This article does not cover as to needs of investing and requirement for the same. It mainly covers pros and cons of various modes of investment. Investing provides various benefits as follows:

♦ Achieving financial goals & obtaining financial freedom

♦ Wealth Creation

♦ Tax Saving

♦ Conquer Inflation

♦ Family & Personal life inflation etc.

TYPES OF INVESTMENT IN INDIA:

Let’s see the most popular investment options available in India. Major characteristics of all types of investment are tabulated here for easy reference & quick decision-making:

- SAVINGS ACCOUNTS:

- Description– It is a classic mode of investment. This term does not require a formal description as everyone knows about the same (even though not in formal terms). It refers to parking money in one’s bank account.

- Pros

- Promotes investment in early stages.

- Ensures liquidity and no lock-in.

- Better than saving money by keeping it in one’s pocket since it provides minor interest income too.

- Allows automated bill payments.

- Cons

- Minimum balance requirement which is absent in other modes of investment.

- Provides return less than the inflation rate and hence decreases purchasing power parity.

- Compounding will be done quarterly (in most of the cases), hence the full potential of interest income cannot be earned.

- Interest rates are subject to periodic change.

- Best for

- Keeping emergency fund.

- Maintaining balance for automated payments like credit card bills, EMIs, etc.

- Saving money till alternative investment options are found.

- SENIOR CITIZENS SAVINGS SCHEME (SCSS):

- Description– SCSS is a Government-backed savings instrument offered to Indian residents aged over 60 years.

- Pros

- Provides interest rate more than all other small savings schemes

- The minimum amount of investment is Rs 1000.

- Investment can be done at any bank/post office.

- Provides interest more than Tax Saver Fixed Deposits.

- Deduction for the purpose of computation of Income Tax Under Section 80C (up to Rs 1,50,000 p.a.).

- Deduction for interest income is available for up to Rs 50,000 p.a. for Income Tax Under Section 80 TTB (in case of senior citizen).

- Option to extend maturity is available to the deposit holder.

- Investment can be made by persons attained the age of 55 years subject to certain conditions

- Cons

- The maximum possible investment is Rs 15 Lakhs per person

- The maximum possible investment through cash is Rs 1 Lakh

- Even though pre-mature withdrawal is allowed after one year, it is subject to a penalty of 1.5 % if withdrawn before 2 years & 1% if otherwise

- Interest rate is subject to periodic change by Government.

- Interest payments are made annually.

- Best for

- Senior citizens who require income for meeting their living expenses

- Senior citizens planning to opt for Tax Saver Fixed Deposit

- Persons opted for VRS after attaining 55 years.

- FIXED DEPOSITS:

- Description– It is a financial instrument provided by banks and NBFCs which provides interest higher than a regular savings account.

- Pros

- The interest rate is more than a regular savings account.

- The higher interest rate for senior citizens.

- The flexibility of amount and term of the investment.

- FD can be made for a period as low as 7 days

- Interest rates are known at the beginning by which one can know the amount of income he is going to earn

- FDs (Other than tax-saving deposits) are liquid, instant credit to the bank account on account of closure.

- A loan against deposit is also possible up to the margin specified by the bank.

- Can be used as a tax-saving tool since FDs having a maturity of more than 5 years are allowed as deduction Under Section 80C to calculate income for computing Income Tax thereon.

- Deposits (including interest) of up to Rs 5,00,000 are secured by Deposit Insurance and Credit Guarantee Corporation

- Cons

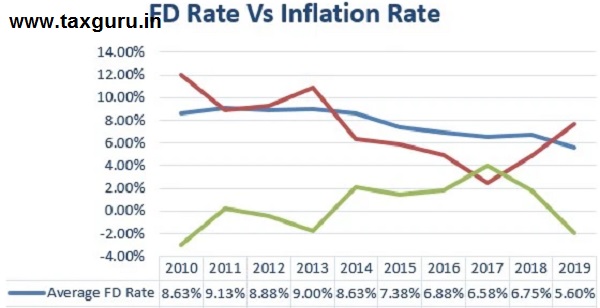

- Returns from FD does not cover inflation and hence cannot provide for purchase power parity. The below image depicts the same:

FD Rate – Average FD rate for one year as per ‘Handbook of statistics of Indian Economy’ released by RBI; Inflation Rate – as reflected by Consumer Price Index

-

-

- Requires lock-in for a certain period for claiming tax exemptions.

