CA Ashish Agrawal

Introduction

The provisions related to “Appeals and Revision” are contained in chapter XVIII-from section 107 to section 121. It gives a detailed explanation on authorities on appeal and revision, appealable and non-appealable orders and decisions and procedures in appeal to be followed by appellant and authorities.

To start with, the following are the list of authorities provided in appeals and revision:-

1. Appellate authority– Yet to be prescribed the eligible person but looking at the administrative set-up and detailed reading of the related provisions, it seems authorities above the rank of commissioner can be nominated for the position.

2. Revisionary Authority– The reading of the related section suggests, a rank of commissioner or above can be considered as revisionary authority.

3. Appellate Tribunal (Section 112)

4. High Court (Section 117)

5. Supreme Court (Section 118)

First level authority- Comparison with existing laws

If we compare this to the authorities in the existing laws, the first level of authority to whom appeal can be filed is Commissioner(Appeals) for central laws and commissioner for state laws, and in case commissioner is the adjudicating authority, the first appeal lies with tribunal. In the new law, Introduction of appellate authority as the first level for all the cases is an attempt to reduce the burden at tribunal level and marking a clear distinction between the adjudicating and appellate authorities.

Similarly, the revisionary powers, in the present laws, lie with Central government in the central laws and commissioner in the state law.However, for central laws the central government has not designated any particular authority to discharge the functions and therefore the provisions were merely existing and seldom invoked.

Appealable and Non Appealable Orders

Before we dwell into the detailed analysis of appeals and related matters at various levels, it is pertinent to understand the scope of orders and decisions which are appealable or non-appealable.

Section 121 contains, notwithstanding anything to the contrary in any provisions of this Act, no appeal lies against the following orders: –

a) An order of the Commissioner or other authority empowered to direct transfer of proceedings from one officer to another officer; or

b) An order pertaining to the seizure or retention of books of accounts, register and other documents; or

c) An order sanctioning prosecution under this act; or

d) An order passed under section 80

The provisions are self-explanatory but for the first item which looks ambiguous. A careful reading suggests that any order of the commissioner or other authority empowered to direct transfer of proceedings shall be non- appealable. Un-arguably it is a drafting error and the intent is to prohibit appeal against the orders which has the effect of transfer of proceedings only.

In the present law, a separate section exists in VAT laws for non- appealable orders (Section 79 in case of D- VAT) and for central laws the corresponding provisions are contained in the respective sections of appeal to various authorities.

The list is longer and more restrictive in the present law as compared to the proposed law. For instance, in matters of questions of rate of duty of excise and value of goods for purposes of assessment, no appeal shall lie with high court (Section 35G).

Detailed explanations on Sections

1. Appeals to Appellate Authority- Section 107

The first section in the league briefs about appeals to the appellate authority. A flow chart is presented below for better understanding:-

A similar procedure is prescribed for revenue to appeal against the order of adjudicating authority but with the following variations:-

a) Authority of the rank of commissioner can suo moto or on request of commissioner of State or UT GST can direct any sub-ordinate, through an order, to file the appeal within six monthsof date of communication of the original order. The authorized officer shall become appellant and the appeal shall be construed as appeal against the order of adjudicating authority.

b) The commissioner has to be satisfied on grounds of “legality and propriety” to determine the case fit for appeal [Section 107(2)]

An important observation to note here is the commissioner is not obliged to file against the order only in cases where it is against the interest of revenue. Therefore, even in cases where the orders are against the interest of revenue but the commissioner is satisfied otherwise on the grounds mentioned above, the case can be said as “fit for appeal”. An interesting argument though arises as to who shall be appellant in those cases ( Commissioner through his authorized officer or the person against whom the order is passed).

There are few anomalies in the drafting of section which is highlighted below:-

1. In proviso to section [107(13)] , it says to exclude the time of stay for issuance of order as directed by the court or tribunal from the recommendatory period of 1 year to pass the order.

