Case Law Details

Asha Industries Vs C.C.E. & S.T. (CESTAT Ahmedabad)

Partnership Firm and proprietorship concern having one common partner as individual could not be defined as relative u/s 2(41) of Companies Act

Conclusion: A proprietorship firm and the partnership firm even though the said proprietor was one of the partner in the partnership firm, both could not be a related person under section 2(41) of the Companies Act,1956. Moreover, the department was kept informed about the partners and proprietor of manufacturer assessee as well as the dealer, however, department had not taken any action and subsequently the demand was raised by invoking extended period of limitation based only on presumption and assumption, which could not be accepted in law.

Held: Appellant-Asha Industries was a partnership firm engaged in the manufacture of IPCO creamy snuff falling under chapter sub heading 240399.40 of the schedule to the Central Excise Tariff Act, 1985 in their factory Nadiad since 2001. Names of three persons as partners were endorsed on the reverse of the Registration Certificate. The goods manufactured by the appellant firm were sold in the local market through M/s. IPCO Sales Agency, which was a proprietor concern of one of the partner in the partnership firm The case of the department was that since the manufacturing firm and the trading firms were run by one family members they were related in terms of Section 4 of Central Excise Act 1944. Accordingly the value at which the trading firm M/s. IPCO Sales Agency sold the goods the same should be treated as transaction value and excise duty was required to be paid on such value. Accordingly, the show cause notice was issued, whereby the differential duty was demanded. The Adjudicating Authority confirmed the entire demand proposed in the show cause notice and imposed the penalty on the appellant manufacturer under Section 11AC and also imposed penalties on other two appellants under Rule 26 of the Central Excise Rules, 2002. Therefore being aggrieved by the order-in-original, the appellant filed the present appeals. It was held that in prima facie view a proprietorship firm and the partnership firm even though the said proprietor was one of the partner in the partnership firm, both could not be a related person. However, this was a highly debatable issue. It was noted that the department was kept informed about the partners and proprietor of manufacturer assessee as well as the dealer. With these information if at all the department was of the view that both were related persons the issue could have been raised within the normal period of limitation i.e. one year. However, department has not taken any action and subsequently the demand was raised by invoking extended period of limitation. There was no dispute that all the correspondences had been acknowledged by the department by putting a rubber stamp and in some of the letters there were signature of the receiving officer. Despite having these letters on record which bears the rubber stamp as well as the signature, the department had not taken pain to carry out the investigation about the genuineness of the rubber stamp and the signature put thereon. Therefore, in absence of carrying out such investigation or inquiry, the observation of the Adjudicating authority to doubt the above letters was based only on presumption and assumption, which could not be accepted in law. In the present case the demand was raised for the period 2002-06 to 2007-08 by issuing the show cause notice dated 30.09.2013 therefore, the entire demand was covered under the extended period of limitation. The department was kept informed from time to time about the constitution of the manufacturer’s partnership firm as well as the buyer’s proprietorship firm. Therefore there was no suppression of fact on the part of the appellant.

FULL TEXT OF THE CESTAT AHMEDABAD ORDER

The brief facts of the case are that the appellant M/s Asha Industries was a partnership firm comprising of Shri Indubhai M Patel, Shri Devangbhai R Patel and Smt. Naynaben M Patel, during the financial years 2005-06 and 2006-07. Later during the financial year 2007-08, Shri Devangbhai R Patel and his wife Smt. Anitabrn D Patel were the partners of the firm. The firm was engaged in the manufacture of IPCO creamy snuff falling under chapter sub heading 240399.40 of the schedule to the Central Excise Tariff Act, 1985 in their factory Nadiad since 2001. They obtained Central Excise Registration on 14.12.2001 in the names of the above Partnership firm. Names of above three persons as partners were endorsed on the reverse of the Registration Certificate. The goods manufactured by M/s Asha Industries were sold in the local market through M/s. IPCO Sales Agency, which is a proprietor concern of Smt. Anitaben D Patel during the period 2005-06, 2006-07 and 2007-08. The said business was operated as partnership firm until 25.07.2005, when the firm was dissolved and one of the partner Smt. Anitaben D Patel allowed to carry on the business as her proprietary concern.

