I. Introduction

In the previous article ‘IFC Reporting- Fresh Perspective beyond Compliance’, we have covered when the IFC will be applicable, the Responsibility of Management and Auditor while implementing IFC, advantages,and importance of IFC along with a case study. In this article, we are going to cover how the implementation of IFC will lead to the identification of various unidentified risks and weaknesses in various processes of the company, which may affect the financial reliability of the company. Once identified, through the IFC implementation process various suggestions, recommendations, and process improvement initiatives can be proposed for improving process efficiency and internal control. Therefore, in this article, our focus will be on how various risks can also be eradicated from the company process while implementation of the IFC.

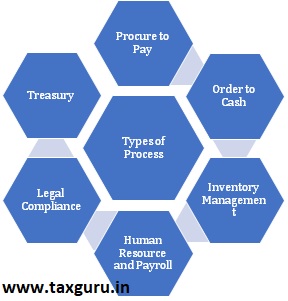

II. Various types of processes in the company

All of these processes form part of a major function of the companies. However, all these processes include some types of risks which can affect the functional ability and can be hazardous to the company.

> In the case of Procure to Pay,process starts with Making of PO and ends with making a payment to the vendor, However, the entire process flow goes in the following manner

> In the case of Order to Cash, the process start with Receiving sales order and end with collection of payment. However, the entire process flow is shown below

> Inventory Management becomes an essential process in the case of trading or manufacturing companies. The inventory process flow is as follows

III. Risks which can be involved in above processes

The followings are some examples of risks that exist in various types of processes.

> Procure to pay process includes major types of risk like, unauthorized and incorrect PO, delay in recording of the transaction, recording of transaction at an inaccurate amount which ultimately leads to paying incorrect amount or double payment.

> In Order to cash process, various risks like delay in order processing, delay and wrong recording of the invoice, not receiving of payment on agreed credit period, and not recording of the receipt.

> Inventory process may include risks like delay in recording of GRN, fictitious/Incorrect batch, not maintaining aging of inventory which leads to issue in tracing of expired inventory and not recording of inventory as per company’s policy/ prescribed accounting standards.

All these types of risks exist in various areas of the company and to overcome them companies are required to have internal financial control. Internal financial control helps the company not only to reduce risks but also to improve efficiency. However, it is not mandatory to have Internal financial control for all the companies. Provision of Companies Act, 2013 has stated certain types of companies,which must mandatorily have Internal financial control, to read more on applicability and advantages of IFC click on below mentioned link.

https://taxguru.in/finance/ifc-reporting-fresh-perspective-compliance.html

Now let us understand from the following example how while implementing IFC we can identify risk and weaknesses in company processes and how proposed measures by an IFC expert can eliminate the same.

IV. Case Study:

Aakruti Ltd is engaged in the pharmaceutical industry, which was incorporated in the year 2014 and was in a growing position. However, in the last few months, they are facing issues in the procurement process, which resulted in the delay in making payment to the supplier, and ultimately it was started affecting the creditability of the company.The company already had few controls existed in the company even after that it was facing certain difficulties. To overcome these difficulties the company has hired Mr. Sky, an IFC expert.

Mr. Sky started investigating and had a meeting with all managerial personnel linked with the procurement and warehouse team. Based ondata he has received and observations he made while taking a walk-through of the process, he came across a few unidentified risks and weaknesses in the process. Mr. John proposed the following controls for each risk and weaknesses to eliminate such risks.

| Process | Risk Description | Existing control | Proposed Control | Control Evidence |

| Invoice Processing & Payment | Incorrect invoices are processed in the system | The Invoice received from Procurement are booked in System as when received | In the case of material invoices, the Invoice value must be matched with GRN & at the same time, GRN is tagged against the invoice. If the invoice value is not matched with the GRN value, then no invoice shall be booked. First, it shall be sent to the procurement coordinator to solve the issue after that the only invoice should be booked. | Invoice and GRN matching |

| Process | Risk Description | Existing control | Proposed Control | Control Evidence |

| PO Clearance | Unauthorized / Erroneous / Fictitious materials procured and recorded / Procurement of goods with incomplete data in PO | PO is created by procurement department as and when requirement arises and same is forwarded to the vendor | Before the creation of the PO, the required department should give the indent for procurement. The indent must be approved by procurement HOD. Without the creation of Indent, no PO should be created. Indent reference in PO must be stated. | Indent approved by Procurement HOD |

| Invoice Processing & Payment | Duplicate payments / Manual errors while processing payments / Unauthorized payment to vendor / Payment to incorrect vendor | Payment made by Finance & Accounts Department as when intimation from vendor is received. |

The payment intimation must be given by Procurement manager & then it should be approved by Finance HOD then payment should be made. |

Proper Authorization |

V. Conclusion:

As it is evident from the case study above, implementation of IFC will lead to the identification of unidentified weaknesses and flaws in various processes and operations of the company. This can also be used as an opportunity for improvement in the process by recommending good practices and setting various benchmarks to develop and strengthen their process and internal control systems. It will result in enhancing the reliability of their financial statements and assurance that the company’s operations are conducted in accordance with the company’s policy and provisions of applicable laws and regulations.

In case you would like to know more on how can your organization benefit from implementation of IFC and how it will improve your company’s performance, you can reach us on our below mentioned e-mail ID.

*****

Authors:

CA Aakash Mehta | Partner | E-mail ID: aakash.mehta@masd.co.in

CA Punit Ruparelia |Director | E-mail ID: punit.ruparelia@masd.co.in

Sahil Rathod | Associate Consultant | E-mail ID: sahil.rathod@masd.co.in

Author Bio