goods cleared under notified exemption notifications and all returns for the last 6 months under the existing law are filed immediately preceding the appointed date.

5.4 Section 140(2) of the CGST Act, 2017 stipulates that a registered person can avail the unavailed CENVAT credit of capital goods not carried forward in the return under the existing law relating to the period before 01.07.2017, if such credit is admissible as ITC under the CGST Act, 2017.

5.5 Section 140(3) of the CGST Act, 2017 states that a registered person can take credit of eligible duties in respect of inputs held in stock & inputs contained in semi-finished or finished goods held in stock on appointed day, if he was not liable to be registered under the existing law, manufactures or provides exempted supply, provides works contract service & was availing benefit of Notification No. 26/2012-ST and is a first or second stage dealer or a registered importer or a depot of a manufacturer, subject to following conditions:

- The inputs or goods are used for making taxable supplies under this Act;

- The registered person is eligible for ITC on such inputs under this Act;

- Invoices evidencing payment of duty under existing law is in possession;

- Such invoices were issued not earlier than 12 months before the appointed day;

- The supplier of services is not eligible for any abatement under this Act.

5.6 Section 140(4) of the CGST Act, 2017 provides that Input tax Credit can be taken under Section 140(1) & (3) for supply taxable under this act & previously assessable under the Central Excise Act, 1944 or Chapter V of the Finance Act, 1994. (Section 140 (1, 3, 4, 5) of CGST Act 2017)

5.7 Section 140(5) of the CGST Act, 2017 states that Input tax Credit of eligible duties (except service tax) can be taken for supplies received on or after the appointed day if the invoice was recorded in the books of accounts within 30 days from the appointed day & statement is furnished.

5.8 Section 140(6) of the CGST Act, 2017 states that a registered person paying tax at a fixed rate or composition levy can take credit of eligible duties in respect of inputs held in stock & inputs contained in semi-finished or finished goods held in stock on appointed day provided, the inputs or goods are used for making taxable supplies under this Act, the registered person is eligible for ITC on such inputs under this Act, invoices evidencing payment of duty under existing law are in possession and such invoices were issued not earlier than 12 months before the appointed day. (Section 140(6) of CGST Act 2017)

5.9 Section 140(7) of the CGST Act, 2017 provides that Input tax Credit on services received prior to the appointed day by an Input Service Distributor shall be eligible for distribution even if the invoices relating to such services are received on or after the appointed day.(Section 140(7) of CGST Act 2017)

5.10 Section 140(8) of the CGST Act, 2017 states that a registered person having centralized registration under existing law can avail CENVAT credit carried forwarded in the return under the existing law relating to the period before the appointed day, provided that such credit is admissible as ITC under this Act and all returns for the last 3 months under the existing law are filed before the appointed date. (Section 140(8) of CGST Act 2017)

5.11 Section 140(9) of the CGST Act, 2017 provides that if CENVAT credit for input services provided under the existing law has been reversed due to non-payment of consideration within 3 months, credit can be reclaimed if payment is made within 3 months from the appointed day. (Section 140(9) of CGST Act 2017)

5.12 Section 141 of the CGST Act, 2017 Transitional provisions relating to job work: (Section 141 of CGST Act 2017)

If any inputs or semi-finished goods or excisable goods are sent to a job worker without payment of tax under existing law prior to the appointed day & such inputs or goods are returned within 6 months from the appointed day, no tax is payable, if manufacturer & job-worker declare the details of the inputs or goods held in stock by the job-worker on the appointed day. If said inputs or goods are not returned within the specified period, ITC shall be recovered under Section 142(8)(a) of the CGST Act, 2017. The manufacturer may transfer the said goods to the premises of any registered person for supplying there from, on payment of tax in India or without payment of tax for exports within specified period. (Section 142(8) (a) of CGST Act, 2017)

5.13 Section 142 – Miscellaneous transitional provisions:

(i) Section 142(1) of the CGST Act, 2017 provides that if goods on which duty had been paid under the existing law at the time of removal (less than 6 months prior to the appointed day) are returned by an unregistered person within 6 months from the appointed day, then the person shall be eligible for refund. (Section 142(8) (a) of CGST Act, 2017)

