Property Tax can be tapped to generate Additional Revenue at City Level

The Economic Survey 2016-17, presented today in the Parliament by the Union Finance Minister Shri Arun Jaitley, stated that Urban Local Bodies (ULBs), having primary responsibility for the development and service provisioning of cities, face major and inextricably linked problems: large infrastructure deficits, inadequate finances, and poor governance capacities. Every Indian city faces serious challenges related to water and power supply, waste management, public transport, education, healthcare, safety, and pollution.

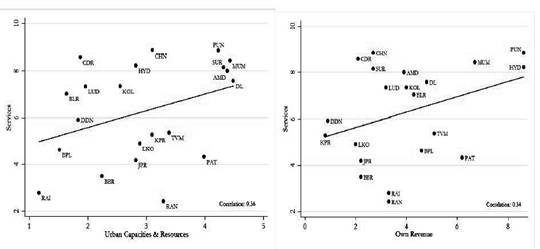

The analysis carried out for the Survey has found that greater service delivery is correlated with more resources, own revenue, staffing and capital spending per capita (Figure 1a,1b) Analysis indicates no clear relationship between service delivery and governance.

Figure 1a: Urban Capacities, Resources & Services Figure 1b: Own Revenue & Services

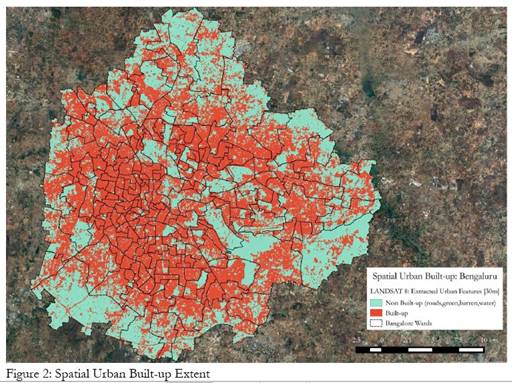

Currently, tax revenues are not constrained by inadequate taxation powers of ULBs. One promising source is property tax. The study done for the Survey shows that property tax potential is large and can be tapped to generate additional revenue at city level. Satellite imagery can be a useful tool for improving urban governance by facilitating better property tax compliance. The study has shown that Bengaluru and Jaipur are currently collecting no more than 5-20 per cent of their respective potentials for property tax (Figure 2).

Competition between States is becoming a powerful dynamic of change and progress, that dynamic must extend to competition between States and Cities and between cities. Cities that are entrusted with responsibilities, empowered with resources, and encumbered by accountability can become effective vehicles for competitive federalism and, indeed, competitive sub-federalism to be unleashed.