♣ As per Section 24(i) of The Central Goods and Service Tax Act, 2017 (herein after referred to as “CGST Act”), Person making any “Inter-State Taxable Supply” needs to get registration notwithstanding anything contained in sub-section (1) of Section 22 of the CGST Act.

As per Notification No.10/2017 – Integrated Tax dated 13th October, 2017, person having inter-state taxable supply upto 20 Lakhs (10 lakhs for certain states) in a financial year are exempted from GST Registration.

♣ Inter- State Taxable supply has not been defined under any of the CGST, IGST, SGST or UGST Act. However, we should look to the definition of “Inter-state supply” and “Taxable supply” given in the Act to determine the meaning of “Inter-State Taxable Supply”

♣ “Inter-State supply” in relation to “Service” has been defined under Section 7(5) of The Integrated Goods and Service Tax Act, 2017 (herein after referred to as “IGST Act”) as

“Supply of goods or service or both –

(a) when the supplier is located in India and the place of supply is outside India;….. ”

Shall be treated to be a supply of goods or service or both in the course of inter-state trade or commerce.”

♣ “Taxable Supply” has been defined under Section 2(108) of the CGST Act as

“Taxable supply means a supply of goods or service or both which is leviable to tax under this Act”

♣ “Exempt Supply” has been defined under Section 2(47) of the CGST Act as “Exempt supply means supply of any goods or service or both which attracts Nil rate of tax or which many be wholly exempt from tax under Section 11 or under Section of the IGST Act and includes non-taxable supply”

♣ Export of service or goods has been classified as “Zero-rated supply” as defined under Section 16 of the IGST Act which is not an exempt category or neither government has stated in the exemption notification that export of service is an exempt service.

♣ If Export of service / goods is an exempt supply then government would not have 2 category like export with IGST and export without IGST which clearly states that export is a taxable supply but if someone satisfy the conditions then he/she can export without IGST. However that does not give exemption to the person from taking the registration which is stated in Section 24 of the CGST Act.

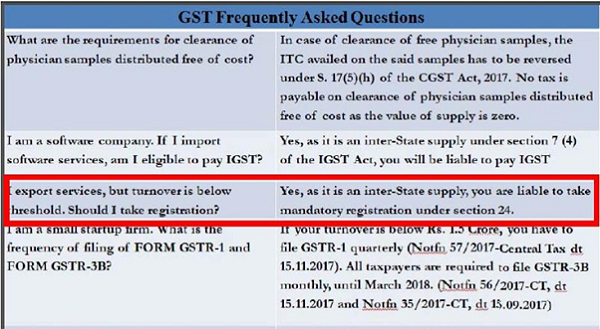

♣ In one of the FAQ answered by the Government and posted on twitter also vide dated 22nd December, 2017, they have clearly stated that export service is an inter-state taxable supply and liable for registration.

Author Bio

EXPORT OF SERVICES NEED TO REGISTER UNDER GST . AFTER REGISTRATION THEN WE WIIL REGISTER UNDER LUT.. and Thus can a dealer export services without registration where his total turnover is below threshold limit

As my turnover is of Rs. 45 lac and local turnover of Rs 2.5 lac should I required to take GST Registration..?

EXPORT OF SERVICES NEED TO REGISTER UNDER GST . AFTER REGISTRATION THEN WE WIIL REGISTER UNDER LUT..

foreign money recived which type of registration required.plz sir help me ..and process

Thanks for sharing.

Exports are treated as inter state supply as per IGST act.

And as per notification no.10/2017 of IGST Tax registration is not mandatory for inter state supplies of services upto threshold limit.

Thus can a dealer export services without registration where his total turnover is below threshold limit.

If yes, does export services would require any other legal formality to be complied with..??

If the services are performed in India on the goods provided by the overseas client and the bill is raised in Foreign Currency whether it will be treated as EXPORT OF SERVICES ? If not then whether it will attract IGST to be charged to the overseas client ? if the foreign client does not pay the IGST as there is no agreement / term in the contract to pay the IGST then whether the IGST is payble under Reverse Charge by the service provider ? if so whether on realisation of basic amount in foreign currency whether the Refund can be filed by the Service provider (Indian Entity) ?

Please guide.