(ii) Section 142(2) of the CGST Act, 2017 provides that if in pursuance of a contract entered into prior to the appointed day, the price of supply is revised on or after the appointed day, supplementary invoice or debit or credit note shall be issued within 30 days of such revision & such issue shall be deemed to be outward supply made under this Act. If recipient has not reduced ITC relating to credit note, supplier cannot reduce his tax liability relating to credit note. (Section 142(2) of CGST Act 2017)

(iii) Section 142(3) of the CGST Act, 2017 provides for refund filed by any person before, on or after the appointed day, for refund of any amount of CENVAT credit, duty, tax, interest or any other amount paid under the existing law and will be disposed of in accordance with the provisions of existing law and any amount eventually accruing to him shall be paid in cash. (Section 142(3) of CGST Act 2017)

(iv) Section 142(4) of the CGST Act, 2017 provides for refund filed after the appointed day for refund of any duty or tax paid under existing law in respect of the goods or services exported before or after the appointed day and shall be disposed of in accordance with the provisions of the existing law. (Section 142(4) of CGST Act 2017)

(v) Section 142(5) of the CGST Act, 2017 provides for refund of tax paid after the appointed day under the existing law in respect of services not provided and shall be disposed of in accordance with the provisions of existing law and any amount eventually accruing to him shall be paid in cash. (Section 142(5) of CGST Act 2017)

(vi) Section 142(6) of the CGST Act, 2017 provides that every proceeding of appeal, review or reference relating to a claim for CENVAT credit initiated whether before, on or after the appointed day under the existing law shall be disposed of in accordance with the provisions of existing law, and any amount of credit found to be admissible to the claimant shall be refunded to him in cash. (Section 142(6) of CGST Act, 2017)

(vii) Section 142(7) of the CGST Act, 2017 states that every proceeding of appeal, review or reference relating to any output duty or tax liability initiated whether before, on or after the appointed day under the existing law, shall be disposed of in accordance with the provisions of the existing law, and if any amount becomes recoverable as a result of such appeal, review or reference, the same shall, unless recovered under the existing law, be recovered as an arrear of duty or tax under this Act and in case any amount found to be admissible to the claimant shall be refunded to him in cash. (Section 142(6) of CGST Act, 2017)

(viii) Section 142(8) of the CGST Act, 2017 states that where in pursuance of an assessment or adjudication proceedings instituted, whether before, on or after the appointed day, under the existing law, any amount of tax, interest, fi ne or penalty becomes recoverable from the person, the same shall, unless recovered under the existing law, be recovered as an arrear of tax under this Act and if found refundable to the taxable person, the same shall be refunded to him in cash under the said law. (Section 142(8) of CGST Act, 2017)

(ix) Section 142(9) of the CGST Act, 2017 states that where any return, furnished under the existing law, is revised after the appointed day and if, pursuant to such revision, any amount is found to be recoverable or any amount of CENVAT credit is found to be inadmissible, the same shall, unless recovered under the existing law, be recovered as an arrear of tax under this Act and if found to be refundable or CENVAT credit is found to be admissible to any taxable person, the same shall be refunded to him in cash under the existing law. (Section 142(9) of CGST Act 2017)

(x) Section 142(10) of the CGST Act, 2017 stipulates that the goods or services or both supplied on or after the appointed day in pursuance of a contract entered into prior to the appointed day shall be liable to tax under the provisions of this Act. (Section 142(10) of CGST Act 2017)

(xi) Section 142(11) of the CGST Act, 2017 provides that no tax is payable to the extent the tax was leviable under the VAT Act of the State or Chapter V of the Finance Act, 1994 & if tax is already paid then credit can be taken for supplies after the appointed day. (Section 142(11) of CGST Act 2017)

(xii) Section 142(12) of the CGST Act, 2017 provides that if goods are sent on approval not less than 6 months before the appointed day are rejected or returned within 6 months after the appointed day, no tax is payable. (Section 142(12) of CGST Act 2017)