1.1 The case of the department is that since the manufacturing firm and the trading firms are run by one family members they are related in terms of Section 4 of Central Excise Act 1944. Accordingly the value at which the trading firm M/s. IPCO Sales Agency sold the goods the same shall be treated as transaction value and excise duty is required to be paid on such value. Accordingly, the show cause notice dated 20.08.2010 was issued, whereby the differential duty was demanded. The Adjudicating Authority vide Order-In-Original dated 13.09.2013 confirmed the entire demand proposed in the show cause notice and imposed the penalty on the appellant manufacturer under Section 11AC and also imposed penalties on other two appellants under Rule 26 of the Central Excise Rules, 2002. Therefore being aggrieved by the order-in-original, the appellant filed the present appeals.

2. Shri S.P. Mathew, Learned Counsel appearing on behalf of the appellant submits that the Adjudicating Authority held that the partnership firm and a Proprietorship firm are a related persons. It is the submission that the partnership firm is independently a juridical person and not a natural person a juridical person cannot have a relative as defined in clause 41 of Section 2 of Companies Act, 1956 which definition of relative is adopted in section 4 of the Act. The definition of relative provided in Companies Act, 1956 is applicable only in respect of natural person and therefore the said definition has no application to the fact of the present case. In this regard he placed reliance on the Hon’ble Supreme Court judgment in the case of The State of Punjab Vs Jullundur vegetable Synd. AIR 966 SC 1295.

2.1 He further submits that the partners of the manufacturer assessee and the proprietor of the buyer are though members of the same family cannot have any bearing for determination of the issue related person under the Act in as much as the term family or members of the same family is not employed anywhere in Section 4 of the Act while explaining the term related therein. Accordingly, the whole basis of the allegation that the manufacturer assessee and the buyer is a related person is misleading and without any authority of law. Therefore the demand only on the basis of that the manufacturer assessee and the buyer are related cannot be sustained on merit itself.

2.2 Without prejudice, he further submits that the appellant right from the beginning kept informed the department about the constitution of the manufacturer assessee and the buyers, and changes in the partners or proprietor were informed time to time to the department. In this regard he refers to the various correspondence made vide letter dated 22.10.2003, 28.07.2005, 23.04.2007 and 30.07.2007 addressed to Assistant Commissioner, Naidiad Division, Nadiad.

2.3 He submits that from the chain of the correspondence made with the department informing about the partners and the proprietor of manufacturer assessee and the buyer and all the letters were acknowledged by the department, there is no suppression of fact on the part of the appellant, therefore the demand is clearly time barred. He submits that the Adjudicating authority has discarded this vital evidence on the ground that on inquiry from the department, it was found that these letters were not recorded in the inward register of the department.

2.4 He submits that so long all the letters were acknowledged by the department and the genuineness of such letters were not questioned, merely because the concerned inward staff has not recorded the details of these letters in their inward register, It cannot be concluded that this letters were not submitted. In support of his submission that the entire demand is time bared, he placed reliance on the following judgments:

- The State of Punjab Vs M/S. Jullundur Vegetable Synd. – AIR 1966 SC 1295

- Union of India Vs. Atic Industries – 1984 (17) ELT 323 SC

- Continental Chandigarh – 2007 (216) ELT 177 SC Vs. CCE Chandigarh 2007 (216) ELT 177 SC

- Pushpam Pharmaceuticals Co. Vs. CC Ex. Bombay – 1995 (78) ELT 401 SC

- CC Ex. Chennai – III Vs. Ranka Wires Pvt. Ltd. – 2015 (322) ELT 410 SC

- Apex Electricals Pvt Ltd Vs UOI 1992 (61) ELT 413 (Guj.)

- ITW India Ltd. Vs. Commissioner of Cus. Hyderabad – 2008 (322) ELT 257 (Tribunal Bangalore)

3. Shri R K Agarwal Learned Superintendent (AR) appearing on behalf of the Revenue reiterates the finding of the impugned order.

4. We find that entire case is made out on the allegation that there is undervaluation of the excisable goods cleared by M/s Asha Industries on the ground that the buyer namely IPCO Sales Agency is related to M/s. Asha Industries. We find that manufacturer Asha Industries is a partnership firm and the buyer M/s IPCO Sales Agency is proprietorship firm. In our prima facie view a proprietorship firm and the partnership firm even though the said proprietor is one of the partner in the partnership firm, both cannot be a related person. However, this is a highly debatable issue.

