Page Contents

- A. Frequently asked questions on Form GSTR-5A

- 1. What is GSTR-5A?

- 2. By when do I need to file GSTR-5A?

- 3. Who needs to file GSTR-5A? Is it mandatory to file GSTR-5A?

- 4. What are the available modes of preparing GSTR-5A?

- 5. What are the pre-requisites for filing GSTR-5A?

- 6. From where can I file GSTR-5A?

- 7. What details are required to be furnished in GSTR-5A?

- 8. Can I file GSTR-5A for current period if return for previous period has not been filed?

- 9. Can I file GSTR-5A after making part payment of taxes?

- 10. Can OIDAR services provider claim ITC in GSTR-5A?

- 11. Is there any late fee in case of delayed filing of GSTR-5A?

- 12. What happens after Form GSTR-5A is filed?

- 13. Is there an Electronic Credit Ledger available for GSTR-5A?

- 14. I have already made payment on the CBEC Portal for GSTR-5A liabilities. Do I need to again make payment on the GST Portal?

- B. Procedure / Manual four filing of Form GSTR-5A

A. Frequently asked questions on Form GSTR-5A

1. What is GSTR-5A?

GSTR-5A is a Return to be furnished by Online Information and Database Access or Retrieval (OIDAR) services provider to un-registered person or customers, on the GST Portal for the services provided from a place outside India to a person in India, other than a registered person.

2. By when do I need to file GSTR-5A?

Monthly Return(s) needs be filed by 20th of the month succeeding the Tax period to which the return pertains or by the date as may be extended by Commissioner.

3. Who needs to file GSTR-5A? Is it mandatory to file GSTR-5A?

Non-Resident Online Information and Database Access or Retrieval (OIDAR) services provider needs to file return in Form GSTR-5A. Filing of return is mandatory.

GSTR-5A needs to be filed even if there is no business activity (Nil Return) in the tax period.

4. What are the available modes of preparing GSTR-5A?

GSTR-5A can be prepared using the following modes through:

- Online entry of data on the GST Portal after log in

- Using third party application of Application Software Provider (ASPs) through GST Suvidha Providers (GSPs)

5. What are the pre-requisites for filing GSTR-5A?

Pre-requisites for filing GSTR-5A are:

1. Taxpayer should be a registered as OIDAR services provider and should have a valid GSTIN.

2. Taxpayer should have valid User ID and Password.

3. Taxpayer should have valid & non-expired/ non-revoked PAN based Digital Signature (DSC) for filing with DSC.

4. Taxpayers can file the return through EVC also. If authorised signatory is not an Indian, OTP will be conveyed through e-mail message.

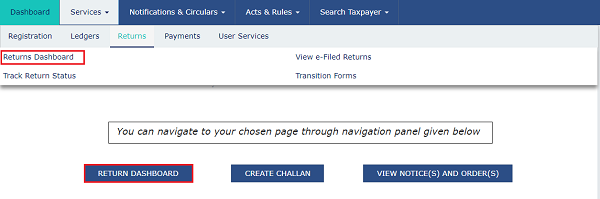

6. From where can I file GSTR-5A?

Login to the GST Portal and click the Services > Returns > Returns Dashboard command to file GSTR-5A.

7. What details are required to be furnished in GSTR-5A?

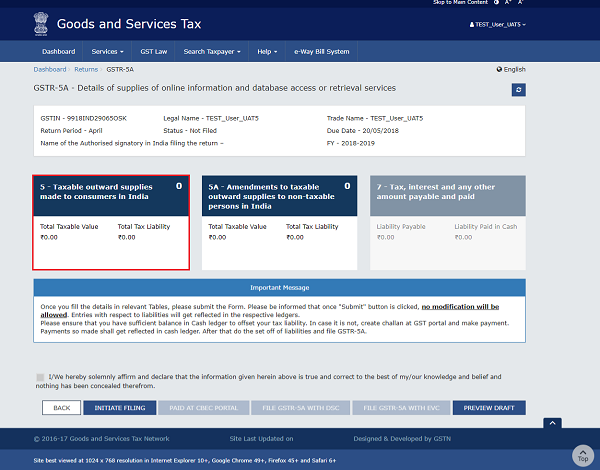

The taxpayer can furnish details of taxable outward supplies made to non-taxable persons/ consumers in India, amendment to the details furnished in preceding tax period(s) and to view details of interest, or any other amount and offset the liabilities etc. in their GSTR-5A.

