Introduction:

Yes Bank which was once India’s Forth Largest Private Sector Bank, is now struggling for its survival. Under the management headed by Rana Kapoor, the bank has grown its loan book manifold in very short span since its inception. Yes Bank’s business includes banking and financial services, AMC services and UPI services etc.

On 05th March 2020, RBI imposed 30 Days moratorium (Not on account of Covid) on the bank and replaced entire top management in order to avoid collapse of the bank. Due to Moratorium and other revealed issues, bank has lost its goodwill and trust. RBI granted Rs 50,000 Crores as emergency fund to the bank for its operations. This article covers the instances that almost led to collapse of bank in birds eye view & whether the bank is on correct way to its turnaround.

What Happened with Yes Bank?

– Increase in NPA due to bad loans & Money Laundering

Rana Kapoor, the founder of Yes Bank, was very good at sanctioning loans and getting the same back from corporates. But on his way to increase the loan book of the bank, he started to treat the bank as his own piggy bank and started giving loans even to financially distressed companies and which are in losses and negative networth companies but started showing NPA less than actual. Yes Bank has made funding to most of the big companies which are under insolvency now. Below table shows the list of default loans (In Crores) given by Yes Bank:

| Particulars | Amount |

| Anil Ambani Group | 12,800 |

| Essel Group | 8,400 |

| DHFL ## | 4,735 |

| IL&FS | 2,500 |

| Jet Airways | 1,100 |

| Cox & Kings | 1,000 |

| BM Khaitan | 1,250 |

| Omkar Realtors | 2,710 |

| Radius Developers | 1,200 |

| CG Power (AG) # | 500 |

| 36,195 |

# Birds eye view of Loan to Avanta Group (AG):

One of the group company of AG has obtained loan from ICICI bank and DCB by keeping a property valuing 550 Crores in prime location of Delhi as collateral. Same company has entered into an LRD^ agreement with Yes Bank under which the bank has granted a credit of Rs 400 Crores to the group.

Before availing LRD facility, the same property was given on rent at Rs.1.02 Crore p.a. (i.e., Rs 8.5 Lakhs per month) to a group company. But as per new agreement on which LRD was availed, lessee (another group company) will pay lease rental of Rs 65 Crore every year with escalation of 5% every year (which is around 64 times of previous rent). Further, after sanctioning the loan, no rent was remitted by latter tenant.

Repayment schedule of said loan was reading that amount of principal loan repayment for the first one year will be Rs. 5 lakh per month (Almost 1% of Monthly rentals) to keep the loan as standard.

Loan from Yes Bank was used for repayment of previous loans (i.e., to ICICI & DCB). Both, AVL (the borrower) and BGPPL (The latter tenant), were financially distressed companies and were not eligible for the loan with hundreds of crores of existing liabilities.

After the above transaction, property which was kept as collateral with Yes Bank was purchased by a company which is owned by daughter and wife of Mr Rana Kapoor at a price far less than the market value. This is a clear case of Money Laundering. (Source – FIR filed against Rana Kapoor and his group companies)

^ LRD (Lease Rent Discounting) is an agreement whereby borrower gets discounted value of future rent as loan from lender and future rent payments will be used to repay the loan.

## Out of the Loans given to DHFL (one of them amounting to Rs.750 Crores) was given by keeping land worth 39.66 Crores stating the valuation as 735 Crores on the assumption that these agricultural lands will be converted to residential with permission of local authorities and will be used for construction and eco-tourism activity. In return, group has paid a kickback of Rs 600 crore to Kapoor and his family members under the garb of loan of the same loan from DHFL, according to the ED

There are allegations that part of the loan amount given by the bank to some of the above mentioned distressed companies (other than above) was transferred to the group companies of Kapoor as Money Laundering.