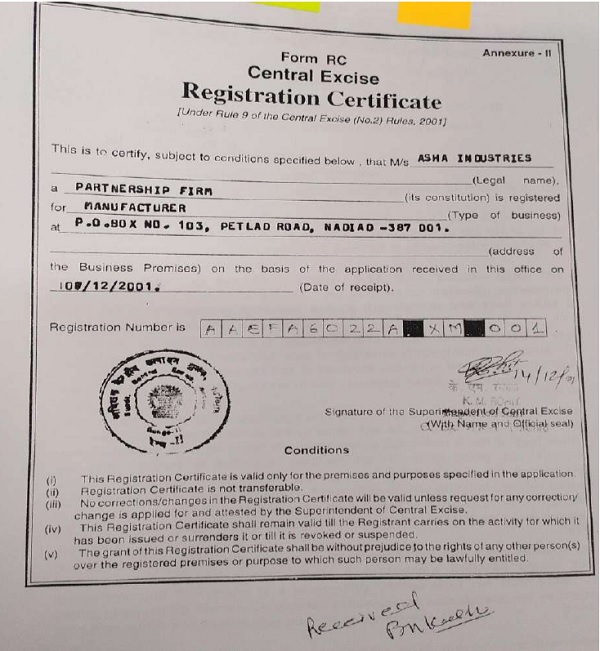

4.1 We find that even though the appellant have strong prima facie case on merit but considering facts of the case the appeals can be decided on the grounds of limitation alone. In this regard we find that the appellant are registered with the Central Excise and obtained the registration certificate which is reproduced below:

–

From the above registration, it can be seen that the appellant manufacturer was partnership firm and the names of the partners are appearing on the registration i.e. Shri Indu bhai M Patel, Shri Devang bahi R Patel, Smt. Nayna ben A Patel. With this information the department was very well within the knowledge of the constitution of the manufacturer partnership firm.

4.2 The appellant from time to time informed the department regarding any change either in the manufacturer firm or in the buyer firm M/s IPCO Sales Agency. The said letters are scanned below:

–

–

–

From the above letters, the department was kept informed about the partners and proprietor of manufacturer assessee as well as the dealer. With these information if at all the department was of the view that both are related persons the issue could have been raised within the normal period of limitation i.e. one year. However, department has not taken any action and subsequently the demand was raised by invoking extended period of limitation. The Adjudicating Authority made a serious charge about the authenticity of the aforesaid letters, on the ground that on the verification from the concerned department it was found that the above letters submitted by the appellant to the department, the same were not recorded in the inward register. Therefore, he concluded that these letters were not submitted to the department.

4.3 In this regard we find that there is no dispute that all the correspondences have been acknowledged by the department by putting a rubber stamp and in some of the letters there are signature of the receiving officer. The appellant have also submitted the some sample letters which were bearing the same rubber stamp and signature. This clearly established that the rubber stamp affixed on the appellant’s letters and signatures are exactly tallying with the other letters submitted to the department. We find that despite having these letters on record which bears the rubber stamp as well as the signature, the department has not taken pain to carry out the investigation about the genuineness of the rubber stamp and the signature put thereon, such as forensic test of the letters, particularly the rubber stamp and the signature.

4.4. It is observed that the department also not inquired from the officer who put the signature on the letters submitted by the appellant. Therefore, in absence of carrying out such investigation or inquiry, the observation of the Adjudicating authority to doubt the above letters is based only on presumption and assumption, which cannot be accepted in law.

4.5. In the present case the demand was raised for the period 2002-06 to 2007-08 by issuing the show cause notice dated 30.09.2013 therefore, the entire demand is covered under the extended period of limitation. We do accept that the above letters were submitted by the appellant with the department whereby the department was kept informed from time to time about the constitution of the manufacturer’s partnership firm as well as the buyer’s proprietorship firm. Therefore there is no suppression of fact on the part of the appellant.

4.6 In the facts and circumstances of the present case, we find that the judgments relied upon by the Learned Counsel which are on the issue of limitation directly apply in the present case. Accordingly, the entire demand is beyond the normal period of limitation. Hence the same is not sustainable on the ground of time bar. Since the demand itself is not sustainable, penalty on the appellant and other two appellants under Rule 26 shall also not be sustainable.

5. Accordingly, we set aside the impugned order by setting aside the demand on the ground of time bar and allow the appeals with consequential relief.

(Pronounced in the open court on 19.10.2023)