8. Can I file GSTR-5A for current period if return for previous period has not been filed?

No, GSTR-5A return cannot be filed for the current tax period, if return for the previous tax period has not been filed.

9. Can I file GSTR-5A after making part payment of taxes?

No, GSTR-5A return cannot be filed after making part payment of taxes. It can be filed only after making full payment of taxes and other liabilities for the return period.

10. Can OIDAR services provider claim ITC in GSTR-5A?

No, OIDAR services provider cannot claim any ITC in GSTR-5A.

11. Is there any late fee in case of delayed filing of GSTR-5A?

At present, there is no late fee in case of delayed filing of GSTR-5A.

12. What happens after Form GSTR-5A is filed?

After successful filing of the Form GSTR-5A, an acknowledgement is generated and an Email message is sent to the taxpayer on the Indian mobile number of authorized signatory mentioned in the registration application. If mobile number is obtained from authorised Indian person, then SMS will also be sent to the authorized signatory.

13. Is there an Electronic Credit Ledger available for GSTR-5A?

No, there is no Electronic Credit Ledger maintained for GSTR-5A.

14. I have already made payment on the CBEC Portal for GSTR-5A liabilities. Do I need to again make payment on the GST Portal?

No, you do not need to make any payment on the GST Portal if you have already made payment on the CBEC Portal for GSTR-5A liabilities. You just need to mention Payment Reference number and Date of the payment as generated in the CBEC Portal on the GST Portal before filing GSTR-5A.

Payment Reference number should be either numeric or alpha numeric and should be upto 25 digits.

B. Procedure / Manual four filing of Form GSTR-5A

1. How can I create and file details for the Taxable outward supplies made to consumers in India in the Form GSTR-5A?

To create, submit and file details for the outward supplies in the GSTR-5A, perform the following steps:

1. Login and Navigate to GSTR-5A page

2. Enter Details in various tiles

3. Preview Draft

4. Initiate Filing for GSTR-5A

5. Offset Liabilities

6. File GSTR-5A with DSC/ EVC

7. Download Filed GSTR-5A Return

1. Access the www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the GST Portal with valid credentials.

3. Click the Services > Returns > Returns Dashboard command.

Alternatively, you can also click the Returns Dashboard link on the Dashboard.

4. The File Returns page is displayed. Select the Financial Year & Return Filing Period (Month) for which you want to file the return from the drop-down list.

4. The File Returns page is displayed. Select the Financial Year & Return Filing Period (Month) for which you want to file the return from the drop-down list.

5. Click the SEARCH button.

6. The File Returns page is displayed. This page displays the due date of filing the returns, which the taxpayer is required to file using separate tiles.

In the GSTR-5A tile, click the PREPARE ONLINE button.

Note: The due date for filing GSTR-5A is 20th of every month or as extended by the Commissioner.

Note: The due date for filing GSTR-5A is 20th of every month or as extended by the Commissioner.

2. Enter Details in various tiles

There are tiles representing tables to enter relevant details. Click on the tile names to know and enter related details:

- 5 – Taxable outward supplies made to consumers in India – To add details of Taxable outward supplies made to consumers in India

- 5A – Amendments to taxable outward supplies to non-taxable persons in India – To add details of amendment to taxable outward supplies to non-taxable persons in India

5 – Taxable outward supplies made to consumers in India

To add details of Taxable outward supplies made to consumers in India, perform the following steps:

1. Click the 5 – Taxable outward supplies made to consumers in India tile.

2. The 5 – Taxable outward supplies made to consumers in India page is displayed. Click the ADD DETAILS button to add details for a new POS.

3. Select the Place of Supply from the drop-down list.

4. In the Taxable Value field, enter the Taxable Value.

5. Select the Rate from the drop-down list.

6. Click the ADD button.

7. Click the SAVE button.

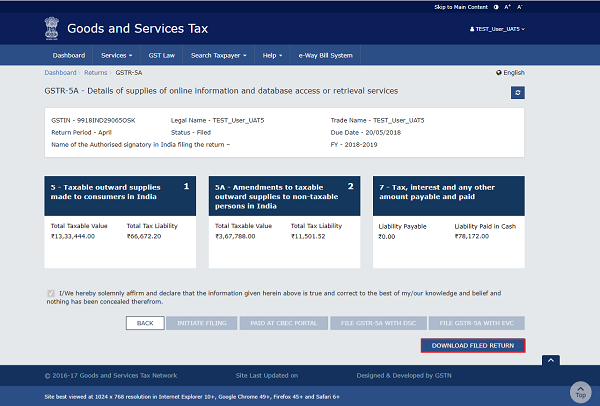

You will be directed to the GSTR-5A landing page and the 5 – Taxable outward supplies made to consumers in India tile in GSTR-5A will reflect Total Taxable Value and Total Tax Liability.

