Akansha Tulsyan

Analysis of Recent Notifications & Circulars issued on 3rd April 2020. (Effective from 20th March 2020)

Notification No. 30/2020- No 110% Restriction for Returns of February 2020 to August 2020

A Provision has been inserted under Rule 36(4) to provide that the said condition shall apply cumulatively for Period February 2020 to August 2020 and the return in Form GSTR-3B for the tax period September 2020 shall be furnished with the cumulative adjustment of input tax credit for the said month i.e. condition of restricting ITC to 110% of GSTR 2A figure for the month of Feb , March, April, May, June, July, August 2020 shall be applied CUMULATIVELY in the GSTR 3B of September 2020.

Example:

| Month | ITC as per GSTR 2A | ITC as per Books | ITC taken in GSTR 3B |

| February-2020 | 35 | 50 | 50 |

| March-2020 | 30 | 40 | 40 |

| April-2020 | 40 | 60 | 60 |

| May-2020 | 50 | 70 | 70 |

| June-2020 | 40 | 50 | 50 |

| July-2020 | 25 | 60 | 60 |

| August-2020 | 55 | 70 | 70 |

| September-2020 | 100 | 150 | 150-[550-(110% of 375)]= 12.5 |

| Total | 375 | 550 | 412.5 |

Notification No: 31/2020 and 32/2020: Rate of Interest and Late fees for delayed filing of GSTR-3B

Notification No 33/2020: No Late fees for delayed filing of GSTR 1

No Late Fees for Returns (GSTR-1) for March, April and May 2020 if Filed on or before 30th June 2020.

Notification No: 30/2020 and 34/ 2020– For Composition Dealers

> Allow taxpayers opting for the Composition scheme for the FY 2020-2021 to file their option in FORM CMP-02 till 30th June 2020

> Extension of due date of furnishing statement, containing the details of payment of Self-assessed tax in FORM GST CMP-08 of the CGST Rules, 2017 for the quarter ending 31st March 2020 till the 7th July 2020.

> Extension of due date of filing FORM GSTR-4 for the FY ending 31st March, 2020 till the 15th day of July 2020.

Notification No 35/2020– Relaxation in other compliances

Any Compliance whose due date falls between 20thday of March, 2020 to the 29th day of June, 2020 shall extended till 30th June 2020. It includes:

> Filing of Appeal

> Reply to ANY Notice

> Making application

> Furnishing of any report/documents

> Filing of Return

> Completion of any proceedings or passing of any orders by any authority, commissioner or tribunal

> Issuance of any notice, intimations, notifications, sanction, approval by any authority, commissioner or tribunal

But such extension of time shall not be applicable for the compliances of the provision of the said Act, as mentioned below:

> Chapter IV;

> Sub-section (3) of section 10, section 25, 27, 31, 37, 47, 50, 69, 90, 122, 129: Application for normal Registration/Casual/Non-Resident to be done even during lockdown; Tax invoice can be raised; Detention of goods may be happen in transit; Arrest can be made under GST during lockdown.

> Section 39 except sub-section (3), (4) and (5): TDS, TCS and ISD Returns filers have been allowed to furnish the respective returns/Statements specified in sub section (3), (4) and (5) & Sec 52 of the said Act, for the month of March 2020 to May 2020 on or before the 30th day of June 2020.

> Section 68, in so far as E-way bill is concerned- E-way Bill need to be generated even during lockdown.

> Rules made under the provision specified above

Note: Deemed Extension of E-way Bill

Where an E-way Bill has been generated under Rule 138 of the CGST Rules, 2017 and its period of validity expires during the period 20th day of March 2020 to 15th day of April 2020, the Validity of such E-way Bill shall be deemed to have been extended till the 30th day of April 2020.

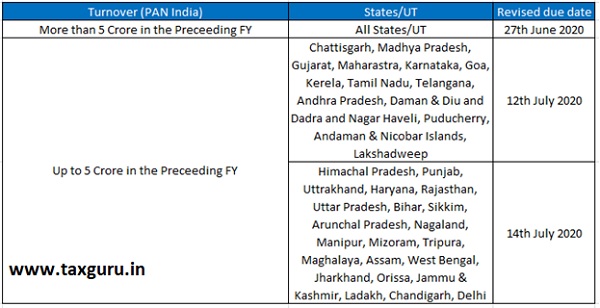

Notification No. 36/2020– GSTR 3B due date for the month of May 2020

Note: The above Notification shall be effective from 20th day of March, 2020.

Author Bio