- Even though other FDs do not require lock-in, in case of pre-mature withdrawal, a reduction in the interest rate and penalty imposed will reduce incremental income from the same.

- FDs can be used as a tax-saving tool but if we opt for the same, funds will be blocked for 5 years at a very low rate of interest.

Partial withdrawal is not allowed. - The interest rate in the current scenario is decreasing. Hence, even if you invest in FDs when the interest rate is high when you want to re-invest the proceeds after maturity, interest rates will be less than the current rate (in majority of the cases)

- Even though default risk is rare but it is in existence.

- Best for

- Individuals (Non-senior citizens) planning for tax planning with a predetermined rate of income

- Parking funds for a short duration with predetermined income

- Parking funds for emergency (since the time taken in the closure of FD and credit into a bank account is almost nil)

-

- RECURRING DEPOSITS:

- Description– It is a special kind of term deposit by which account holders can park a specified part of their income as a Fixed Deposit and earn interest equal to a Fixed Deposit. Since all features of FD apply to RD, the Pros and Cons mentioned above are applicable here also.

- Pros

- Term of as low as Six Months

- Helps to create a short-term corpus with minor investments.

- Flexi RD, where the account holder can invest a flexible amount as per his convenience is allowed with certain conditions.

- Interest rate is fixed for the entire term at the beginning itself (if every installment is created as a separate FD, distinct ongoing interest rates are applicable for the same)

- Cons

- Same as Fixed Deposits.

- Best for

- Persons who are willing to accumulate an amount that is less than the minimum amount for which FD is allowed.

- Persons who are willing to accumulate a part of their income for a predetermined interest rate.

- PPF (PUBLIC PROVIDENT FUND):

- Description– PPF is a tax-free saving scheme regulated by the Indian Government. It is a long-term investment scheme popular among individuals who want to earn stable and predetermined returns with low risk.

- Pros

- Can be used as a tax-saving tool since deduction under section 80C is available for the contribution made.

- Interest income from the PPF account is also exempt from tax.

- PPF account can be opened with any bank.

- Can be extended beyond the original term of 15 years by blocks of 5 years.

- Investment can be started from as low as Rs 500.

- Investment can be made for a predetermined rate of return.

- The frequency of deposits can be extended up to 12 times a year.

- Since it is offered by Government, risk-free returns as well as capital protection.

- Cons

- The minimum tenure is 15 Years and hence lock-in of funds at a low rate of return.

- Closure of account is permitted only after completing 5 years.

- Partial withdrawals are allowed only after the completion of 6 years.

- An annual investment of more than Rs 1.5 Lakhs will not earn any interest and not eligible for tax-saving.

- Best for

- Individuals who want to create corpus with a long-term outlook.

- Individuals opting for risk-free investment opportunities with tax benefits.

- EMPLOYEE PROVIDENT FUND (EPF):

- Description– EPF is a scheme that helps employees to save corpus for retirement where both employee and employer contribute a certain percentage of their salary to the fund which is being managed by EPF Organization.

- Pros

- Contribution to EPF is compulsory for employees having a salary of less than 15,000 per month. Hence it promotes investment among low income earning individuals.

- Can be used as a tax-saving tool as it comes with EEE (Exempt – Exempt – Exempt) concept. The contribution made to EPF is eligible as a deduction from tax, interest and maturity proceeds (if withdrawn after 5 years) are also exempt from tax.

- The interest rate is generally higher than that of FD/PPF/SSCS.

- Contribution can be made by an employee (over and above specified percentage) to earn a higher return.

- Withdrawal is also possible in certain circumstances subject to certain conditions.

- Balance in the account can be obtained by a missed call/SMS too.

- Cons

- Withdrawals before maturity are subject to tax over and above the specified limit.