Similarly, you can add details of State wise supplies made to consumers during the tax period.

5A – Amendments to taxable outward supplies to non-taxable persons in India

1. Click the 5A – Amendments to taxable outward supplies to non-taxable persons in India tile to add details of amendment to taxable outward supplies to non-taxable persons in India.

To Add details:

To Add details:

a. Select the Financial Year from the drop-down list.

b. Select the Months from the drop-down list.

c. Select the Place of Supply (State/UT) from the drop-down list.

d. Click the SEARCH button.

e. In the Taxable Value field, enter the taxable value amount.

e. In the Taxable Value field, enter the taxable value amount.

f. Select the Rate from the drop-down list.

g. In the Cess field, enter the amount of Cess.

h. Click the ADD button.

i. The amended records are displayed. You can also click the Delete button to delete the record.

i. The amended records are displayed. You can also click the Delete button to delete the record.

j. Click the SAVE button.

To Amend details:

To Amend details:

a. Select the Financial Year from the drop-down list.

b. Select the Months from the drop-down list.

c. Select the Place of Supply (State/UT) from the drop-down list.

d. Click the SEARCH button.

e. The search results are displayed. You can also click the Edit button to edit the details.

e. The search results are displayed. You can also click the Edit button to edit the details.

f. Once details are edited, click the SAVE button.

2. Click the BACK Button. You will be directed to the GSTR-5A landing page and the 5A – Amendments to taxable outward supplies to non-taxable persons in India tile in GSTR-5A will reflect Total Taxable Value and Total Tax Liability.

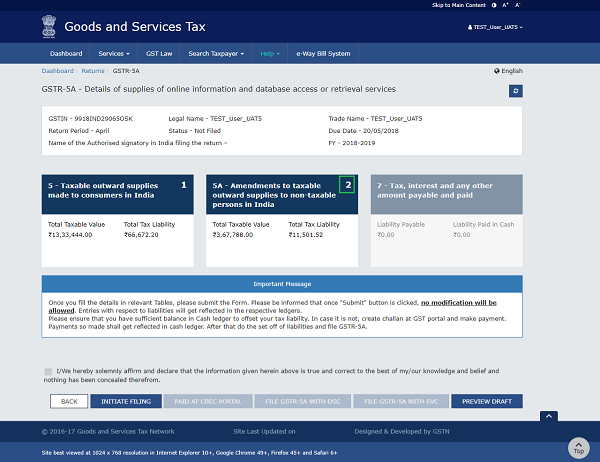

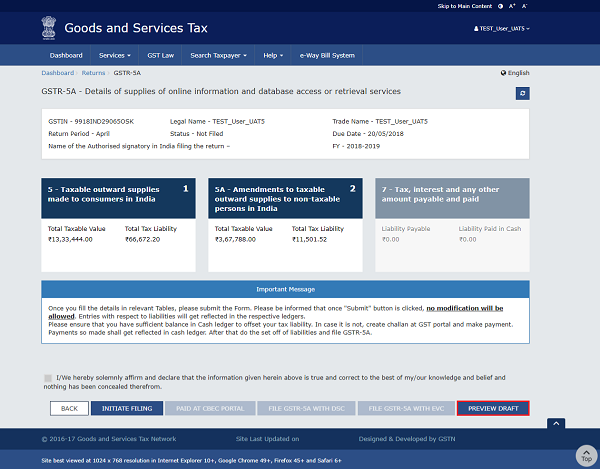

3. Preview Draft for GSTR-5A

1. Click the PREVIEW DRAFT button to preview the draft for GSTR-5A.

Draft is displayed in PDF format.

4. Initiate Filing for GSTR-5A

1. Click the INITIATE FILING button in the landing page to initiate filing for GSTR-5A.

Note:

- The INITIATE FILING button will freeze the information filled up for that particular month.

