IFRS 9

The financial crisis of 2008 was a wakeup call for all the financial and banking institutes as well as business entities of the world, that it was a time to have a fundamental change in the way finance is done. This global financial crisis was quite different from the previous one because this time banking giants from advanced economies were directly on the line of fire. The crisis was so severe that its impact was global and every major s well as minor economies felt the heat of it. This prompted global leaders and international forums such as G20, Financial Stability Board, and Basel Committee on Banking Supervision to unite and evolve new method to financing and managing it. In order to change the finance system finance reporting standard and financial instruments related standards of both IFRS Framework and US need to be changed too. So International Accounting Standard Board (IASB) and Financial Accounting Standard Board (FASB) worked together on war footing basis to undertake complete overhaul of standards on Financial Instruments.

By keeping IFRS standard 5 years worth of extensive time bound work was invested which resulted into globally standard, acceptable and robust financial instrument or its equivalent standards in various jurisdictions IFRS 9. As it was reported widely, transition to IFRS 9 was a monumental change which requires galvanization of entire organization and substantial cost and efforts. It is expected that benefits of changes brought by IFRS 9 outweighs the efforts and resources employed in successfully managing this huge transformation. IFRS has been able to maintain its superior quality globally accepted standards which bring in transparency, accountability and efficiency in the economy and financial capital market around the world. Time and time, it has been proven successful which led to its emergence as “Gateway to Global Capital Markets’. One of the key characteristics of high quality accounting standards is its robustness, to serve lager public interest and ability to capture the nature and type of economic events. In this overall context of global change, the ICAI undertook a project to evaluate the impact of worldwide implementation of IFRS 9, so that this impact study would provide valuable insights of these financial reporting reforms and also act as a guiding factor for banks and jurisdictions that will be transitioning to IFRS 9 or equivalent in the near future. Considering the importance of the matter, ICAI came out with publication on IFRS 9 Transition Impact on Banks across the Globe, which is a comprehensive study covering 75 banks from 26 global jurisdictions. Overall this study shows that even the prudential regulators of various jurisdictions had very positive opinion and were highly supportive of embracing this change.

Objectives, Sample Size and Limitations

The major objective of this study was to evaluate, how transition to IFRS9 have affected the equity of BFIs (banks and financial institutions) as of the transition date to IFRS 9. Another minor objective was to assess the extent of impact on regulatory capital ratio (commonly known as Basel Capital Ratio) of BFIs, which is a key parameter applied to ensure soundness and stability of the banking sector. The sample size of the study comprised of 75 BFIs headquartered in 26 jurisdictions that use IFRS Standards and evaluation was carried out solely by way of desk top review of audited financial statements. Since the samples for the study were selected randomly and one of the common factors here was the financial statements (F/S) available in public domain, as a result the sample size mostly comprises large internationally active banks.

The only limitation of this study was not being unable to analyze the impact on Statement of Profit or Loss or Income Statement due to lack of published information in this area as most of the entities have opted for exemption from restating the comparative financial information.

Key Findings- IFRS 9 Financial Instruments Impact

In order to find the true impact of IFRS 9 on finance institutions it is very much important as to observe its initial impact on various major finance institutes of several countries. The initial impact can be related to two areas of fundamental significance viz. Transition Exemptions in general and the overall approach towards Expected Credit Loss measurement. It was observed that all the 75 sample entities opted for not disclosing the prior year comparative financial information. Although this fact provided considerable operational relief to preparers, there would be data loss about IFRS 9 initial impact on the income Statement. Furthermore, most of the financial institutes have chosen to continue applying the hedge accounting requirements, which was the key area of previous standard IAS 39. Very few numbers of entities used prepayment features with negative compensation to IFRS 9 which was made very close to the mandatory effective date of arriving IFRS 9; this adjustment is considered to be of significant importance.

One of the interesting results about the primary approach being used by the entities in the applying the ECL model in relation to impairment loss component of IFRS 9 is that the majority of 72 out of the total sample 75 entities have reportedly based their ECL computations on sophisticated credit risk measurement parameters, which are Probability of Default (PD), Loss Given Default (LGD) and Exposure at Default (EAD). This outcome was predicted by keeping the advancement of credit risk measurement frameworks considered for prudential regulatory purposes and for internal risk management, expected in BFIs due to nature, size and complexity of their credit exposures and banking activities. Despite the result it was still uncertain in many of these cases whether those financial institutes have influenced their basal capital adequacy frameworks infrastructure used for discreet regulatory purposes. One of the major improvements brought by IFRS over previous standard was consideration of forward looking Information in ECL Measurement Techniques, which basically comprises of 3 scenarios- Base case, Downside and Upside. All three scenarios were considered along with several economic factors such as – Gross domestic productivity, Inflation, Crude Oil Price, which were found to be in the range of 3 to 8.