- Employer’s contribution is limited to a specified % of Rs 15,000 irrespective of employee’s contribution.

- Even though the rate of return is higher than FD, but the real rate is very less when inflation is taken into account.

- Not mandatory for employees working in a specified class of entities.

- Not applicable for persons working as consultants.

- Best for

- Employees earning low income to accumulate a corpus

- Accumulating corpus earning income at a specified rate of income without any risk and tax impact.

- NPS (NATIONAL PENSION SCHEME):

- Description– NPS is largely focused on one’s retirement. While up to 60% of the maturity corpus can be withdrawn as a lump sum on maturity, the balance is compulsorily annuitized, i.e., balance is used to fund the annuity (pension) after retirement.

- Pros

- The fund is managed by professional, qualified, and experienced fund managers, and hence returns are expected to be higher than EPS.

- NPS Account can be opened at any bank and in multiple modes which promotes easy documentation and accessibility.

- No restriction on the frequency of contributions.

- Can be started with a minimum investment which can be made by multiple modes.

- Even though NPS funds are not maintained by Government but are regulated by Government which ensures safeguarding.

- Can be used as a tax-saving tool and deduction can be claimed up to Rs 2,00,000 subject to certain prescribed conditions.

- An investor can open multiple accounts (Tier-1 & Tier-2) which provides investment into multiple modes of investment.

- Withdrawals are permitted (from Tier-2 account) subject to certain restrictions.

- Cons

- Corpus upon withdrawal is subject to Income Tax (Unlike PPF, EPF).

- Subscribers cannot invest more than 50% of total investment in NPS towards equities.

- Even though NPS offers higher returns, but returns are not predetermined and hence subject to some risk.

- Best for

- Individuals (Employees/Others) who wish to invest with long-term horizon and variable returns with minor risk.

- Individuals who wish to contribute amounts without any pattern/period.

- PRADHAN MANTRI VAYA VANDHAN YOJANA (PMVVY):

- Description– PMVVY is a pension plan for senior citizens managed and operated by LIC which provides for the assured return of a certain specified percentage of return payable at such frequencies at the option of the investor. Investment is available till 31.03.2023.

- Pros

- Loan up to 75% of principal is allowed after 3 years of the policy.

- Premature withdrawal of up to 98% (balance 2% is a premature penalty) is allowed for medical/other specified emergencies.

- No maximum age for entering into policy.

- The minimum investment is Rs 1,000.

- The amount can be invested for a predetermined return.

- Since the scheme is handled by LIC, low/minimal risk of default of principal and interest.

- Cons

- Pension is payable at the end of the period.

- The minimum term of the policy is 10 years.

- The maximum amount of investment one can contribute is Rs 15 Lakhs.

- Returns from the scheme are not exempt from Income Tax.

- Best for

- Senior citizens who wish to receive fixed periodic income.

- SUKANYA SAMRUDHI YOJANA (SSY):

- Description– SSY comes with many useful features that can help the girl child meet her future requirements by providing financial assistance and lead a comfortable life. This scheme provides an interest rate higher than schemes with similar interest and lock-in period schemes.

- Pros

- EEE Exemption like in the case of EPF.

- SSY account can be opened at any commercial bank/post office.

- Interest rates are normally higher than FD.

- No risk of default of principal and interest since backed by the Government.

- Can be used as a tax-saving tool since deduction Under Section 80C is available for the same.

- The minimum amount of deposit is Rs 250.

- Cons

- Not idle for short-term since the deposited amount can be withdrawn only after the girl child attaining 21 years of age.

- Premature withdrawal is allowed only after attaining 18 years of age.

- The interest rate is not predetermined.

- The maximum number of accounts that can be opened is Two. Hence one cannot open an SSY account for a third girl child.

- The maximum amount that can be deposited into the scheme is Rs 1,50,000 per annum.

- SSY account cannot be opened for a girl child who has crossed 10 years of age.

- SSY account cannot be operated online.

- Best for

- Parents who wish to accumulate a corpus for the girl child with a long-term perspective.