- Please ensure that you have sufficient balance in Electronic Cash Ledger to offset your tax liability. In case it is not, create challan at GST portal and make payment which will be reflected in Electronic Cash Ledger. Thereafter, proceed on to set off liabilities and file GSTR-5A.

2. Summary of information is displayed. Click the CONFIRM AND SUBMIT button.

Please note that clicking on the CONFIRM AND SUBMIT button will freeze the information filled up for that particular month.

Refresh the page and the status of GSTR-5A changes to Submitted after the submission of GSTR-5A.

Once you submit GSTR-5A, 6 – Calculation of interest or any other amount, 7 – Tax, interest and any other amount payable and paid tile and PAID AT CBEC PORTAL button gets enabled.

5. Offset Liabilities

Scenario 1: In case you have not paid the liability of GSTR-5A through CBEC Portal

1. To view details of interest or any other amount payable, click the 7 – Tax, interest and any other amount payable and paid tile.

2. Click the CHECK LEDGER BALANCE button to know the balance in the Electronic Cash Ledger.

3. Click the OK button.

4. Click the OFFSET LIABILITY button after filling in the amount to be paid in various heads.

5. Click the CLOSE button.

6. Liability is offset and debit number is displayed. Click the BACK button.

7. You can click the PREVIEW DRAFT button to preview the draft for GSTR-5A.

The form is displayed in the PDF format.

Scenario 2: In case you have paid the liability of GSTR-5A through CBEC Portal

In case you have already paid the liability of GSTR-5A through CBEC Portal, you do not need to go for net banking for paying the liability through cash.

1. Click the PAID AT CBEC PORTAL button.

2. Click the Yes radio button.

3. Enter the Reference number and Date of the payment as generated in the CBEC Portal.

Note:

- Payment Reference number should be either numeric or alpha numeric and should be upto 25 digits.

- Once the details are submitted, credit entry is posted to the Electronic Liability Register and taxpayer can file the return. After filing return, tax authorities of CBEC may verify the payment made.

4. Click the CLOSE button.

5. You can click the PREVIEW DRAFT button to preview the draft for GSTR-5A.

The form is displayed in the PDF format.

6. File GSTR-5A with DSC/ EVC

1. Select the Declaration checkbox.

2. In the Authorised Signatory drop-down list, select the authorized signatory. This will enable the two buttons – FILE GSTR-5A WITH DSC or FILE GSTR-5A WITH EVC.

4. Click the FILE GSTR-5A WITH DSC or FILE GSTR-5A WITH EVC button to file GSTR-5A.

Authentication with DSC can be done if the authorised signatory has a DSC which is issued on an Indian PAN.

Note: On filing of the GSTR-5A, an acknowledgement through e-mail message and SMS is sent to the Authorized Signatory’s mobile.

FILE WITH DSC:

a. Click the PROCEED button.

b. Select the certificate and click the SIGN button.

FILE WITH EVC:

a. Click the PROCEED button.

b. Enter the OTP sent on email and mobile number of the Authorized Signatory registered at the GST Portal and click the VERIFY button.

4. The success message is displayed. Click the CLOSE button.

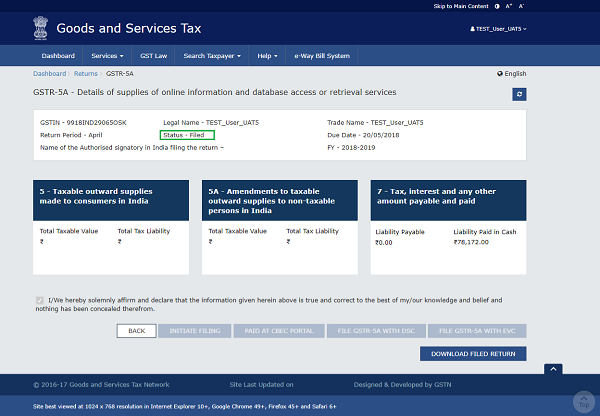

The status of GSTR-5A changes to Filed.

Note: On filing of the GSTR-5A, an acknowledgement through e-mail and SMS is sent to the Authorized Signatory.

7. Download Filed GSTR-5A Return

1. Click the DOWNLOAD FILED RETURN button.

The return is downloaded in PDF format.