– Underreporting of NPA

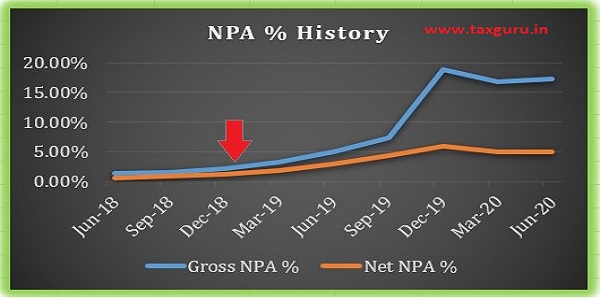

Since loans were given to financially distressed companies, NPAs as a percentage of Loan Book was increasing continuously but the same was misreported for a long time. Further, RBI imposed Rs 6 Crores penalty on yes bank over non-compliance related to disclosure of bad loans. RBI found that actual NPAs of the bank were 5X the reported numbers. Below image depicts the same.

After Rana Kapoor was ordered by RBI to step down from his positions in Yes Bank during Jan-19, Original NPAs started reporting.

– Mismanagement & Weak Corporate Governance

Following incidents evidences mismanagement in the bank:

* Rana Kapoor has granted various loans without complying with regulatory norms for personal benefit

* Willful underreporting of NPAs over long period

* Non-reporting of pledged shares held by Rana Kapoor

* Three Independent directors left the company in short span

* Appointment of additional director by RBI to check Corporate Governance issues closely

Why Govt should try to revive a Private Sector Bank?

If a company fails to pay its dues or unable to carry its business, it shall be either dissolved or be moved to Insolvency Board for starting of the process of Insolvency. In the instant case, RBI and Government along with it’s owned enterprises like SBI has prepared a revival plan when the bank was about to collapse due to Governance Issues and Mismanagement. It was done not because Govt found competitive advantage / exceptional business strategy in the bank but for following reason.

Banks deal with huge volumes of money, and trust is of paramount importance in this case. If Yes Bank was allowed to collapse, then it will create a fear and loss of trust on private sector banks and may lead to disruption of business of all players in the sector. Because, whenever such an incident happens with a public sector bank like SBI or PNB or IDBI Bank, Government funds money to it for conducting the business but this can’t be done in case of private sector bank.

Is it on the right way to turnaround?

It is now too early to decide that the bank is out of danger since only 5 Months has elapsed from RBI imposing moratorium and owing to ongoing covid issues. However available financial & non-financial data after the moratorium period can be used for understanding the direction.

– Comparison of Financial Results

We should compare the YoY performance because comparison with the Q1 of the last financial year is not meaningful due to reconstruction of the bank. However, QoQ (Quarter-on-Quarter) and YoY (Year-on-Year) comparison of data is being tabulated as it works as quick reference for desired ratios in medium to long period:

| Particulars | Q1-21 | Q4-20 | Q1-20 | QoQ | YoY |

| Net Interest Income | 1,908 | 1,274 | 2,281 | 49.76% | -16.35% |

| Non-Interest Income | 621 | 597 | 1,273 | 4.02% | -51.22% |

| Total Net Income | 2,529 | 1,871 | 3,554 | 35.17% | -28.84% |

| Operating Profit | 1,147 | 106 | 1,959 | 982.08% | -41.45% |

| PAT | 45 | -3,688 | 114 | NA | -60.53% |

| Provisions | 1,087 | 4,872 | 1,784 | -77.69% | -39.07% |

| Deposits | 1,17,360 | 1,05,364 | 2,25,902 | 11.39% | -48.05% |

| Net Advances | 1,64,510 | 1,71,443 | 2,36,300 | -4.04% | -30.38% |

| CASA Ratio | 25.80% | 26.60% | 30.20% | -3.01% | -14.57% |

| PCR | 75.10% | 73.80% | 43.10% | 1.76% | 74.25% |

| CET I Ratio | 6.50% | 6.30% | 8.00% | 3.17% | -18.75% |

| GNPA 1 | 17.30% | 16.80% | 5.01% | 2.98% | 245.31% |

| NNPA 2 | 4.96% | 5.03% | 2.90% | -1.39% | 71.03% |

| LCR | 114.10% | 37.00% | 132.60% | 208.38% | -13.95% |

1 Gross NPA percentage though increased in QoQ, was actually reduced by Rs 175 Crores. Increase in GNPA% was due to shrink in loan book.