- MUTUAL FUNDS:

- Description– Mutual Fund is a type of investment vehicle where money pooled from investors is being invested by Asset Management Company into assets as per scheme approved. There are various types of Mutual Funds like Debt, Equity, Hybrid, Commodity, index funds, etc. The pros and cons of each major category of the fund are discussed individually below. Same in general applicable for all Mutual Funds are discussed here:

- Pros

- Funds are managed by professionals which reduces the risk.

- Research and data required for investing are being collected by various fund themselves as well as other brokers.

- These investments are liquid (except tax saver funds).

- Can start investment from as low as Rs 100.

- With mutual funds, one can invest in companies having higher share price with minimal investment (In case one would like to invest in MRF Ltd whose share price is around Rs 75,000 can invest the same through mutual funds with a minimal amount like Rs 500/Rs 1000 depending upon features of the fund).

- AMCs that manage mutual funds are regulated by SEBI and other regulatory bodies on a timely basis which ensures safety and transparency.

- Certain types of mutual funds provide for passive income like a dividend.

- DEMAT account is not required for making investments in mutual funds.

- Investing in mutual funds is easy and automated payments can be made for Systematic Investment Plans (SIPs).

- There are various types of mutual funds that provide a choice of investments considering one’s financial goals, risk-taking abilities, etc.

- Cons

- Returns are variable and hence subject to volatility on account of market factors.

- Unitholder needs to endure tax payments on the transfer of units by himself as well as on the transfer of securities by AMC.

If the investment is done after the cut-off date on a particular day, units are allowed based on NAV on the succeeding working day which does not ensure - The majority of the funds (except dividend funds) does not provide for passive income.

- Even though diversification reduces the risk of loss, it also averages profit and hence extreme returns cannot be expected.

- Points to be considered – invest in MF having–

- High AUM (Assets Under Management) since the adverse effect of any part of investment does not affect the value of the portfolio and also usually funds with high AUM often tend to have low expense ratio (impact of the same is discussed in detail below).

- Has a history of giving good returns.

- Has lower portfolio turnover ratio (i.e., number of transactions is less which leads to low transaction costs ensures good returns).

- Higher NAV does not mean good returns. In other words, a fund with a NAV of Rs 10 & a fund with a NAV of Rs 1,000 with the same return (say 10%) are the same.

- Direct mutual funds rather growth-oriented one (since expense ratio is less)

- Low Expense Ratio – one may ignore this as it ranges from 0.5 to 2%. In long run, it does show a big impact on investment having the same other characteristics as depicted below:

0.67% of expense ratio led to Rs. 39,000 extra return to the investor in the former case (with other variables assuming constant).

-

-

- Rating given by various institutions.

- Low/No Exit Load.

- Best for– investors who want to take a calculated risk with diversification and returns outstanding inflation.

-

- Equity Oriented Mutual Fund– A Type of mutual fund which invests at least 65% of scheme assets in equity and equity-oriented instruments.

- Pros

- Provide for better returns when compared to other types of funds.

- ELSS funds provide for deduction under Section 80C of Income Tax (up to Rs 1,50,000 per annum) with a duration of 3 years (being the shortest of all other class investments eligible for similar deductions).

- Provides a wide range of options like small-cap, mid-cap, large-cap, sectoral thematic, focused 50, etc. at times, it acts as a con since it creates confusion among investor.

- Index funds (being one of the types of EOMF) have the least expense ratio.

- Generally, has a predetermined exit load.

- Cons

- Returns are more volatile than other funds like debt funds etc.

- Short-term investments can be riskier.

- Not suitable for investors having less risk appetite/risk-averse investors.

- The expense ratio is generally high since an in-depth analysis of equity needs to be made.

- Pros

- Debt Oriented Mutual Fund– a mutual fund scheme that invests in fixed income instruments, such as bonds issued by the government and corporate, debt securities, and money market instruments, etc.

- Pros

- Less volatile when compared to equity-oriented funds.

- Funds can be parked in short/ultra-short/over-night funds that have no exit load.

- Provides stability to the portfolio in terms of risk and returns.

- Do not over-react to equity market and economy conditions.