If the period is only recommendatory, then whether the proviso is redundant to that extent.

If it is mere clarification, then whether appeal for stay of issuance of order lies with Tribunal also.

Contrast with Present Laws

The similar provisions of appeal exist in the present laws as discussed above, except the first level of appeal lies with commissioner ( Appeals) in case of central laws and Commissioner in case of state laws.

The provisions of appeal by the commissioner against the order of adjudicating authority is similar except two contrast as:-

a) when the adjudicating authority is commissioner, the appeal shall be filed with tribunal.

b) The powers are vested with committee to decide the case fit for appeal and not individual commissioner which reduces the scope of biasness and judgemental errors.

2. Powers of Revisionary Authority- Section 108

The section goes on to give the power to revisionary authority to revise orders passed by the adjudicating authority sub-ordinate to him in the following circumstances:-

a) On his own motion; or

b) Information received by him; or

c) Request from commissioner of State or UT GST

It further restricts the scope only to orders which were “ erroneous in so far as it is prejudicial to the interest of the revenue and is illegal or improper or has not taken into account certain material facts, whether available at the time of issuance of the said order or not or in consequence of an observation by the CAG” [Section 108(1)].

Few critical points to ponder from the above said description of the section:-

a) The drafting seems ambiguous to the extent usage of words “information received by him” or “material facts”, as unless these terms are not defined in terms of their source and scope, it may give a scope of un-ending discretion to be used by the authority.

b) The law is not clear whether it intends to give the person other than revenue an opportunity to file for revision unlike in present excise, service tax and income tax laws where it is explicitly allowed for an assessee to file for revision.

c) On careful reading of definitions of “adjudicating authority”, it clearly excludes the revisionary authority from it’s scope of coverage. However, if the language of section 108(1) is anything to go by, then it seems revisionary authority will be a rank of commissioner, thereby leaving few questions un-answered.

Thereafter the section imposes certain restrictions for authority to exercise it’s power on matters [Section 108(2)]:-

a) If the order is subject to appeal under appellate authority, or tribunal, or high court, or supreme court; or

b) The period of six months( allowed to commissioner to file appeal) in section 107(2) has not yet expired or more than 3 years have expired since the passing of order sought to be reversed; or

c) The order has been taken for revision under this act at an earlier stage; or

d) The order is passed in exercise of powers under sub-section (1)( redundant as otherwise also it has authority to revise orders of sub-ordinates only)

This subsection starts with “ The revisionary authority shall not exercise any power……”. The question arises as to the time limit mentioned under clause (b) is for initiating the proceedings or passing of order by the revisionary authority.

Another drafting anomaly emerges if we read section 108(2) and section 108 (4) together.Section 108 (4) seeks to exclude the period spent between the appeal made at high court against the decision of tribunal or period spent between the appeal made at supreme court against the order of high court In proceedings which involve similar issue, from the period mentioned under clause (b) of section 108(2). Section 108(2) as defined above contains restrictions on exercise of power only for orders appealed at higher authority and no-where restricts issuance of order in case the order involving the similar issue is pending at the tribunal or court level. Therefore, the authority is not obliged to execute the proceedings in case any other order involving similar issue is pending at higher levels.

This section other than above points contain procedures to dispose of orders which again are falling short on completeness factor as certain important aspects of whom to communicate etc missing.

In nutshell, this section requires a careful analysis of the issues that might come up in case it is brought in it’s existing structure. Also a look at the corresponding provisions in income tax contained in section 263 and section 264 may be necessary to ensure it benefits appropriately to the revenue and any other aggrieved person.