(xiii) As per Section 142(13) of the CGST Act, 2017 if invoice is issued before appointed day but payment is made on or after the appointed day, TDS is not deducted under Section 51 even if required to be deducted under any State or Union territory law relating to VAT. (Section 142(13) of CGST Act 2017)

6. CGST RULES, 2017 UNDER THE TRANSITIONAL PROVISIONS

6.1 Rule 117 of the CGST Rules, 2017 stipulates that every registered person entitled to take credit of input tax under Section 140 of CGST Act, 2017 shall submit a declaration electronically in FORM GST TRAN-1, within ninety days of the appointed day. The amount of credit specified in the application in FORM GST TRAN-1 shall be credited to the Electronic Credit Ledger of the applicant maintained in FORM GST PMT-2 on the common portal. Form GST TRAN-2 is available for dealers and traders who have registered for GST after being previously unregistered. If a dealer does not possess a VAT or excise invoice for the stocks they held on 30.06.2017, they may use TRAN-2 to claim a tax credit on those stocks. (Rule117 of CGST Rule 2017) (Section 140 of CGST Act 2017)

6.2 Rule 118 of the CGST Rules, 2017 states that every person to whom the provision of clause (c) of sub-section (11) of section 142 applies, shall within the period specified in rule 117 shall submit a declaration electronically in FORM GST TRAN-1 furnishing the proportion of supply on which Value Added Tax or Service Tax has been paid before the appointed day but the supply is made after the appointed day, and the Input Tax Credit admissible thereon. (Rule 118 of CGST Rules 2017)

6.3 As per Rule 119 of the CGST Rules, 2017, every person to whom the provisions of Section 141 apply within the period specified in rule 117 shall submit a declaration electronically in FORM GST TRAN-1, specifying therein, the stock of the inputs, semi-finished goods or finished goods, as applicable, held by him on the appointed day. (Rule 119 of CGST Rules 2017 Section 141 of CGST Act, 2017)

6.4 Rule 120 of the CGST Rules, 2017 states that every person having sent goods on approval under the existing law and to whom sub-section (12) of section 142 applies within the period specified in rule 117 shall submit details of such goods sent on approval in FORM GST TRAN-1. (Rule 120 of CGST Rule 2017 Section 142(12) of CGST Act, 2017)

6.5 Rule 120A of the CGST Rules, 2017 states that every registered person who has submitted a declaration electronically in FORM GST TRAN-1 within the time period specified in rule 117, rule 118, rule 119 and rule 120 may revise such declaration once and submit the revised declaration in FORM GST TRAN-1 electronically on the common portal within the time period specified in the said rules. (Rule 117, 118,119, 120,120A of CGST Rules, 2017)

6.6. Rule 121 of the CGST Rules, 2017 provides for recovery of credit wrongly availed under section 73 or 74 of the CGST Act, 2017. (Rule 121 of CGST Rules,2017 Section 73,74 of CGST Act, 2017)

7. CIRCULARS ISSUED BY CBIC

- Circular No. 87/06/2019-GST dated 02.01.2019 -Clarification regarding section 140(1) of the CGST Act, 2017.

- Circular No. 42/16/2018-GST dated 13.04.2018 -Clarification regarding procedure for recovery of arrears under the existing law and reversal of inadmissible input tax credit.

- Circular No.180/12/2022-GST dated 09.09.2022 – Guidelines for filing/revising TRAN-1/TRAN-2 in terms of order dated 22.07.2022 & 02.09.2022 of Hon’ble Supreme Court in the case of Union of India vs. Filco Trade Centre Pvt.

- Circular No. 182/14/2022-GST – Guidelines for verifying the Transitional Credit in light of the order of the Hon’ble Supreme Court in the Union of India vs. Filco Trade Centre Pvt. Ltd., SLP(C) No. 32709- 32710/2018, order dated 07.2022 & 02.09.2022.

*****

Source: Handbook of GST Law and Procedures for Departmental Officers issued by Ministry of Finance