- Less risky when compared to equity-oriented funds. Certain types of debt funds (Gilt funds etc.) has no/very low risk. CRISIL Long Term Gilt Index as shown below depicts low volatility of funds:

- Pros

In Mar’20 to May’20 when stock market fell about 50%, Long Term Gilt Index fell around 7% making it less volatile.

-

- Cons

- The past trend shows returns are lower than equity-oriented funds.

- They are not risk-free assets and possess low risk (on account of interest rate, currency risk, etc.)

- Cons

- Commodity Funds– As the name suggests, they invest in commodities such as gold, silver, agricultural products, energy resources, etc. Investment can be in the form of physical holding or buying future contracts or related companies.

- Pros

- Storage cost and other maintenance costs, which otherwise are required to be incurred on the purchase of investment in physical form are not required to be incurred.

- Some of the commodities like gold and silver move against the stock market and hence it provides for a hedge against losses.

Offers diversification to the portfolio. - Investment can be made with little amounts which are not possible in the case of direct holding of commodities.

- No chance for price disparity which may happen in the case of physical holding of commodities.

- Cons

- Does not provide for any passive income.

- Changes in the price of the commodity on which the fund is normally constructed do not support any evidence for the same.

- If an investor wants to hold the commodity on which he has bought units of the fund, there is no other way than redeeming the units and buying the same in physical form.

- Pros

- GOLD:

- Description– Needless to say in detail, Investment in gold refers to buying gold in physical form as a gold biscuit/ornament. It is seen as a classic mode of investment for parking funds.

- Pros

- Investment can be made at any time, any place.

- Easy to buy/sell.

- Seen as a quality hedge against down market.

- A real asset with limited supply.

- Return always beats inflation (as per historic figures).

- Provides diversification for the portfolio.

- Cons

- GST needs to be paid on purchase and sale (if registered).

- The threat of theft, loss due to wastage, etc.

- Additional maintenance costs to be incurred if gold is bought as an ornament.

- Storage & Maintenance Cost needs to be incurred.

- Investment in Gold Funds is seen as an alternative option that can serve all the above points.

- It earns money only when you sell it. It does not earn any passive income.

- Price of gold changes sometimes purely due to demand and supply since it does not have any basis for the determination of price. Sometimes, the price can be speculated.

- The rate of return for a specified period cannot be expected since the price does not follow a pattern.

- Best for

- Investors who want to diversify their portfolio into a new segment.

- The best investment to hedge downside risk.

- BONDS:

- Description– Bonds refers to fixed income securities issued by corporates. There are various types of bonds depending upon term, interest rate, risk etc.

- Pros

- Provides periodic income.

- The predetermined rate of income and capital.

- Has a low risk of default (when compared to equity).

- Often liquid since traded on different markets but not as liquid as stocks.

- Investment can be made through debit funds for bonds that cannot be invested through a recognized market.

- Cons

- A periodic review of credit rating needs to be done.

- Bonds are not as regulated as stocks/mutual funds.

- Price changes due to market conditions and required yield and lower than that of equity.

- Even though not subject to interest rate risk, but subject to the exchange rate, volatility, inflation, credit, and solvency risk.

- Best for

- Investing a portion to diversify portfolio into a stream with regular income.

- Reduces Beta (change in the value of the portfolio with that of the market) to an acceptably low level.

- REAL ESTATE:

- Description– This term does not require any particular explanation. It includes investment in immovable properties.

- Pros

- Provides passive income like rent.

- All benefits can be obtained with a down payment and with the use of leverage (i.e., by use of loans) which is not present in any of the remaining portfolios.

- Provides diversification to the portfolio.

- Has a history of appreciation over a while, has a remote risk of diminution in value.

- Even though gain on sale is taxable, a deduction can be obtained from the same by investing in other properties/specified bonds.

- Since supply (i.e., availability of land) is limited, price is always expected to increase over a while.

- Provides hedge against inflation.

- Cons

- Investment can be made only with a long-term perspective.

- Often illiquid since we need to find a buyer for sale which may take time.

- Huge registration cost involved on transfer.

- Always overreacts to market conditions.

- The transfer cannot be made online/physical presence is required for transfer.