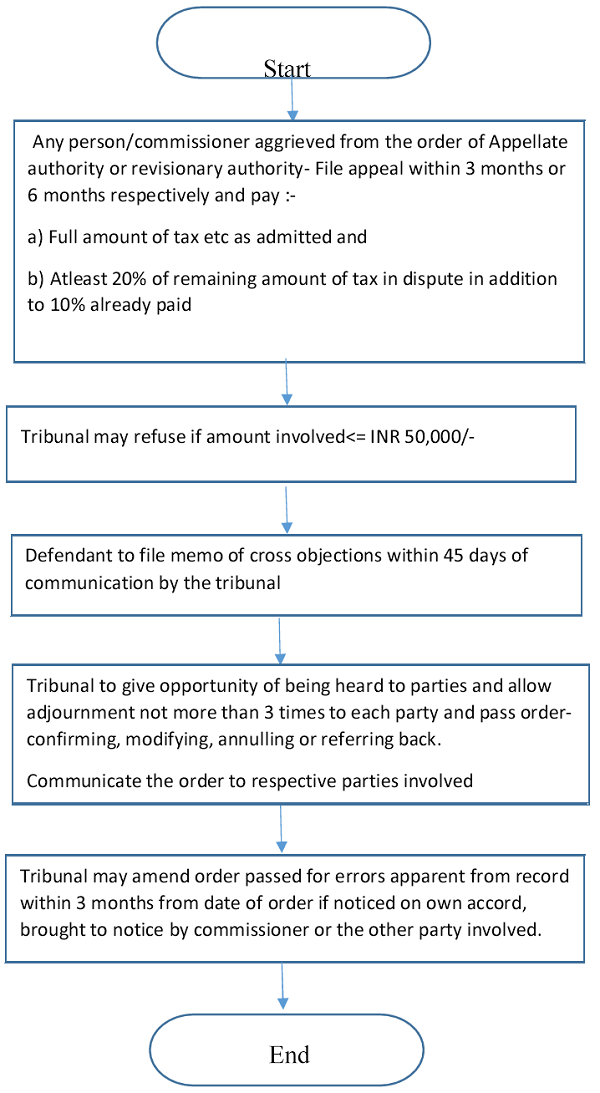

3. Appeals to Tribunal- Section 112 and Section 113

The provisions are explained through flow chart

A recommendatory period of 1 year is prescribed for issuance of order which is at three years in the existing laws.

The remaining provisions of appeal at tribunal is similar to what is provided in existing laws except for some orders which are non-appealable.

4. Appeal to High Court and Supreme Court- Section 117 and Section 118

The provisions contained in sections for appeals to high court and supreme court are lucidly defined and are straight forward and self-explanatory.

The basic premise on which appeal is accepted at the level of high court and above is the involvement of substantial question of law, for which court determines if it involves a question of law or not.

The word substantial is not defined anywhere in the existing laws or proposed law but is now settled by various judicial pronouncements :-

It was observed by the Supreme Court in Sir Chunilal V. Mehta & Sons Ltd. v. Century Spg. & Mfg. Co. Ltd., that “a question of law would be a substantial question of law if it directly or indirectly affects the rights of parties and/or there is some doubt or difference of opinion on the issue”. But “if the question is settled by the Apex Court or the general principles to be applied in determining the question are well-settled, mere application of it to a particular set of facts would not constitute a substantial question of law” – Krishna Kumar Aggarwal v. Assessing Officer.

The major shift in the appeal process at high court and above level is that, some matters decided at the tribunal level (National Bench or regional bench of tribunal) can now be appealed in supreme court only. However, at what level formation and acceptance of substantial question of law would happen is not prescribed.

Conclusion

The attempt is in the right direction, as decisions such as limiting non-appealable orders, creating clear distinction between adjudicating and appellate authority and allowing certain tribunal decisions to be directly appealed at supreme court level indicates an intent to bring in more effectiveness in judiciary process and ensure speedy disposition of appeals.

However, there is a dearth of improvement such as clarifying the provisions related to revisionary authority and bringing in certain innovation in the form of DRP’s etc like as they exist in income tax laws. Looking at the magnitude of issues which will arise post the new law, the appeals and revision architecture needs to be more strengthened.