Bonded Manufacturing Scheme

In the current situation of COVID 19 pandemic which have a major impact on all aspects of daily life and undeniably also on businesses. Business leaders now face immediate challenges, including managing their cash flow. Any relief from the government during this pandemic which results in providing a better cash flow management is highly appreciated.

A scheme which was introduced with the support to promote India as the next manufacturing hub and to encourages investments in India through Realtime assistance to entities to set up business is now beneficial in the current pandemic situation too.

About the Scheme

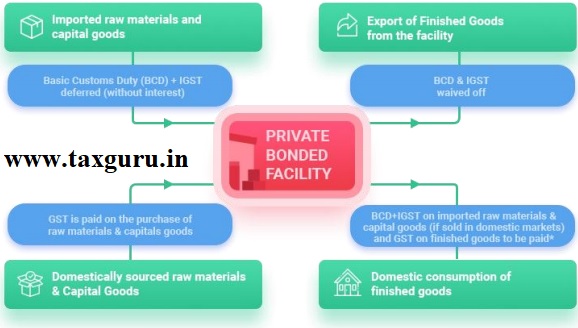

The scheme allows the import of raw materials and capital goods without payment of duty (BCD + IGST) for manufacturing and other operations in a bonded manufacturing facility.

Deferment or waiver of Import duty:

- The import duty is deferred for payment till such time, when the resultant finished goods are cleared to the domestic market,

- In cases where imported goods are utilized for the purpose of exports*, the import duty is exempted or waived off.

(Source: https://static.investindia.gov.in/s3fs-public/inline-images/CBIC%20Page_BM%20DE_V2.png)

*It is pertinent to note that along with the waiver of import duty, the GST on the exported goods can be zero-rated as per the provisions of section 16 of IGST Act read with rules.

As such there is no restriction on type of the businesses who can avail the benefits under this scheme, the scheme is available to all type of business.

Procedure to avail the benefits of the Scheme

Common application cum approval form for a license for private bonded facility and permission for manufacturing and other operation:

⇒ Fill online application as per Annexure A

Some details like Nature of manufacturing, details of imported goods, expected trade volume along with the relevant documents like – COI, Partnership Deed, ID proofs of proprietors/ partners/ directors, Aadhar Card of Authorised Signatory, Documents supporting property-holding rights, such as rent agreement, warehouse license, if issued earlier, Ground plan of the site, Fire safety audit certificate.

⇒ Execute a bond as per Annexure C and submit a physical copy to your Jurisdictional Commissioner of Customs

⇒ Maintain detailed accounts as per Annexure B

⇒ Commissioner of Customs grants the permission for manufacturing or other operations in the bonded facility

⇒ Approval from the Authorities

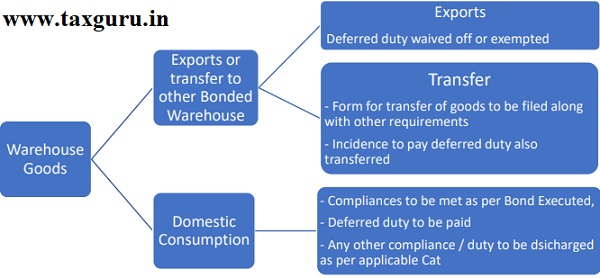

Steps for clearance of Warehouse Goods

Positives of the Scheme

- Provides cash flow support up to certain extent

- Single Point approval

- Unlimited period of warehousing

- No geographical restriction

- Easy compliances (As per Annexure B)

- No blockage of funds for the exporters otherwise they have to claim refund under GST under appliable rules

Negatives of the Scheme

The only negative point one can see is, it may discourage the domestic suppliers, as no exemption is provided to the suppliers of such units. If all other conditions are same, the manufacturers may opt for the imports instead of domestic supplies of Inputs & Capital goods. This may go against the concept of Aatma Nirbhar Bharat, the vision of Central Government.

Disclaimer – The above writeup is for educational & information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. There may be possibility of different view on the various subject matter discussed – nikunjsharma4@gmail.com