- Requires additional cost by way of maintenance and insurance.

- Risk of the dispute of ownership.

- Alternative investment mode of investing in REIT bonds can be made.

- Need familiarity with the market before investing.

- A definite exit strategy is required for this market.

- Investment in properties creates liabilities (if levered).

- Best for

- Parking funds for diversification with periodic passive income.

- Parking fund with a long-term perspective.

- STOCK MARKET:

- Description– It is a secondary market where securities of various companies listed on a recognized stock exchange are listed.

- Pros

- Provides for returns higher than other forms of investment (if the same is made after proper analysis).

- Sensex & Nifty has given a CAGR of more than 15% since inception. The best method of investment to beat inflation.

- The liquid in nature and funds can be withdrawn within a short time.

- No activity requires physical presence.

- Easy to buy & sell.

- The cost involved in acquisition and transfer is minimal.

- Provides passive income in nature of dividend, rights premium, etc.

- Gain from sale of shares is taxable at a rate lower than other income (In case of Long Term – 10% and for Short Term – 30%)

- Cons

- Is often risky and not suitable for risk-averse investors.

- Has more losers than winners since most of the people invest without doing the required analysis.

- Proper analysis of the market is time taking.

- In the case of trading, brokers can eat into profit margins.

- Is very volatile.

- In the case of liquidation (very rare), share-holders are given last preference when comes to payment.

- Liability may arise up to the portion of the unpaid amount.

- Most of the investors are often trapped by an emotional roller coaster by which they will tend to hold even if the price falls and buy even if the stock is over-priced.

- Has common belief as gambling.

- Best for

- Individuals have proper knowledge of the market, economy, and company and the capability of analyzing the same.

- INSURANCE:

- Description– It is a contract by which one party agrees to indemnify risk of loss on receipt of consideration in nature of premium. Even though, primarily it seems like protection of loss, certain types of life insurance policies also serve investment purposes. Other types of insurance (like health insurance, burglary insurance, etc.) does not serve investment purpose and hence the same is not covered here.

Major types of life insurance products are explained below:

-

-

- Term/protection – Provides for insured amount only if the policyholder dies in the period covered.

- Endowment – Covers risk for a specified period and at the end of the period specified, the insured amount is paid along with any accumulated bonus.

- Money-Back – Subset of an endowment policy, provides for periodic payments of partial payments till the time when the policyholder is alive.

- Whole Life Insurance Product – Provides cover throughout the lifetime of the insured, the sum assured is paid to the family in case of death of the policyholder.

- ULIP – Value of policy changes as per underlying investment assets. It serves both protection and investment needs.

- Pension/Retirement plans – Retirement solution where policyholder determines retirement age and will receive a portion of the commuted amount on retirement and periodic payments from thereon.

- Annuities – a contract where an insurer, in return for periodic payments received till a specified date, pays periodic payments to the insured.

- Group Insurance – covers insurance for a group of people, generally taken by companies on their employees.

- Pros

- Provides financial protection to insured/nominees.

- A loan is available against the premium paid (up to a certain percentage of the premium paid).

- The investment made is allowable as a deduction under section 80C subject to certain conditions.

- Proceeds from certain types of life insurance are exempt from tax.

- Certain types of insurance products provide for periodical income by way of pension etc.

- Guaranteed and predetermined return on money.

- Cons

- Always long time-oriented.

- Can be expensive for old people.

- Term life policies do not have cash values.

- Returns of life insurance proceeds will be sufficient only if one verifies for all conditions, payment terms, and options, etc.

- The terms of the policies are complex.

- Details of insurance policies are not generally communicated to beneficiaries due to which amount of unclaimed insurance is accumulating over a while. As of 31.03.2018, Rs 15,166 crore was lying as an unclaimed amount with several insurance companies.

- Best for

- Individuals planning for income replacement need a long-time horizon.

-

Conclusion:

One should perform his own analysis before making investment in above mentioned modes and above content can be taken as reference for the same.

Senior Citizen Savings Scheme interests are paid quarterly on 30 June, 31 October, 31 december & on 31 March each year and NOT Annually as mentioned in the article