Overall Summary

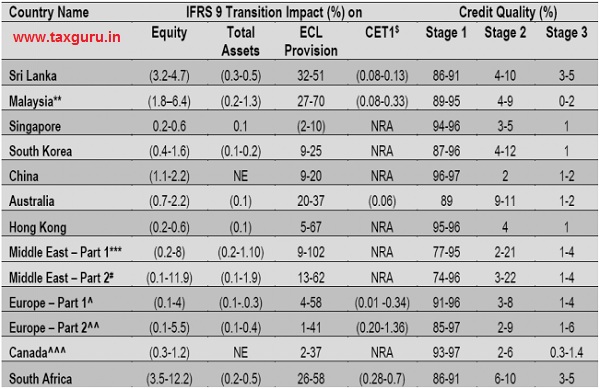

The final outcome of this study is summarized by explaining the transitional impact of IFRS 9 in the form of transition Impact (%) on, equity Total, Assets, ECL and Provision CET1$ (Core Equity Tier 1 under Basel III) . Following table exclusively presents all of the above information.

*Numbers in bracket indicate reduction

**In Malaysia, one entity had positive impact on equity and one entity had positive impact on CET 1

***In Middle East-Part 1, one entity had positive impact on total assets and one entity had reduction in ECL provision

# In Middle East-Part 2, one entity had positive impact on equity, one entity had positive impact on total assets and one entity had reduction in ECL provision

^In Europe-Part 1, one entity had positive impact on total assets, one entity had reduction in ECL provision and two entities had positive impact on CET 1

^^ In Europe-Part 2, one entity had reduction in ECL provision

^^^In Canada, one entity had positive impact on equity and one entity had reduction in ECL provision

$CET1 on Fully loaded basis

NE= Negligible

NRA = Not readily available

Table 1: High level summary of quantitative impact in respect of a few critical parameters

Following are the major outcomes of the study-

1) The total equity has had negative impact and in some jurisdictions such as= Malaysia, Middle East-GC, Europe-Part 2. However South Africa had more pronounced impact of it. Rest of the remaining jurisdictions had insignificant changes on their total equity and impact appears to be not material.

2) The key components where significant and direct impact of IFRS 9 can be observed as follows-

a) ECL approach for recognition and measurement of impairment loss appears to have reduction in Equity in all jurisdictions except for one. This phenomenon can be explained by looking at the increased amount of impairment loss allowances. In some exceptional jurisdictions, the negative impact of ECL is partly offset by deferred tax benefits on these impairment loss allowances.

b) One of major change after arrival of IFRS 9 was reclassification and consequential changes in measurement principles because of reclassification among measurement categories based on new criteria added in IFRS 9. Overall the effects of these reclassifications have positive impact on equity. The reclassifications are largely concentrated in FVTPL and FVOCI categories and due to application of SPPI Test. Apart from FVTPL and FVOCI there are reclassifications of material gross carrying amounts also, but its overall quantitative initial impact on Equity is found to be on insignificance.

c) One of the striking features of the IFRS 9 is that the overall impact is reportedly concentrated in Financial Assets area. There have been barely any changes in respect of Financial Liabilities except for one or two entities out of 75 entities, other than that the financial liabilities have been of no concerns.

d) The new Hedge Accounting Framework featured in IFRS 9 have no major observable impact that was reported by any of the international banking financial institutes.

3) All the selected 75 financial entities have not reported any Basel regulatory impact of IFRS9. This data was readily available in case of only 19 BFIs and generally trend is reduction in CET1 ratio, but magnitude of reduction appears to be very low.

4) IFRS 15: No material impact on Equity has been observed. BFIs have generally reported some changes in the presentation and disclosure areas and not the recognition and measurement areas.

It has been almost a decade since IFRS arrived and many of players in the global economy were eagerly waiting for the outcome of revolutionary changes in the financial reporting world of banking sector i.e. implementation and initial impact of IFRS 9 or its local equivalent (hereinafter referred to as IFRS 9). Financial Statements of Banks and Financial Institutions (BFIs) for the year ending 2018 in many jurisdictions visibly indicate the radical reform of IFRS9 and its initial impact on their financial position.

IFRS 9 have unique mixed measurement model and the multicomponent (or building blocks) structure of its predecessor IAS 39. The measurement models from balance sheet perspective of IFRS9 are dependent on cost (or Amortized Cost) and Fair Value. The approaches to recognize the fair value changes in the statement of financial performance or Total Comprehensive Income are again dependent on Fair Value through Profit or Loss (FVTPL) and Fair Value through Other Comprehensive Income (FVOCI). In order to achieve the above, classification of financial assets and financial liabilities into different categories and the principles behind those classifications played a central role. Other two key building blocks of the standard are Impairment and Hedge Accounting1. IFRS 9 brings paradigm shift in all three building blocks of a high quality robust standard on financial instruments.

Overall IFRS 9 was much needed change for global economy. It was clear from the study that world can no longer rely on old tactics of managing finances and take financial decision based on that. On the face value IFRS 9 appears to be a new robust methodology to follow as a global standard and its initial impacts have been very positive. Although there have been some negatives of IFRS 9 and fair share of critics of it, it can be fairly managed by further optimizing the parameters. Overall future looks promising with arrival and proper implementation of IFRS 9.

Above article is based on study published by CA. Prafulla P. Chhajed June 29, 2019 President, ICAI with valuable efforts of CA. M.P. Vijay Kumar (Chairman, Accounting Standards Board), CA. (Dr.) Sanjeev Singhal, Vice-Chairman, Accounting Standards Board and several members of the Board.

Author Bio