2 Net NPA decreased by Rs 466 Crores on QoQ as a result of better provision coverage

Following extracted data of Q1 FY 21 provides additional financial information:

* Higher NIM (Net Interest Margin) at 3.0% up ~109 bps QoQ

* 26.4% QoQ growth in CA deposits and 12.6% QoQ growth in term deposits

* Operating costs declined ~ 21.7% QoQ

– Loan Book Mix & NPA Share:

* Majority (i.e., about two-third) of the loan book consists of Corporate Loans and 96% of the NPAs are of corporate loans from long period.

* Out of its total loan book of Rs 1.64 lakh crore, about 56% of the book (i.e., Rs.92,631 crore) is still corporate loans while retail book is still only about 23%. The high reliance on wholesale loans continue to pose challenges to the bank.

* Out of the Gross NPAs of Rs 32,702 crore, Rs 31,426 crore is corporate NPAs, while retail and SME contribute only Rs.455 crore and Rs.380 crore.

– Recovery of Toxic Assets:

New Management has started recovery procedure of toxic assets so that it can give liquidity and to make good the loss & decrease of NPAs such as:

* Took possession of Reliance Centre Building [Head Quarters of Anil Dhuribhai Ambani Group (ADAG)] following loan default under SARFESI Act.

* Has acquired over 24 percent of stake in dish TV India on 30 May 2020 by invoking pledged shares.

– Competitive Advantage:

To increase goodwill of the bank and obtain trust in the business, bank has to obtain a competitive advantage in the market or find a niche market where it can focus and be a market leader so that it can remain in business.

Yes Bank is a leader in providing UPI services in the industry and continues to be the leader even now. It provides UPI services for a number of major companies such as Airtel, Cleartrip, RedBus, and PhonePe among others. It accounts for 35%+ market share with processing transactions worth One Lakh Crores in Jun-20. It is No 1 bank in IMPS remittance.

Though it is a market leader in above segment, revenue generation from above segment is very low as compared to its main business. So, bank has to improve its other revenue streams so as to survive in the market.

– External Factors & Indicators:

As per RBI’s Financial Stability Report, GNPA ratio of private sector banks may increase from 8.5% in March 2020 to 12.5 % (14.7 per cent in a very severe stress scenario) by March 2021. GNPA as per latest released data is 17.30%. Any further increase may pose threat to viability of the business.

Covid-19 poses additional threat to the business. 85%+ of the customers of the bank who opted for moratorium are having good credit history and has not defaulted repayment previously but, even if 10% of the book goes bad, the amount of provisions required will wipe out a good chunk of its survival capital.

– Recent developments in the bank

* Successfully raised Rs 15,000 Crores by FPO within 5 Months of Moratorium which gave a temporary relief to the bank

* Moody’s Investors Service upgraded Yes Bank’s long-term foreign currency issuer rating by a notch to ”B3” from ”Caa1” after capital raising. Despite the upgrade, Yes Bank still remains under non-investment grade.

* LIC purchased 105.98 crore shares, reflecting 4.23% stake, of the bank from the open market. Prior to this, LIC had 0.75 per cent stake in Yes Bank through 19 crore shares held. In all, LIC’s holding in the bank increased to 4.98% through 125 crore shares held. The period of acquisition is between September 21, 2017, and July 31, 2020, it said

* It has repaid Rs. 25,000 Crores (50%) till date towards the RBI special liquidity facility

Conclusion:

Solving Yes Bank’s NPA puzzle will be a daunting task for Prashant Kumar (New CEO appointed by RBI) and his team, especially in the wake economic slow-down followed by Covid-19 outbreak. As of now, bank has started its way to turnaround but a keen attention to its financial & non-financial indicators for medium to long term period may be required to check the way where it is leading.

*****

Disclaimer: The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.