Assessment under GST

Self-Assessment (Own Assessment) – Section 57

Every person registered under the Act shall himself assess the tax payable by him for a tax period and after such assessment he shall file the return required under section 34.

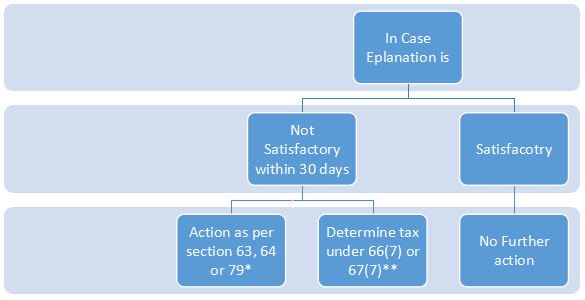

Scrutiny of Returns – Section 59

The Proper officer may scrutinize the returns and inform the tax payer for any discrepancy noticed and seek his explanation.

* Section 63: Audit by Tax Authority

Section 64: Special Audit

Section 79: Power of Inspection, Search & Seizure

** Section 66(7) : Determine tax, interest & Penalty (Penalty is higher of 10 % of tax or Rs. 10000)

Section 67(7): Determine tax, Interest & Penalty based on representation

Assessment of Non Fillers of Returns – Section 60

Sub section 1 explains where a registered taxable person fails to furnish the return required under:

Section 34 – Returns – Monthly or Quarterly or annually as the case may be, or;

Section 40 – Final Return, or;

Section 41 – Within 15 days of receipt of Notice.

The proper officer will pass Assessment order as per “Best Judgement” principal. The officer can pass such order time limit specified u/s 67(8) i.e. 5 years from the due date of return.

Subsection 2 Says that if the person furnishes a valid return within 30 days of the Best judgement assessment order passed, the Said order will stand withdrawn.

Nothing in this section shall preclude the liability for payment of interest under section 45 and/or for payment of late fee under section 42.

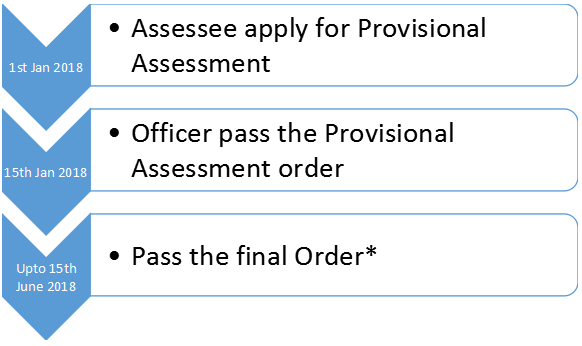

Provisional Assessment – Section 58

Where the taxable person is unable to determine

- The value of goods and/or Service,

- The rate of tax applicable thereto,

He may request the proper officer in writing giving reasons for payment of tax on a provisional basis and the proper officer may pass an order allowing payment of tax on provisional basis at such rate or on such value as may be specified by him.

No tax officer can suomoto order payment of tax on provisional basis.

In such cases the taxable person has to execute a bond in the prescribed form, and with such surety or security as the proper officer may deem fit.

The proper officer shall, within a period not exceeding six months from the date of the communication of the Provisional order issued, pass the final assessment order. (Dates shown below are exemplary)

*Note:

The Joint/Additional Commissioner may extend the period of passing final assessment order by additional SIX months.

The Commissioner may extend the period of passing the final assessment order by period as he may deem fit (i.e. as per Commissioner’s wish)

IF, Tax paid as per Provisional Order < Final Order, the balance amount is to be paid with Interest from the actual due date.

Assessment of unregistered persons – Section 61

Where a taxable person fails to obtain registration even though liable to do so, the proper officer may proceed to assess the tax liability of such taxable person as per

“BEST JUDGEMENT ASSESSMENT”

for the relevant tax periods and issue an assessment order within a period of five years from the due date for filing of the annual return for the year to which the tax not paid relates.

The Person must be given a Show cause Notice and a reasonable opportunity of being heard before passing the order.

Summary Assessment – Section 62

- If assessing officer comes across sufficient grounds to believe any delay in showing a tax liability may cause harm to interest of the revenue, so to protect the interest of the revenue, with the prior permission of additional/joint commissioner, pass the assessment order.

It also provides that where the taxable person to whom the liability pertains is not ascertainable and such liability pertains to supply of goods, the person in charge of such goods shall be deemed to be the taxable person liable to be assessed and pay tax and amount due under this section.

- On an application made within thirty days from the date of receipt of order passed under sub-section (1) by the taxable person or on his own motion, if the Additional/Joint commissioner considers that such order is erroneous, he may withdraw such order and follow the procedure laid down in section 66 or 67.

You can provide your feedback @ camayur2@gmail.com.

Author Bio